The Mosaic Company (MOS), headquartered in Tampa, Florida, manufactures and distributes concentrated phosphate and potash crop nutrients. Valued at $11.2 billion by market cap, the company owns and operates mines that produce key agricultural products like diammonium phosphate, monoammonium phosphate, and ammoniated phosphate, as well as manufactures phosphate-based animal feed additives under the Biofos and Nexfos brands.

Shares of this leading producer of concentrated phosphate and potash have outperformed the broader market over the past year. MOS has gained 29.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 18.4%. In 2025, MOS stock is up 44.5%, surpassing the SPX’s 7.6% rise on a YTD basis.

Zooming in further, MOS’ outperformance is also apparent compared to VanEck Agribusiness ETF (MOO). The exchange-traded fund has gained about 4.9% over the past year. Moreover, MOS’ returns on a YTD basis outshine the ETF’s 13% gains over the same time frame.

Notable gains in operational efficiency and successful cost-reduction initiatives drive MOS' strong performance.

On May 6, MOS shares closed down more than 4% after the company reported its Q1 results. Its adjusted EPS of $0.49 beat Wall Street's expectations of $0.39. The company’s revenue was $2.6 billion, falling short of Wall Street forecasts of $2.7 billion.

For the current fiscal year, ending in December, analysts expected MOS’ EPS to grow 47.5% to $2.92 on a diluted basis. The company’s earnings surprise history is disappointing. It missed the consensus estimates in three of the last four quarters while beating the forecast on another occasion.

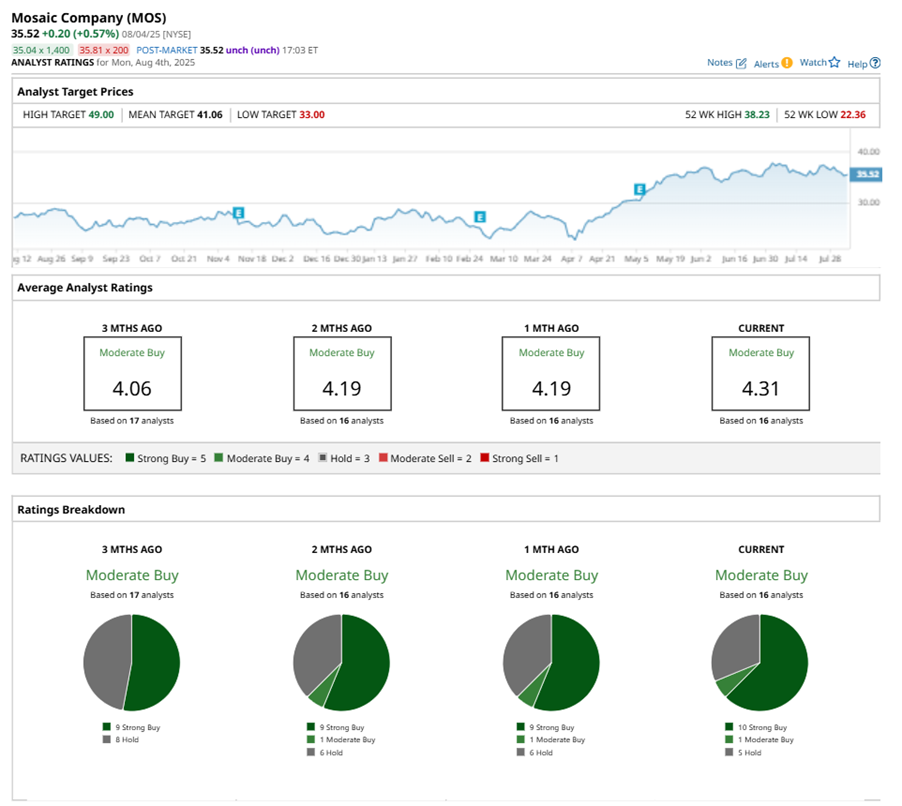

Among the 16 analysts covering MOS stock, the consensus is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, one “Moderate Buy,” and five “Holds.”

This configuration is more bullish than a month ago, with nine analysts suggesting a “Strong Buy.”

On Jul. 25, Berenberg Bank analyst Aron Ceccarelli maintained a “Hold” rating on MOS with a price target of $36, implying a potential upside of 1.4% from current levels.

The mean price target of $41.06 represents a 15.6% premium to MOS’ current price levels. The Street-high price target of $49 suggests a notable upside potential of 38%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)