/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

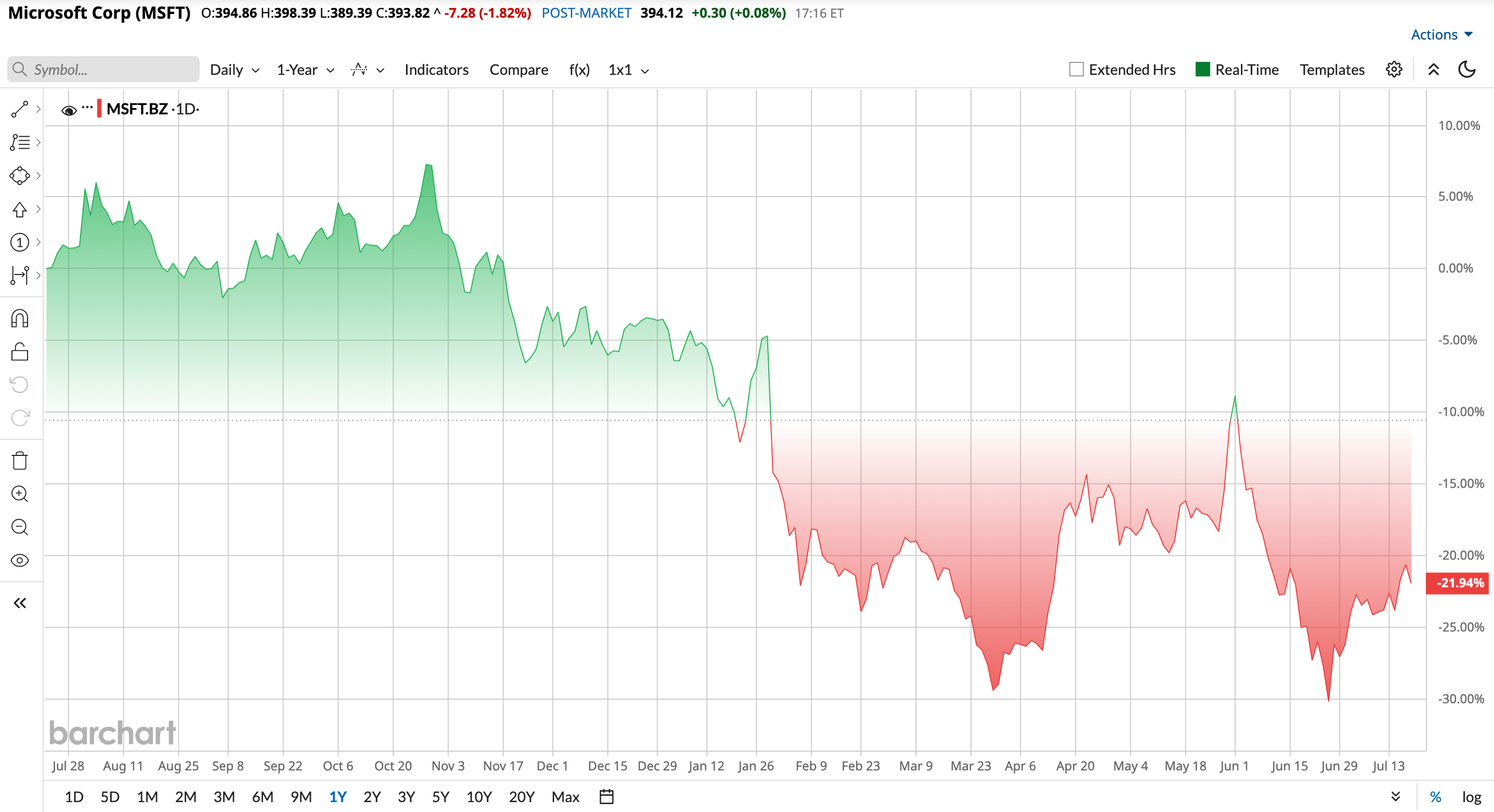

Software stocks did not have a great start to 2026. The iShares Expanded Tech-Software ETF (IGV) fell more than 20% from its recent peak, and when its 50-day moving average dropped below its 200-day, it confirmed a “death cross” that pushed many investors to sell.

After two years of heavy buying on AI hype, reality started to set in. Many software companies admitted that building AI features is expensive, with about 70% saying those costs are hurting margins.

Microsoft Corporation (MSFT), which makes up about 8-8.4% of the iShares Expanded Tech-Software ETF, has been right in the middle of this reset.

The stock dropped 10% after reporting strong earnings, beating both revenue and profit estimates, but investors still cut its valuation as Azure growth slowed slightly from 40% to 39%. That same concern showed up again in July when Citi analyst Tyler Radke cut his price target on Microsoft from $620 to $570. He pointed to ongoing multiple compression across software, even while keeping a “Buy” rating and expecting a strong fiscal Q4. Citi has now lowered its target several times this year, from $690 to $660 in January and from $635 to $600 in April, each time staying positive on the stock.

Microsoft's fundamentals are still strong, but its valuation keeps getting adjusted. So is this just short-term pressure, or something more lasting?

Breaking Down Microsoft’s Latest Numbers

Microsoft runs a broad business built on the Azure cloud, workplace software like Microsoft 365 and Dynamics, and products like LinkedIn, Windows, and gaming. A big part of its strength comes from steady, recurring revenue and long-term enterprise customers.

Even with that, the stock has been under pressure, down 23% over the past 52 weeks and 18.6% year-to-date (YTD).

That pullback has brought valuation closer to peers, with Microsoft now trading at a forward price-to-earnings ratio of 20.51 times compared to the sector average of 24.29 times. The company still returns cash to shareholders, offering a 0.92% dividend yield, below the tech average of 1.37%, but backed by 24 straight years of increases. Its forward payout ratio is 21.42%, and it pays quarterly.

The numbers themselves are still strong. In fiscal Q3 2026, revenue grew 18% to $82.9 billion, operating income rose 20% to $38.4 billion, and net income climbed 23% to $31.8 billion, with EPS at $4.27. Cloud remains the main driver, with Microsoft Cloud revenue up 29% to $54.5 billion, and future demand looks solid with remaining performance obligations up 99% to $627 billion. Azure grew 40%, pushing Intelligent Cloud revenue up 30% to $34.7 billion. Productivity and Business Processes rose 17% to $35 billion, while More Personal Computing dipped 1% to $13.2 billion. And, Microsoft returned $10.2 billion to shareholders during the quarter.

Growth Engines Remain in Focus

Microsoft is building out its AI capacity in a very practical way, starting with its partnership with 3M Company (MMM). Azure is set to use 3M’s Expanded Beam Optical technology in its data centers, replacing traditional fiber connections. This should make installations faster, reduce the need for constant maintenance, and keep performance stable even in crowded data centers. For Microsoft, it is a direct way to handle growing AI demand more efficiently.

Power is another big piece of the puzzle. Microsoft has a 20-year deal with Chevron Corporation (CVX) to supply energy to a major data center project in West Texas. The site is expected to deliver about 2.67 gigawatts of capacity and will be built in phases so it can expand over time. With a mix of natural gas and scalable infrastructure, the setup helps secure the energy needed to run large-scale AI workloads without interruptions.

On the product side, Microsoft is pushing AI deeper into real-world use. Its partnership with Mayo Clinic focuses on building a healthcare AI model that can handle complex clinical decisions. By combining Mayo’s medical data with Microsoft’s cloud and AI tools, the goal is to support earlier diagnoses and more tailored treatments. Microsoft plans to offer this through Azure APIs, making it easier for worldwide healthcare systems to use.

Wall Street Reassesses the Upside

Microsoft is set to report earnings on July 29, after the close. For the June quarter, earnings are projected at $4.21 per share, up 15.34% from $3.65 a year ago. For the full fiscal year ending June 2026, estimates are at $16.71 compared to $13.64 last year, marking a 22.51% increase.

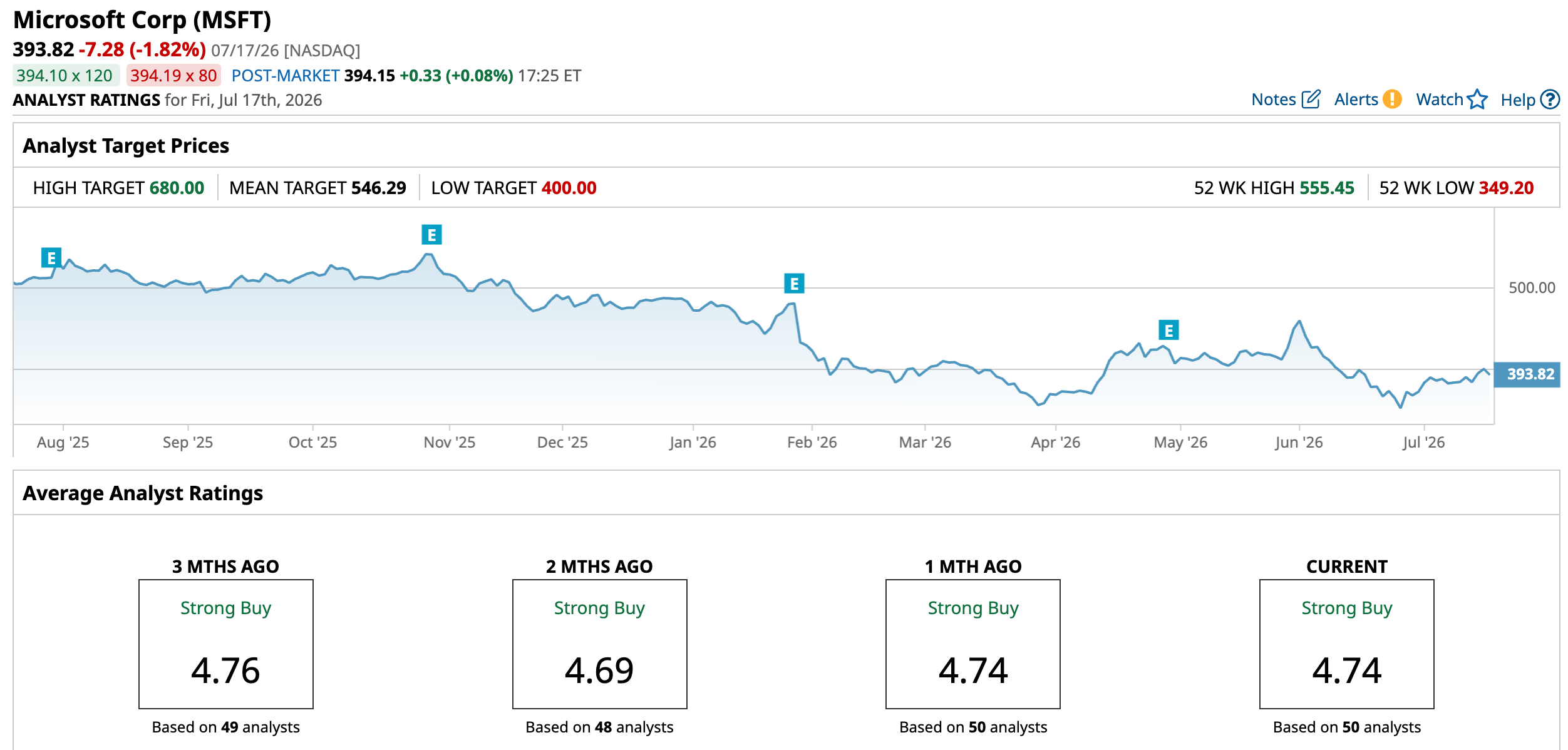

Bank of America has a “Buy” rating on Microsoft with a $500 price target, pointing to its strong position across both AI infrastructure and applications. Benchmark is also bullish, with a “Buy” rating and a $450 target, highlighting the company’s wide ecosystem across Windows, Office, LinkedIn, GitHub, and Azure as a key advantage that is hard to match.

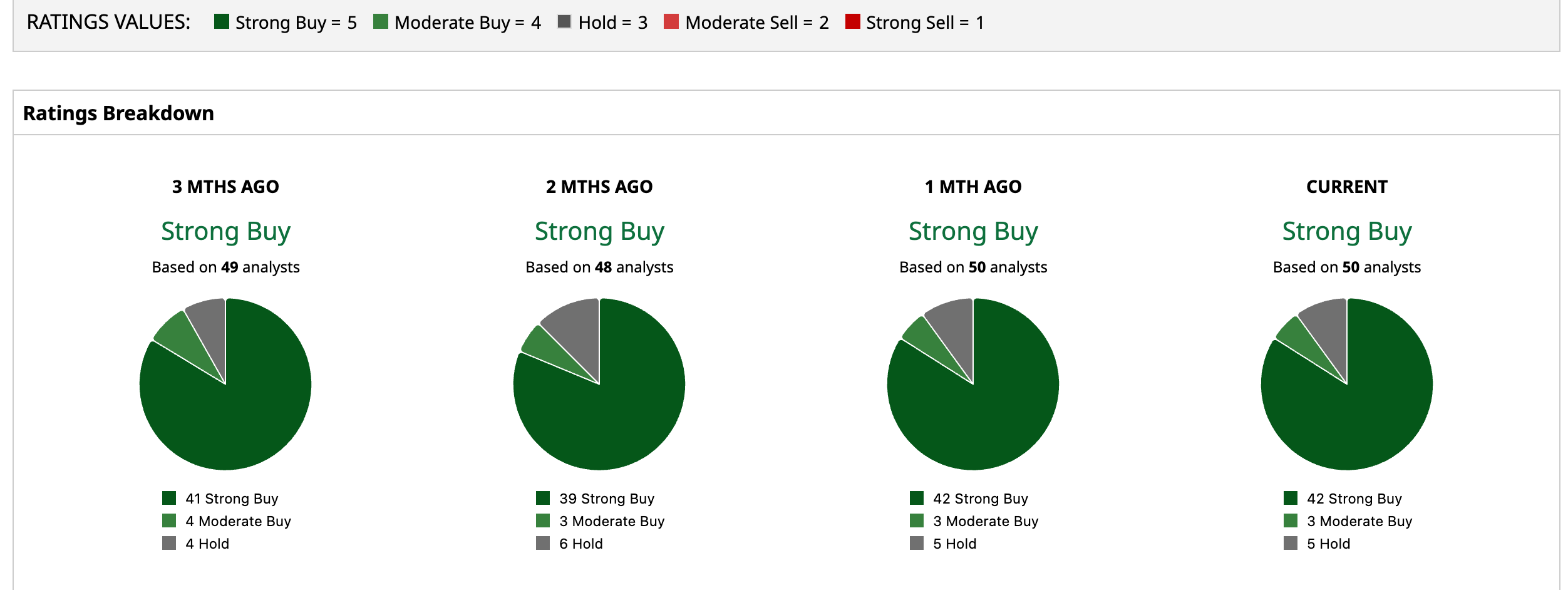

Overall sentiment is still very strong. Of 50 analysts covering Microsoft, a consensus rates it a “Strong Buy”, with an average price target of $546.29. Based on the current price, that suggests a 38.7% upside from here.

Conclusion

Multiple compression is real, but the core story here has not broken. Microsoft continues to deliver solid double-digit earnings growth, its AI and cloud engines are expanding, and analyst conviction remains firmly bullish despite trimmed price targets. The recent pullback looks more like a valuation reset than a deterioration in fundamentals. Going forward, the stock may likely trade with some near-term volatility as the market digests growth versus valuation. But the path of least resistance still appears higher as earnings continue to catch up with sentiment.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)