/PayPal%20Holdings%20Inc%20HQ%20photo-by%20bennymarty%20via%20iStock.jpg)

PayPal (PYPL) shares are ripping higher on Wednesday following reports of takeover interest from rival fintech giant Stripe and private equity firm Advent International.

According to Reuters, the digital payments pioneer has received a joint $53 billion buyout proposal that values its shares at $60.5 each, representing a 28% premium over their previous close.

Despite today’s explosive rally, PayPal stock remains down about 8% versus its year-to-date high.

Why Is Stripe Interested in Buying PayPal?

The surprising proposal, backed by $50 billion in committed bank financing, would see Stripe and Advent International jointly own PayPal as equal partners.

For Stripe, which secured a $159 billion valuation following a February employee tender offer, the acquisition may prove transformative given it already dominates back-end developer infrastructure but lacks a ubiquitous, customer-facing brand.

Buying PYPL would give Stripe access to a premium merchant checkout network used by over 400 million active consumers globally.

Combining its technical prowess with PayPal’s consumer legacy, the fintech giants want to create a strong ecosystem capable of staving off heavy competitive pressure from Apple's (AAPL) Apple Pay and Alphabet's (GOOG) (GOOGL) Google Pay.

Is There Any Further Upside Left in PYPL Shares?

PayPal shares are currently hovering around $55, roughly 10% below the offer price. On paper, that leaves modest arbitrage upside for short-term traders.

However, a deeper narrative is playing out. Sources close to the matter caution that the PayPal board is reluctant to engage with suitors at the proposed valuation, which represents only a fraction of its pandemic high.

Meanwhile, newly appointed chief executive Enrique Lores is already executing a multi-year turnaround, including cutting 20% of the workforce to save $1.5 billion.

If PayPal rejects the offer, demanding a higher premium, the fintech stock could pare back today’s gains just as easily.

Why Caution Is Warranted in Playing PayPal

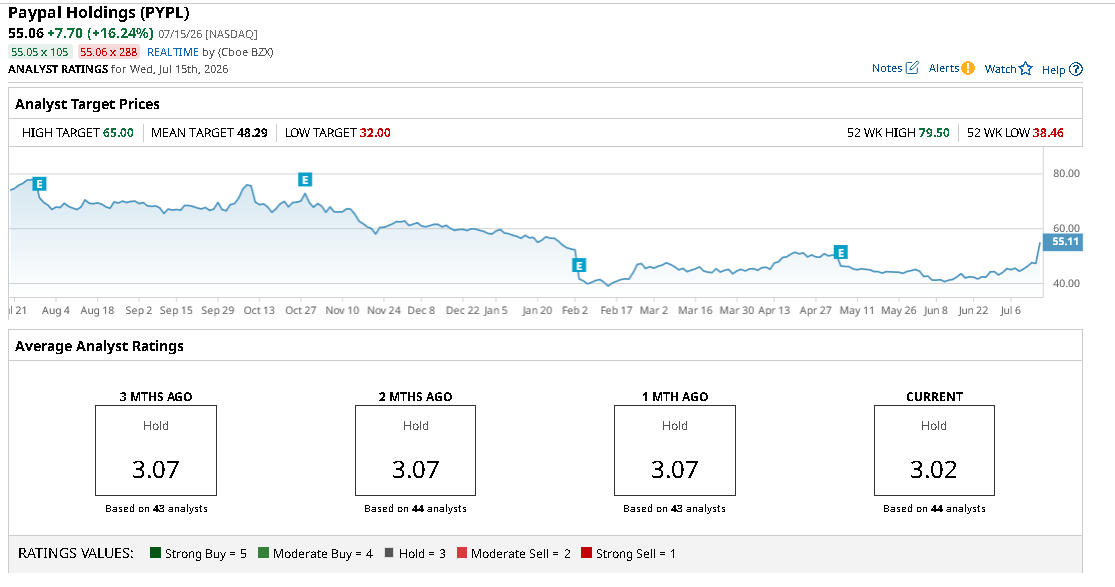

Investors are recommended to exercise caution in playing PYPL stock also because Wall Street analysts seem to view it as overvalued at current levels.

According to Barchart, the consensus rating on PayPal sits at “Hold” only, with the mean price target of roughly $48 indicating potential downside of more than 10% over the next 12 months.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)