/Apple%20products%20arranged%20on%20desk%20by%20tashka2000%20via%20iStock.jpg)

Apple (AAPL) is the world's most valuable technology company, founded in 1976 by Steve Jobs, Steve Wozniak, and Ronald Wayne, and headquartered in Cupertino, California. The company designs, manufactures, and markets a deeply integrated ecosystem of hardware, software, and services spanning iPhone, Mac, iPad, Apple Watch, AirPods, and Apple TV, alongside a high-margin Services portfolio encompassing the App Store, iCloud, Apple Music, Apple TV+, Apple Pay, and AppleCare.

With over 2.5 billion active devices globally, a market capitalization of approximately $4.63 trillion, and an imminent CEO transition from Tim Cook to hardware chief John Ternus, Apple remains the defining benchmark of consumer technology innovation and capital efficiency.

Apple Stock Shines in 2026

AAPL stock has delivered a 55% return over the trailing 12 months, with a 52-week range of $201.50 to new highs of around $325 today. The stock is up 19% year-to-date (YTD), and today's new high reflects sustained momentum driven by iPhone 17 demand and Services growth.

Compared to the S&P 500 Information Technology Index ($SRIT), which has posted strong but more measured gains in 2026, AAPL has meaningfully outperformed its benchmark, with the stock's 50%-plus trailing return cementing its status as one of the standout performers in the large-cap technology universe.

Apple results Beat Estimates

Apple reported fiscal Q2 2026 revenue of $111.2 billion, up 17% year-over-year (YoY), surpassing the analyst consensus of $109.66 billion. Diluted EPS of $2.01 beat the Wall Street estimate of $1.95, extending Apple's streak of quarterly earnings beats to eight consecutive quarters. iPhone revenue came in at $56.99 billion, a March quarter record, up 22% YoY, while Services revenue reached an all-time high of $30.98 billion, up 16% from a year earlier. iPhone was the only segment that narrowly missed estimates, while Mac, iPad, Wearables, and Greater China all outperformed expectations.

Gross margin reached 49.3%, above the high end of the guided range and up 110 basis points sequentially, with Services gross margin at 76.7%. Net income climbed to $29.58 billion from $24.78 billion a year ago, while the board authorized a fresh $100 billion share buyback program and raised the dividend by 4%, reinforcing Apple's commitment to returning capital to shareholders at a pivotal moment in its leadership transition.

For Q3 FY2026, Apple guided revenue growth of 14% to 17% YoY, dramatically ahead of the analyst consensus expectation of approximately 9.5%, with gross margin expected between 47.5% and 48.5%. Management flagged memory cost pressures as a growing headwind beyond the June quarter, while CEO Tim Cook highlighted the installed base reaching an all-time high across all major product categories and geographic segments. The robust Q3 outlook, paired with continued Services momentum and AI feature integration across the iPhone lineup, frames a confident handover to incoming CEO John Ternus.

Apple Handed a Rare Downgrade

Apple shares came under pressure after KeyBanc Capital Markets downgraded the stock from “Sector Weight” to “Underweight,” maintaining a $250 price target, implying a 23% downside from current levels. Analysts Brandon Nispel and John Vinh flagged aggressive device price increases, with iPads up $100–$200, MacBooks up $100–$300, and Mac Studios up $500–$1,300, as a structural demand headwind, arguing that price elasticity for these products exceeds 1, meaning every dollar increase costs more than one unit of demand.

KeyBanc also warned that U.S. carrier subsidy pullbacks from Verizon (VZ) and AT&T (T) could extend device holding periods and suppress upgrade cycles. While iPhone revenue is expected to grow 23.2% in fiscal 2026, KeyBanc projects a sharp deceleration to 4.9% in fiscal 2027, well below the 8.3% consensus, with Services growth also expected to slow meaningfully.

How to Play AAPL Stock?

KeyBanc's “Underweight” call is a sobering counterpoint to Apple's all-time high, raising legitimate questions about price elasticity, carrier subsidy headwinds, and a potentially sharp iPhone growth deceleration in fiscal 2027.

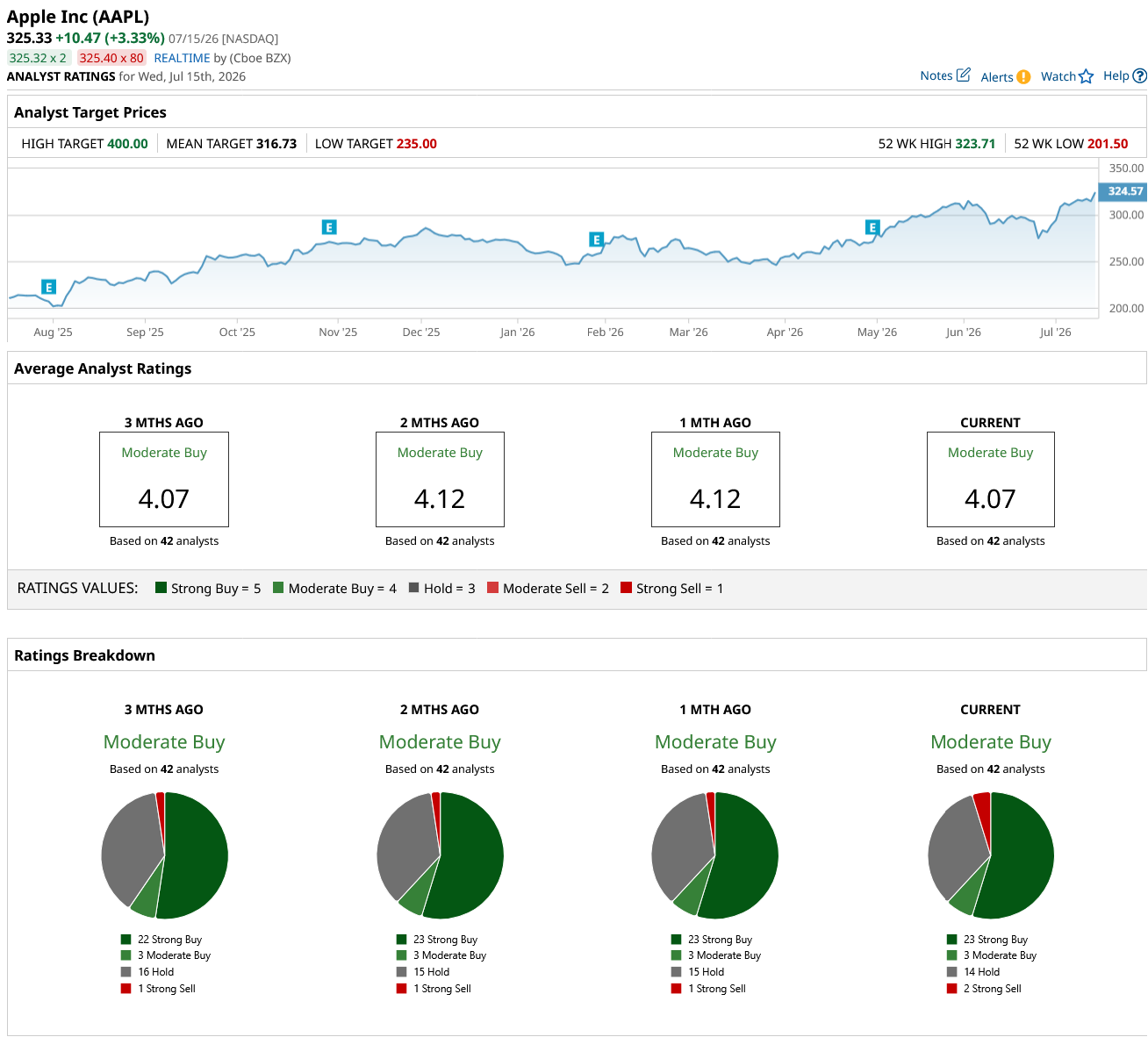

Wall Street, however, remains broadly constructive, handing AAPL stock a consensus "Moderate Buy" rating across 42 analyst ratings, comprising 23 “Strong Buy,” three “Moderate Buy,” 14 “Hold,” and two “Strong Sell” ratings. The mean price target of $316.73 is essentially in line with the current market price (a 2.5% difference), suggesting the stock is fairly valued at these levels and leaving the upcoming July 30 earnings report as the next meaningful catalyst.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)