/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)

Tech giant Apple (AAPL) has never been a company that grows only by building everything from scratch. While the iPhone maker is known for creating category-defining products and one of the world’s most loyal customer ecosystems, it has also quietly used acquisitions to strengthen its technology, bring in specialized talent, and solve problems long before they become visible to consumers. Many of those deals fly under the radar, but they often end up shaping Apple’s products and developer tools in meaningful ways.

Its latest acquisition appears to follow that pattern.

According to filings published by the European Commission, Apple has acquired certain assets and hired employees from SigScalr, the startup behind SigLens, an open-source observability platform. The March 12 transaction surfaced through the European Union’s Digital Markets Act disclosure requirements. Since then, SigScalr’s website has gone offline, while SigLens’ GitHub repository has been archived and made read-only.

SigLens is designed to help developers collect, monitor, search, and analyze logs, metrics, and application traces from software and infrastructure from a single platform. In simple terms, it gives engineers a real-time view of the performance of applications, making it easier to detect bugs, troubleshoot issues, and optimize performance. SigScalr had positioned the platform as a faster and more efficient alternative to observability tools offered by companies such as Splunk, Datadog (DDOG), and Elasticsearch.

While Apple has yet to comment on its planned use of the technology, the acquisition could strengthen its developer ecosystem, improve internal software monitoring capabilities, and support its growing AI and cloud infrastructure efforts. That makes this small acquisition one worth watching as investors assess implications and effects for Apple over the long run.

About Apple Stock

Apple has spent decades turning everyday technology into products people can’t imagine living without. From the iPhone that reshaped communication to the Mac and iPad that redefined personal computing, the Cupertino-based, California giant has built one of the world's strongest consumer brands.

However, today's Apple story extends well beyond hardware. Its fast-growing Services business, powered by more than a billion paid subscriptions across offerings like iCloud, Apple Music, the App Store, and Apple Pay, has become a dependable source of recurring, high-margin revenue that keeps customers firmly within the Apple ecosystem. That combination has helped the company grow its market cap to a whopping $4.63 trillion.

Yet, AAPL stock has not had an entirely smooth ride this year.

The broader tech sector has been navigating choppy waters, with investors weighing geopolitical uncertainty, higher interest rates, and growing debate over whether enthusiasm surrounding AI has run ahead of fundamentals. Even a company with Apple’s track record was not spared from those concerns, and the stock spent part of the year under pressure.

But the tide has gradually turned.

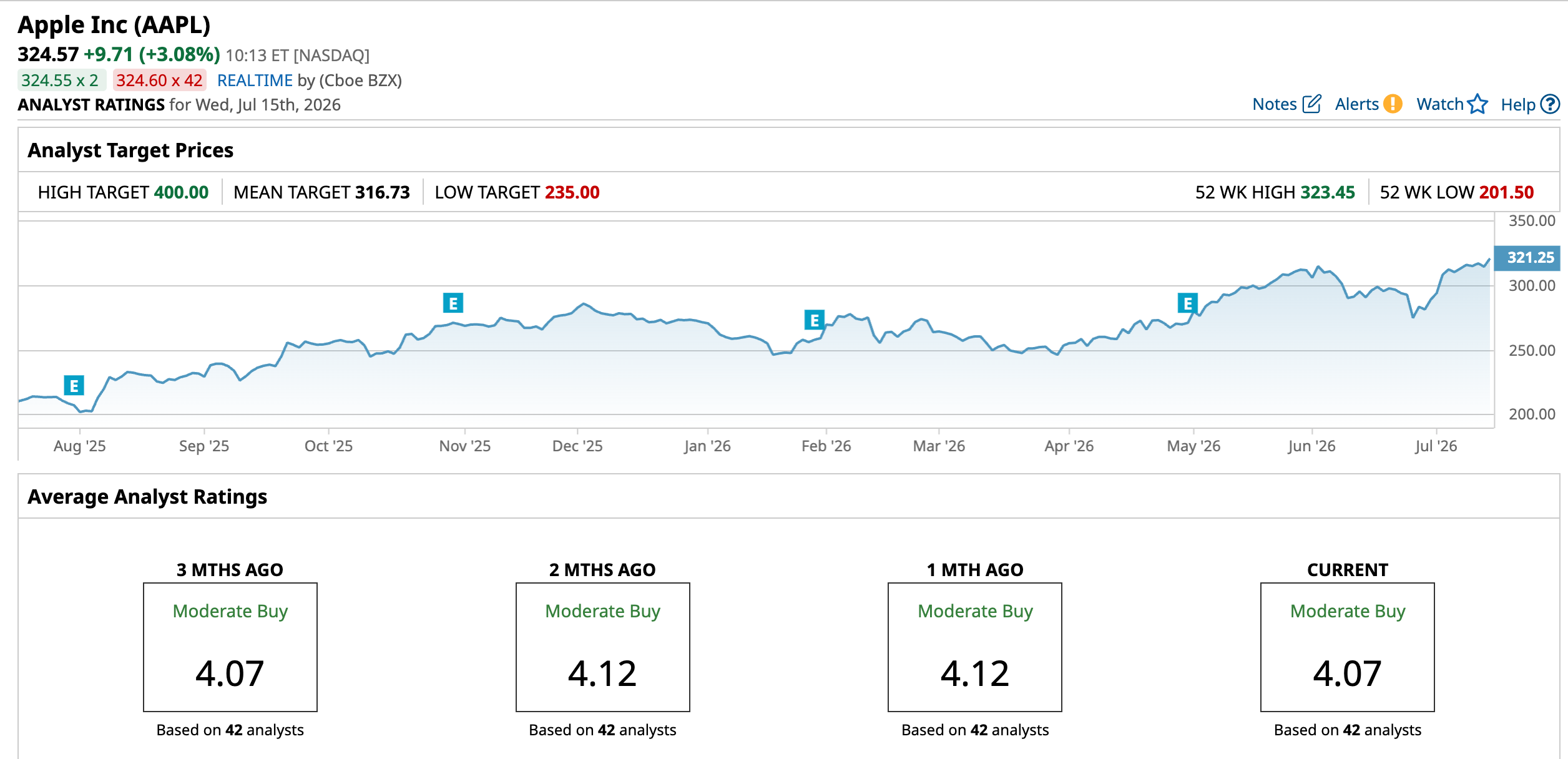

After starting 2026 in negative territory, Apple has clawed its way back, with shares now up 18.1% year-to-date (YTD). The rebound has been fueled by confidence in the company’s expanding Services business, growing AI strategy, resilient iPhone demand, and expectations that Apple will increasingly monetize AI across its vast installed base of devices.

Momentum has accelerated in recent months. Apple stock has gained 20.5% over the past three months and is up 53.5% over the last 52 weeks, reflecting renewed investor confidence in the company’s long-term growth story. Shares recently touched an all-time high of $323.45 on July 13 before pulling back about 2.7%, a reminder that even market leaders rarely move in a straight line. And, today's price thus far set a new high of $325.68.

Technically, trading volume has picked up alongside the rally, suggesting fresh buying interest is supporting the move higher. The 14-day RSI sits 66.64, indicating bullish momentum without the stock entering overbought territory.

Meanwhile, the MACD oscillator signals bullish sentiments, with the MACD line holding above the signal line. Also, the histogram has turned positive and continues to strengthen, signaling that buying pressure is outweighing selling pressure and that the near-term trend remains tilted in favor of the bulls.

Apple stock is not exactly cheap these days. Shares trade at 36.06 times forward adjusted earnings and roughly 9.66 times sales, both above the company’s historical averages and many of its large-cap tech peers. Even so, investors have shown they are willing to pay a premium for Apple’s unmatched ecosystem, consistent execution, robust cash generation, and loyal customer base.

The dividend only strengthens that investment case. Apple has increased its dividend for 13 consecutive years, yet pays out just 12.51% of its earnings, leaving plenty of room for future hikes. Combined with its aggressive share repurchases, that disciplined capital return strategy continues to make Apple an attractive long-term holding for many investors.

A Snapshot of Apple’s Q2 Results

Apple’s fiscal Q2 2026 report, released on April 30, proved once again why it is one of the most consistent money-making machines in the market. When the tech giant reported quarterly results, it not only beat Wall Street’s expectations but also delivered record March-quarter revenue, earnings, and iPhone sales, underscoring that demand for its ecosystem remains remarkably resilient despite a challenging macro environment.

Apple generated $111.2 billion in revenue, up 17% year-over-year (YOY), while EPS climbed 22% annually to $2.01. The biggest star of the show was once again the iPhone. Revenue from Apple’s flagship product jumped 22% to $57 billion, fueled by strong global demand for the iPhone 17 lineup and record customer upgrade activity. Management said the iPhone business delivered its best-ever March quarter, underscoring the brand’s staying power even as the smartphone market matures.

Services continued to be another major growth engine. Revenue reached a record $31 billion, up 16% YOY, as the App Store, iCloud, subscriptions, payments, advertising, and media businesses all posted healthy growth. The segment has become an increasingly important piece of Apple’s business, providing a steady stream of recurring, high-margin revenue that helps cushion the company's hardware cycles.

The rest of the portfolio also chipped in. Mac revenue increased 6% annually to $8.4 billion, iPad sales rose 8% to $6.9 billion, and Wearables, Home, and Accessories revenue climbed 5% to $7.9 billion.

In addition, margins moved in the right direction. Overall gross margin expanded to 49.3%, with the Services business delivering an impressive 76.7% gross margin, while Products posted a 38.7% margin despite ongoing supply-chain constraints and higher memory costs.

Apple closed the quarter with a formidable balance sheet, holding $147 billion in cash and marketable securities against $85 billion in total debt, resulting in a net cash position of $62 billion. The company continued to reward shareholders, returning $15 billion during the quarter through a combination of dividends and share buybacks. Management emphasized that its capital allocation strategy remains unchanged – invest in the business first and return excess cash to shareholders over time. However, the company said it will no longer target a specific “net cash neutral” position, choosing instead to evaluate its cash holdings and debt levels independently.

Looking ahead, management struck an upbeat tone. Apple expects fiscal third-quarter revenue to grow 14% to 17% YOY, with gross margins projected between 47.5% and 48.5%. The company is expected to release its fiscal Q3 report on Thursday, July 30.

Meanwhile, analysts monitoring the company remain optimistic, predicting Q3 revenue around $108.9 billion, while EPS is anticipated to rise by 19.8% YoY to $1.88. Looking further ahead to fiscal 2026, profit is expected to be $8.74 per share, up 17.2% YOY, before surging another 9.4% annually to $9.56 per share in fiscal 2027.

What Do Analysts Expect for Apple Stock?

Wall Street remains bullish on Apple’s long-term outlook. On July 13, Citi analyst Asiya Merchant reiterated a “Buy” rating and raised the price target to $365 from $315. Merchant expects Apple’s premium brand and loyal customer base to support selective price increases, helping protect margins despite higher costs. The analyst also sees strong iPhone 17 demand, AI-powered Siri enhancements, and Apple’s September product launch as key catalysts that could boost revenue and further strengthen investor sentiment.

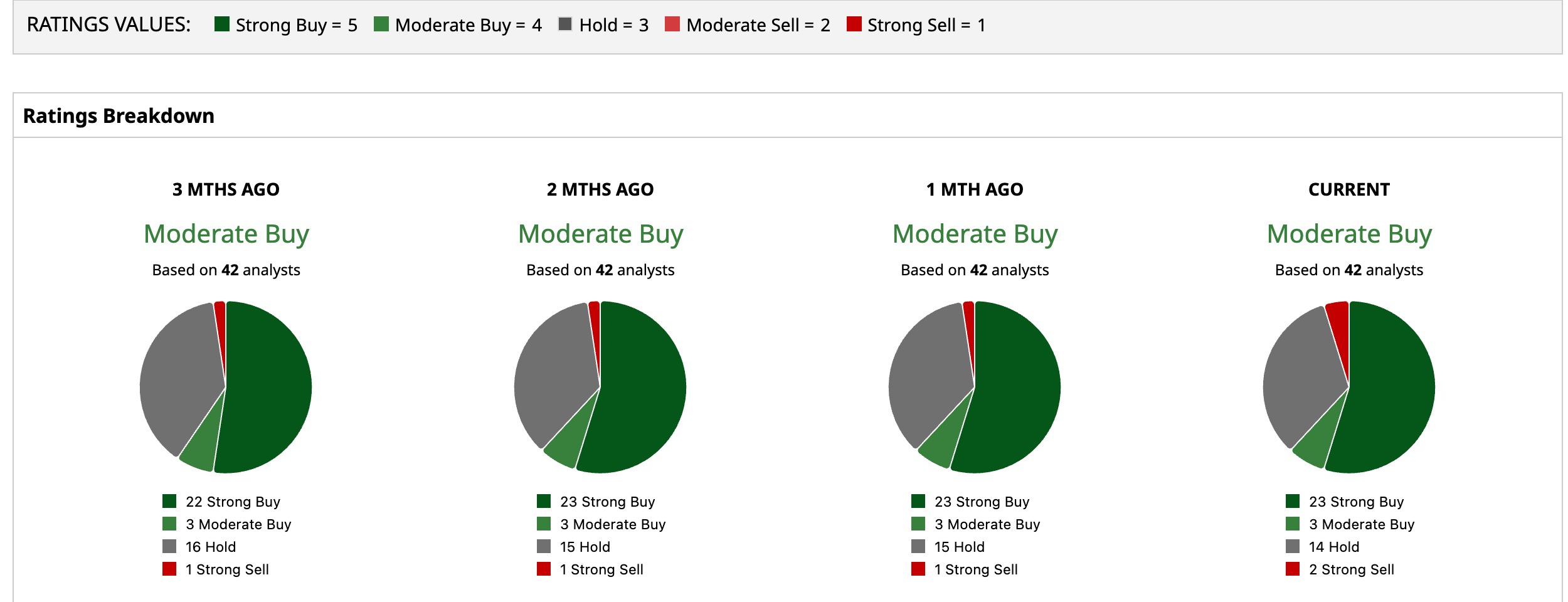

AAPL stock has a consensus “Moderate Buy” rating overall. Out of 42 analysts covering the tech stock, 23 recommend a “Strong Buy,” three give a “Moderate Buy,” 14 analysts stay cautious with a “Hold” rating, and the remaining two analysts have a “Strong Sell” rating.

The average analyst price target of $316.73 shows a downside of 2.4% from the stock's current trading price. But the Street-high target price of $400 suggests that the stock could rally as much as 23.2% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)