/Henry%20Schein%20Canada%20office%20building%20in%20Vaughan%20By%20JHVEPhoto.jpeg)

Henry Schein, Inc. (HSIC), headquartered in Melville, New York, provides health care products and services to dental practitioners, laboratories, physician practices, and ambulatory surgery centers, government, institutional health care clinics, and other alternate care clinics. Valued at $9.8 billion by market cap, the company provides shop supplies, as well as dental and medical solutions and services to improve operational success and clinical outcomes. The world’s largest health care solutions provider is expected to announce its fiscal second-quarter earnings for 2026 in the near future.

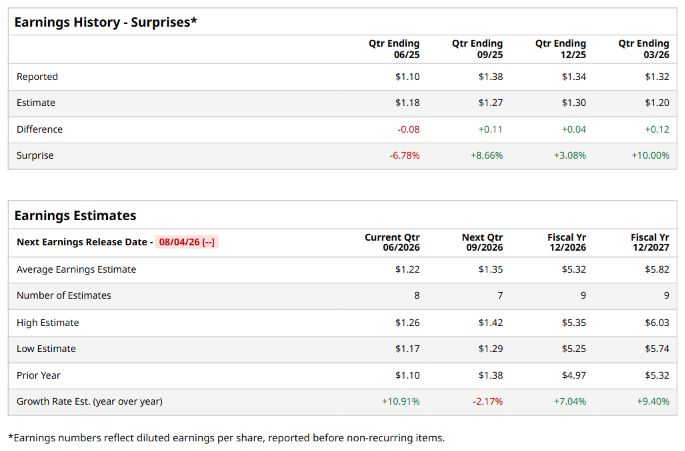

Ahead of the event, analysts expect HSIC to report a profit of $1.22 per share on a diluted basis, up 10.9% from $1.10 per share in the year-ago quarter. The company beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

For the full year, analysts expect HSIC to report EPS of $5.32, up 7% from $4.97 in fiscal 2025. Its EPS is expected to rise 9.4% year over year to $5.82 in fiscal 2027.

HSIC stock has outperformed the S&P 500 Index’s ($SPX) 20.3% gains over the past 52 weeks, with shares up 23% during this period. Similarly, it outperformed the State Street Health Care Select Sector SPDR ETF’s (XLV) 17.2% returns over the same time frame.

HSIC’s medical segment softened due to a milder flu season lowering point-of-care diagnostic demand, though strength in Home Solutions and tech offerings largely offset the impact.

On May 5, HSIC shares closed up more than 3% after reporting its Q1 results. Its adjusted EPS of $1.32 exceeded Wall Street expectations of $1.20. The company’s revenue was $3.4 billion, beating Wall Street forecasts of $3.3 billion. HSIC expects full-year adjusted EPS in the range of $5.23 to $5.37.

Analysts’ consensus opinion on HSIC stock is reasonably bullish, with a “Moderate Buy” rating overall. Out of 18 analysts covering the stock, nine advise a “Strong Buy” rating, eight give a “Hold,” and one recommends a “Strong Sell.” HSIC’s average analyst price target is $88.47, indicating a potential upside of 1.8% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)