/Ge%20Aerospace%20By%20Grand%20Warszawski.jpeg)

Aerospace companies are heading into earnings season with strong demand behind them. General Electric Aerospace (GE), now a focused aviation business after General Electric’s 2024 breakup, has built a backlog of over $210 billion, including more than $170 billion in services, giving it strong visibility into future revenue.

In February 2026, United Airlines (UAL) chose General Electric Aerospace’s GEnx engines to power 300 new Boeing 787 Dreamliner jets, pushing total future GEnx deliveries close to 1,800 engines, including spares. Then in May, a meeting between President Trump and China’s President Xi Jinping helped break a years-long freeze in aircraft orders, with China agreeing to buy 200 planes from Boeing (BA). That deal is expected to benefit General Electric Aerospace, as it will supply 400 to 450 engines.

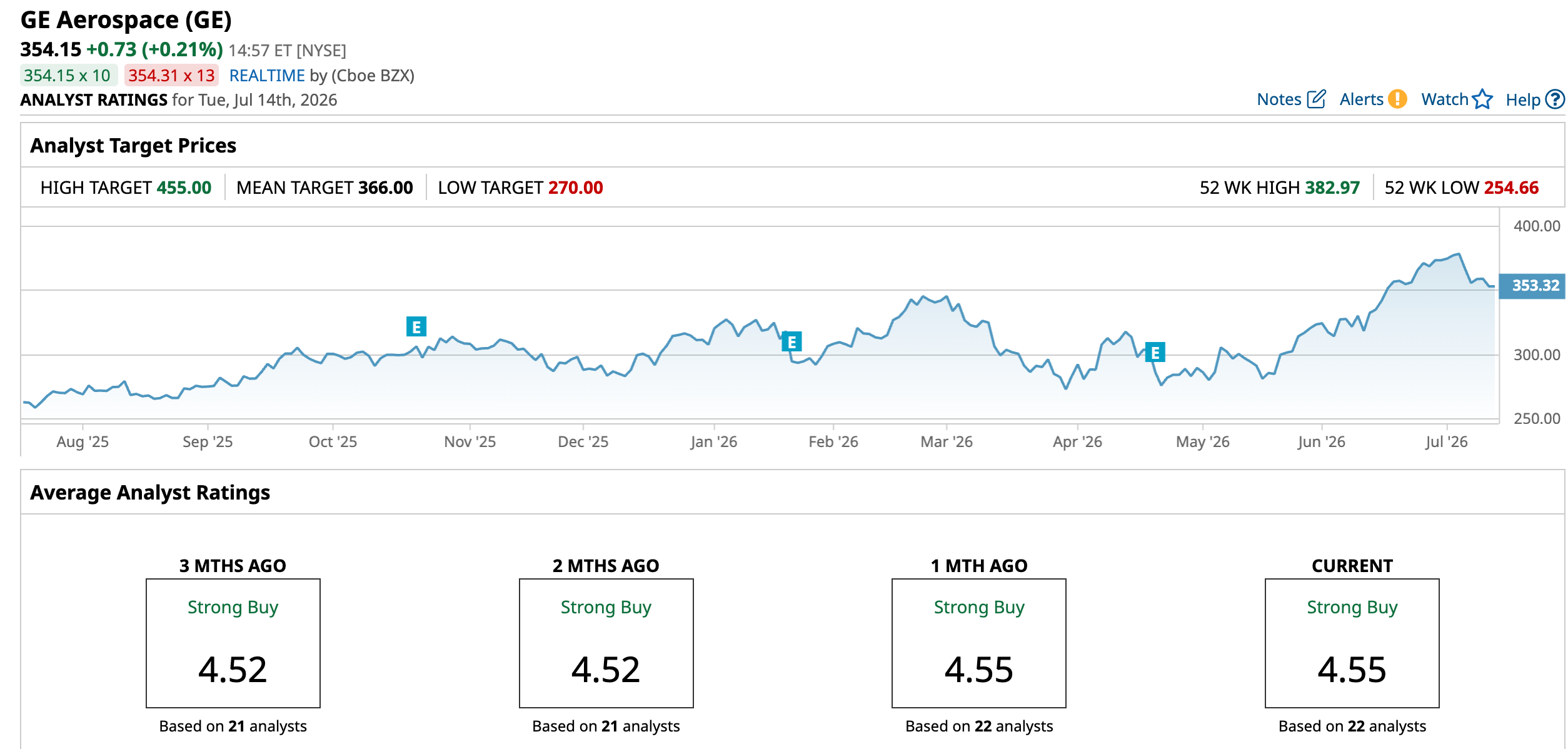

Thursday, July 16, is shaping up to be one of the most closely watched days of the summer for GE Aerospace shareholders. The company will release its second-quarter 2026 earnings results before the market opens, with the official webcast scheduled for 7:30 a.m. EST. Analysts have responded with multiple price target increases in early July 2026.

With five straight earnings beats, steady growth in services, and continued support from Wall Street, can General Electric Aerospace deliver again and justify where the stock is trading?

Breaking Down the Latest Numbers

General Electric Aerospace builds aircraft engines and systems for both commercial airlines and defense, while also making steady money from servicing those engines over time. The stock has been on a strong run, up 35% over the past year and another 15% so far this year.

But it also means the stock is not cheap. General Electric Aerospace trades at a forward price-to-earnings ratio of 48.04 times, well above the sector average of 20.92 times.

On dividends, it is steady but not a big payer. The stock yields 0.47%, below the industry average of 2.36%. It recently paid a $0.47 quarterly dividend on July 6, with a payout ratio of 22.68%. The company has raised its dividend for three straight years, leaving room to continue investing in the business.

GE Aerospace delivered impressive results for Q1 2026, reported on April 21. Adjusted earnings per share reached $1.86, marking a 25% year-over-year (YOY) increase and beating consensus estimates by a healthy margin. Total GAAP revenue climbed 25% to $12.4 billion, while adjusted revenue rose 29% to $11.6 billion. Orders surged an outstanding 87% to $23.0 billion, with services orders up 49% and equipment orders more than tripling.

Key highlights from Q1 included 39% growth in commercial services revenue, driven by a 35% increase in internal shop visit revenue and more than 25% growth in spare parts. This performance was supported by a massive $170 billion commercial services backlog, offering strong demand visibility heading into subsequent quarters. Operating profit rose 18%, though margins faced some pressure from higher install engine volume and targeted investments.

The first quarter was solid, so the next report has a high bar to clear. It should give us a better idea of how GE is dealing with parts supply, holding prices steady, and balancing the commercial plane business with defense work.

Analyst Expectations and Market Sentiment

Analysts expect $1.86 per share for the June quarter, up from $1.66 last year, which is about 12.05% growth. Revenue is projected to climb roughly 23% to approximately $11.77 billion, fueled by high-teens services growth and solid engine deliveries. For the full year 2026, earnings are projected at $7.48, compared to $6.37 in 2025, pointing to a 17.43% increase.

Jefferies lifted its price target to a street-high $455 on July 2, Susquehanna raised its target to $430 on July 9, and TD Cowen lifted its target to $380 (from $330) on July 13.

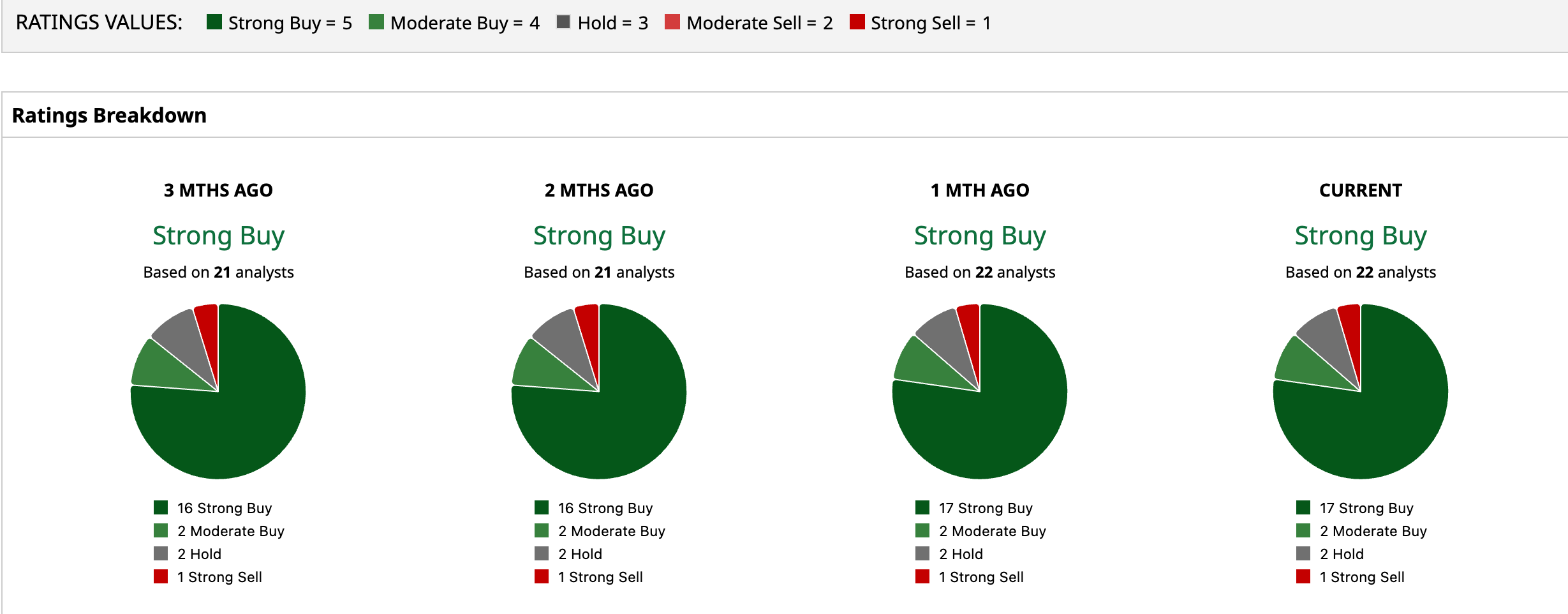

Overall, sentiment is clearly positive. Of 22 analysts covering General Electric Aerospace, a consensus rates it a “Strong Buy”, with an average price target of $366.00, indicating an upside potential of 3.4%. The Street-high price target of $455 implies a climb of 28.5% from here.

Conclusion

GE heads into July 16 with nearly everything lining up in its favor, from strong earnings momentum to a demand backdrop that continues to tighten across aerospace. The premium valuation leaves little room for error, but the company has consistently delivered. Given the track record of beats, rising services strength, and bullish analyst positioning, the most likely near-term direction still tilts upward, especially if guidance comes in stronger again. Notwithstanding, expectations are already high, so any upside will likely depend on GE proving it can keep outperforming at scale.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)