/Space/Rocket%20takes%20off%20by%20Alones%20via%20Shutterstock.jpg)

Veteran investor George Noble didn’t mince words when SpaceX (SPCX) debuted on the public market. He argued that the SPCX IPO was “designed to separate retail investors from their money,” a warning that quickly spread across financial social media as investors rushed into one of the year's most anticipated listings.

The timing of that comment has become difficult to ignore. After an explosive post-IPO rally, SpaceX shares have surrendered much of those gains, leaving investors debating whether the early excitement got too far ahead of the company's fundamentals.

While the long-term growth story remains compelling, the stock's lofty valuation and heavy investment spending have fueled concerns that the market priced in years of future success almost immediately.

SpaceX's Post-IPO Rally Quickly Turned Into a Reality Check

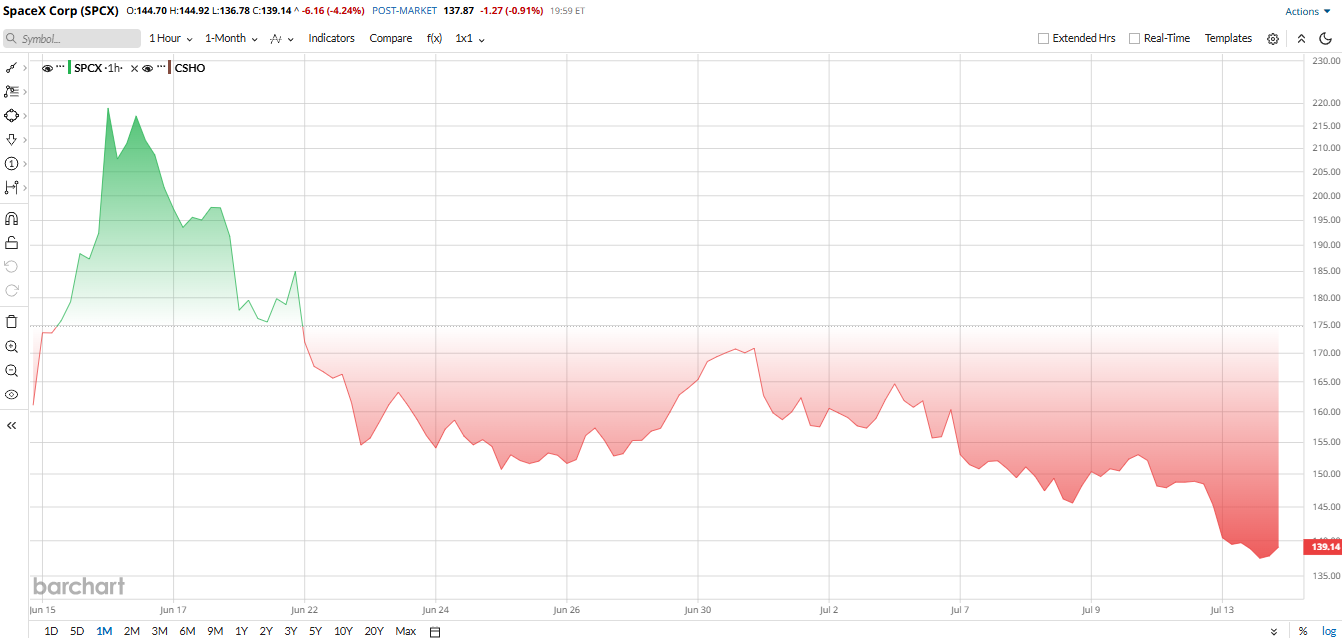

SpaceX went public in mid-June 2026 with an IPO price of $135 per share before opening around $150 in its market debut. Investor enthusiasm pushed the stock above $200 within days as demand overwhelmed supply and passive funds rushed to buy shares following index inclusion.

That momentum didn't last. SPCX had fallen to roughly $145, nearly 28% below its post-IPO peak, before sliding into the mid-$130s later in the month. The pullback came due to several reasons, e.g., profit-taking, broader weakness across technology stocks, and growing concerns that the valuation had become difficult to justify.

Noble's warning also gained traction as investors began discussing upcoming insider lockup expirations and the possibility of additional selling pressure entering the market. Short sellers have become increasingly active as well, with roughly 17% of the public float reportedly sold short, highlighting growing skepticism around the stock's near-term outlook.

The biggest argument against SpaceX today isn't its technology or long-term ambitions; it's the price investors are paying. Based on current trading levels, SpaceX trades at roughly 100 to 130 times sales, compared with about three times sales for the broader S&P 500 ($SPX). Its price-to-book ratio sits near 55 times, while enterprise value to EBITDA approaches an extraordinary 488 times.

Those multiples place SpaceX among the most expensive large-cap companies ever to reach public markets.

Starlink Continues to Shine Even as SpaceX Spends Aggressively

SpaceX's first quarterly report as a public company demonstrated exactly why investors remain excited about the business, while also highlighting why profitability remains a challenge.

First-quarter 2026 revenue climbed to $4.694 billion from $4.067 billion a year earlier as the company continued expanding across its major business segments.

Starlink remained the clear growth engine. The connectivity division generated $3.257 billion in revenue, about 69% of total company sales, and grew roughly 50% year-over-year (YoY). More importantly, the segment produced approximately $1.188 billion in operating profit, showing the satellite internet business is becoming a meaningful earnings contributor.

The picture looked very different elsewhere. Meanwhile, the launch business posted an operating loss of about $662 million, as SpaceX worked diligently on Starship, and the company's newer artificial intelligence (AI) unit had an operating loss of about $2.47 billion with heavy investment in research and infrastructure.

Overall, SpaceX posted a loss of $4,276 million on the bottom line, but it compared to a loss of $528 million for the same period last year. Adjusted EBITDA was also positive at $1.127 billion, although free cash flow remained very negative as the company plows capital into all areas of the growth. SpaceX's cash balance stood at some $16.6 billion at the end of the quarter following the use of a little over $8.5 billion in the quarter.

SpaceX Continues Expanding Starlink and More

Despite investor concerns over the stock, SpaceX's underlying business continues moving forward across multiple fronts.

The company is preparing the next Starship test flight after regulators cleared the program to resume launches following May's setback. The upcoming mission is expected to deploy next-generation Gen 3 Starlink satellites designed to increase network capacity and improve internet speeds.

Meanwhile, Starlink's commercial momentum continues to accelerate. The satellite internet platform reached roughly 10.3 million subscribers during the first quarter, more than doubling from the prior year as global demand remained strong.

SpaceX and xAI merged back in February to bolster the companies' AI ambitions and further worked towards launching “orbital data centers.”

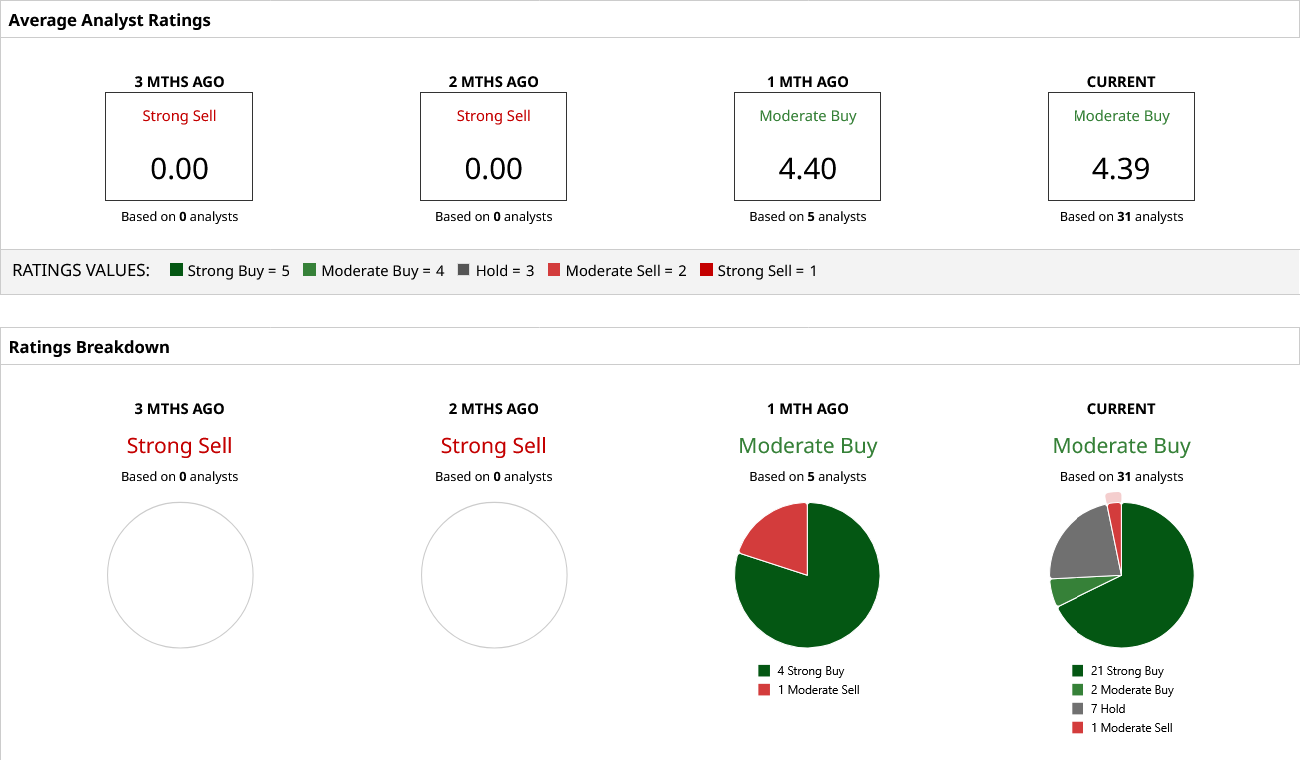

Wall Street Remains Optimistic Despite the Growing Valuation Concerns

Analysts generally agree that SpaceX possesses one of the strongest long-term growth stories in the market, even if opinions differ sharply on how much investors should pay for that opportunity.

Morgan Stanley initiated coverage with an “Overweight” rating and a $300 price target, arguing SpaceX occupies a unique position within global space infrastructure and AI. Oppenheimer lifted its target to $250 from $190, saying the company controls nearly every layer of the AI ecosystem through its expanding platform.

RBC Capital Markets also maintained an “Outperform” rating with a $225 target, pointing to SpaceX's long history of technological disruption despite acknowledging execution risks.

Not every analyst is quite as enthusiastic, with firms such as Stifel adopting more cautious price targets closer to $190.

Overall, Wall Street currently assigns SPCX stock a “Moderate Buy” consensus, with an average price target of roughly $235. That implies a massive upside of nearly 70% from current levels, suggesting analysts remain optimistic about the company's long-term prospects.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)