Wall Street’s bullish outlook on Apple (AAPL) just received another notable vote of confidence.

On Monday, Citi analyst Asiya Merchant raised her 12-month price target on Apple to $365 from $315 ahead of the company’s July 30 earnings report. This shows growing confidence that Apple’s AI strategy and resilient consumer demand can continue driving the stock higher through the second half of 2026.

The new target implies roughly 16% upside from current levels and comes as Apple continues to outperform the broader market. The world's largest company by market capitalization has benefited from stronger-than-expected iPhone demand, accelerating services revenue, and renewed enthusiasm around its expanding artificial intelligence initiatives.

The timing of Citi’s upgrade is particularly notable because investors are now looking toward Apple’s upcoming earnings report as well as the launch of the iPhone 18 in September.

Apple's Strong 2026 Rally Has Been Driven by Better Fundamentals

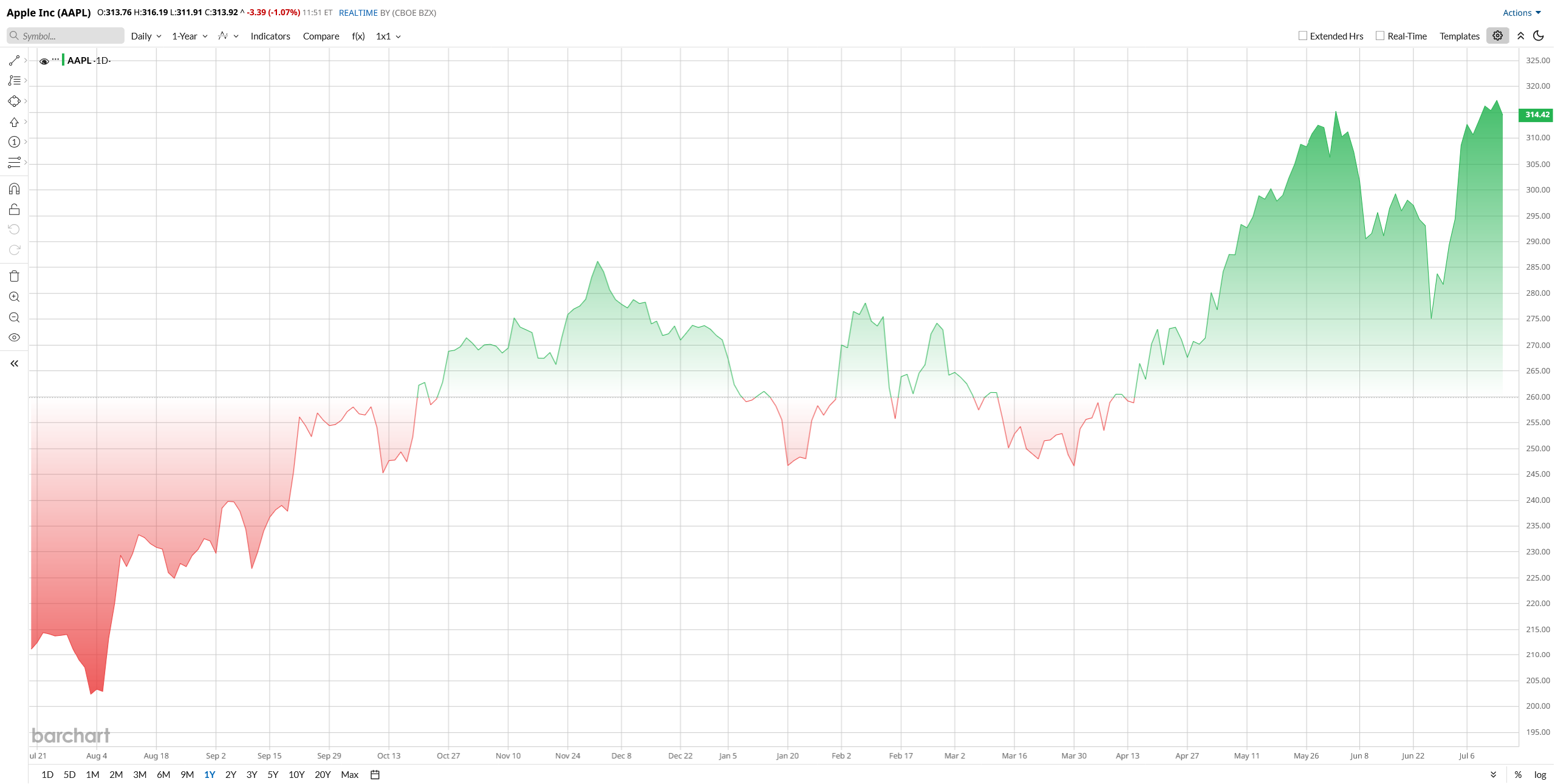

Apple has quietly become one of the strongest-performing mega-cap technology stocks this year after a difficult finish to 2025.

AAPL stock has rallied roughly 29% from its March lows and has climbed from the mid-$250s at the beginning of 2026 to around $317 by mid-July, representing a gain of roughly 16% year-to-date (YTD). Investors have become increasingly optimistic following stronger-than-expected iPhone demand, continued expansion in the high-margin services business, aggressive capital returns, and improving sentiment toward AI-focused technology companies.

Citi believes Apple's premium positioning continues to allow the company to gain market share even as global smartphone demand remains uneven. Merchant also expects Apple will retain pricing power, enabling it to offset higher component costs without materially hurting demand.

Despite the impressive rally, Apple continues to trade at a premium valuation compared to its own historical averages.

The stock currently trades at roughly 38 times trailing earnings, well above its five-year average multiple of around 30 times, suggesting investors are already pricing in meaningful earnings growth and continued AI-driven momentum.

Meanwhile, Apple's dividend yield remains modest at approximately 0.3%, meaning the investment case continues to rely primarily on earnings growth, expanding services revenue, and the company's massive share repurchase program rather than income generation.

Investors Will Be Watching Whether Apple Can Extend Its Earnings Momentum

Apple will report fiscal third-quarter results after the market closes on July 30, with Wall Street expecting another solid quarter.

Consensus estimates call for approximately $1.88 in earnings per share, representing roughly 20% year-over-year (YoY) growth, while revenue is expected to post another healthy increase led by continued strength in services and wearable devices.

The optimism follows Apple's impressive fiscal second-quarter results released in April. The company delivered $111.18 billion in revenue, up 16.6% YoY, while earnings reached $2.01 per share, increasing approximately 22% and comfortably exceeding Wall Street expectations. Revenue also topped analyst forecasts by roughly $1.7 billion, reinforcing confidence that Apple's ecosystem continues to generate resilient consumer demand despite a slower global smartphone market.

Management also guided fiscal third-quarter gross margins between 47.5% and 48.5%, suggesting Apple expects to successfully manage higher memory costs while preserving profitability.

AI Strategy Extends Beyond Siri

The Apple Intelligence platform has garnered a lot of attention recently, particularly for its AI integration capabilities in Apple's software, but the company's vision goes beyond that.

Apple has inked a multi-year deal with Broadcom (AVGO) for custom AI silicon and new wireless technologies to bolster its push for more powerful on-device artificial intelligence capabilities. Meanwhile, Apple has incorporated ChatGPT's generative AI capabilities into Siri and other writing apps, meaning that users could enjoy some of the more sophisticated capabilities of this type of artificial intelligence while maintaining much of Apple's privacy-first design.

The investments show Apple's strategy to further engage users through its ubiquitous network of active devices, over $2.35 billion, and extend its higher-margin services business beyond hardware upgrades.

In the eyes of Wall Street, this “ecosystem” strategy could be a sustainable competitive edge as AI is increasingly embedded in consumer devices.

Analysts Continue Raising Their Expectations for AAPL Stock

Citi's target increase adds to a growing list of optimistic Wall Street forecasts ahead of Apple's earnings report.

Morgan Stanley recently described Apple as one of its top investment ideas, arguing that Apple Intelligence could accelerate future iPhone and iPad upgrade cycles. Goldman Sachs also lifted its price target to $340, citing continued momentum across iPhone, Mac, and services revenue. Evercore reiterated its $330 target after Apple's previous earnings beat, highlighting stronger-than-expected revenue and earnings execution.

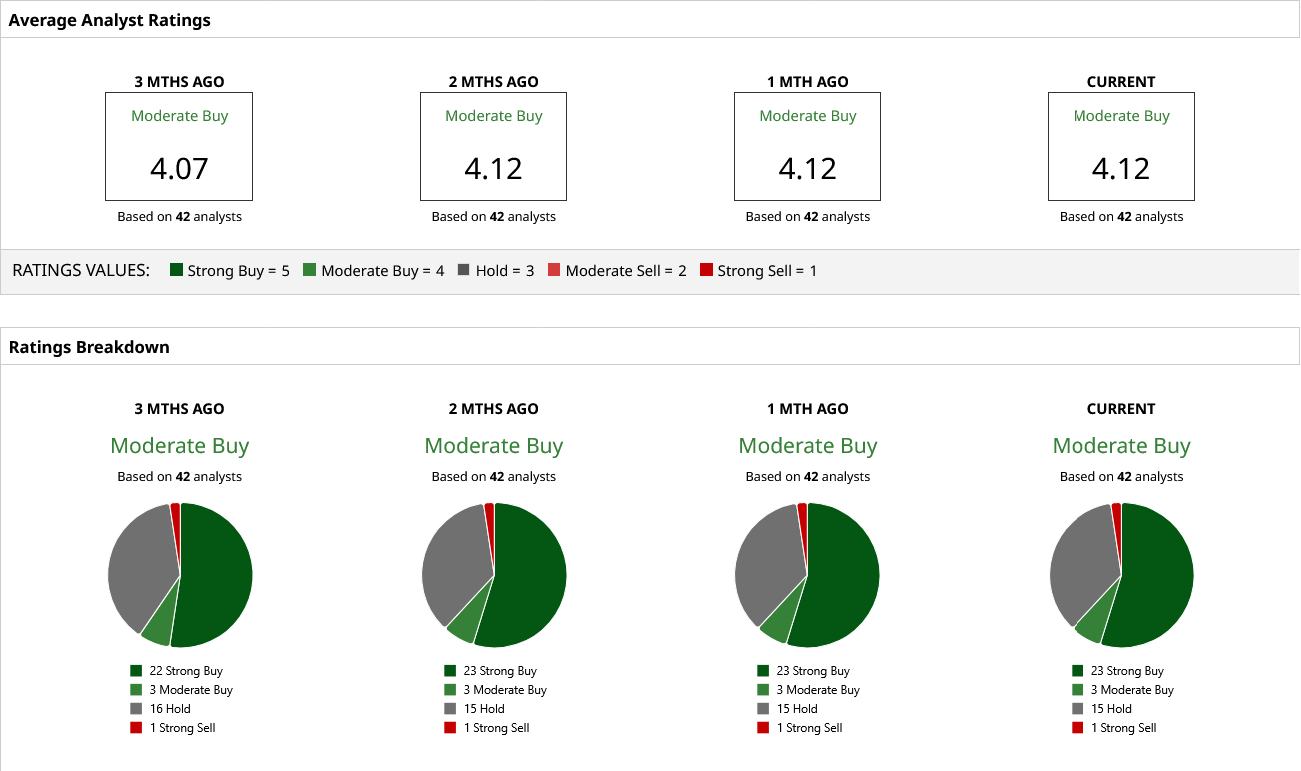

However, Wall Street rates AAPL a “Moderate Buy” overall. The current average analyst price target is $315.38, which the stock is quite close to right now. AAPL stock's Street high target is $400, still giving a possible 27% upside from here.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Space/Rocket%20takes%20off%20by%20Alones%20via%20Shutterstock.jpg)