/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Dell Technologies (DELL) is dealing with two very different trends right now. New industry data shows global PC shipments declined in the second quarter as rising memory and storage costs pushed PC prices higher and weakened demand. That news weighed on DELL stock because investors worry higher component costs could slow future PC sales. However, Dell still outperformed the broader market, shipping 9.3 million PCs and holding a 14% global market share.

At the same time, Dell's core business remains incredibly strong. In its latest quarter, the company easily beat Wall Street's expectations on both revenue and earnings thanks to booming demand for AI servers.

The stock has more than doubled over the past year as investors continue betting on Dell's AI infrastructure business. Strong support from the Trump administration also helped fuel this rally recently. Trump asked citizens to “go out and Buy Dell computers,” which popped Dell's shares even higher. But the question now is whether the stock has run too much or if there's still room to run. Let's find out.

Dell Is Gaining Market Share Despite a Weaker PC Market

The latest industry data isn't encouraging for the PC industry. Global PC shipments fell about 4% year-over-year (YoY) to 65.7 million units during the second quarter as memory and storage prices climbed 20% to 40%. Higher component costs forced manufacturers to raise prices, leading many customers to delay purchases after buying earlier in the year.

Dell, however, performed better than most competitors. The company shipped approximately 9.3 million PCs during the quarter and maintained a 14% share of the global market. That suggests Dell continues taking market share even while the overall industry slows.

The weakness appears to be industry-wide rather than company-specific. Dell's commercial customer relationships and enterprise focus have helped it outperform the broader PC market, although prolonged component inflation could still pressure demand over the coming quarters.

AI Business Continues to Drive Record Results

While the PC market faces challenges, Dell's AI infrastructure business continues to deliver mind-blowing results.

During its fiscal first quarter of 2027, Dell reported revenue of $43.8 billion, up 88% YoY, comfortably beating analyst expectations. GAAP earnings per share surged to $5.24, while adjusted EPS reached $4.86, also ahead of Wall Street estimates. Net income climbed 256% to $3.44 billion, and free cash flow reached roughly $3.2 billion.

The biggest growth driver remains Dell's Infrastructure Solutions Group. Revenue from servers and storage jumped 181% to $29 billion as enterprises continued investing heavily in AI infrastructure. Meanwhile, Dell's Client Solutions Group, which includes its PC business, generated $14.6 billion in revenue, up 17% from a year ago.

Management also raised its full-year outlook, now expecting approximately $167 billion in fiscal 2027 revenue while forecasting around $60 billion in AI server sales.

Beyond earnings, Dell continues expanding its AI ecosystem. The company recently introduced new high-density PowerEdge servers through its Dell AI Factory partnership with Nvidia (NVDA) while also increasing shareholder returns through a $0.63 quarterly dividend and continued share repurchases.

DELL Stock Isn’t Cheap Anymore

Dell's execution so far has been outstanding, but investors are paying a premium for that growth.

DELL stock trades at roughly 30 to 35 times forward earnings, far above traditional PC peers like HP. That higher valuation reflects investor expectations that Dell's AI server business can continue delivering exceptional growth for years.

If enterprise AI spending slows, customers delay infrastructure upgrades, or higher memory costs begin affecting margins, investors could become less willing to pay such a premium multiple.

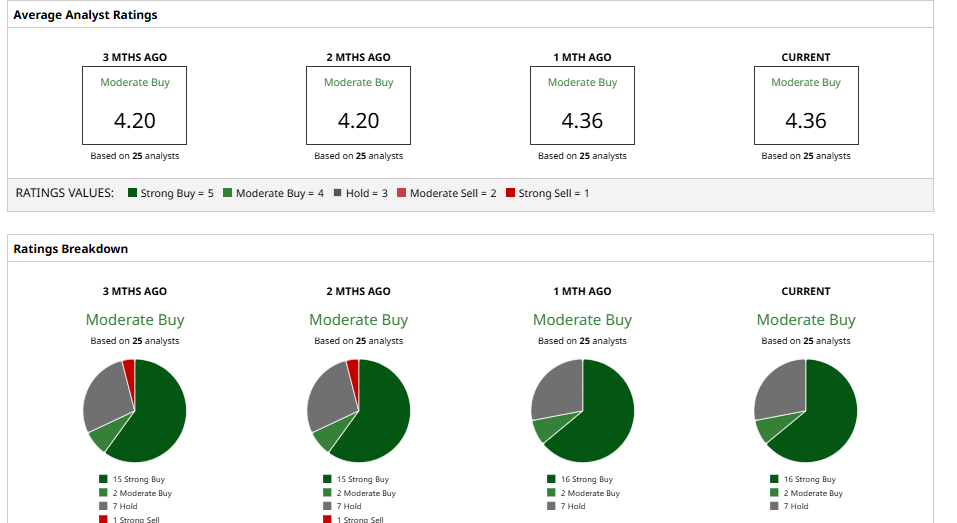

What Do Wall Street Analysts Think of DELL Stock?

Wall Street remains optimistic about Dell's long-term AI opportunity, although price targets suggest the upside may be more limited after the stock's huge rally.

Bank of America recently raised its price target to $246 and maintained a “Buy” rating. Evercore increased its target to $240 with an “Outperform” rating, while Citi lifted its target to $235 and also rates the shares Buy. Morgan Stanley remains more cautious with a $110 target.

Overall, analysts still rate DELL stock a “Moderate Buy.” After the bull run over the past year, the average 12-month price target of $489.14 is still giving 16% upside from the current share price, suggesting Wall Street believes much of the near-term AI optimism has room to grow.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)