/Ge%20Aerospace%20By%20Grand%20Warszawski.jpeg)

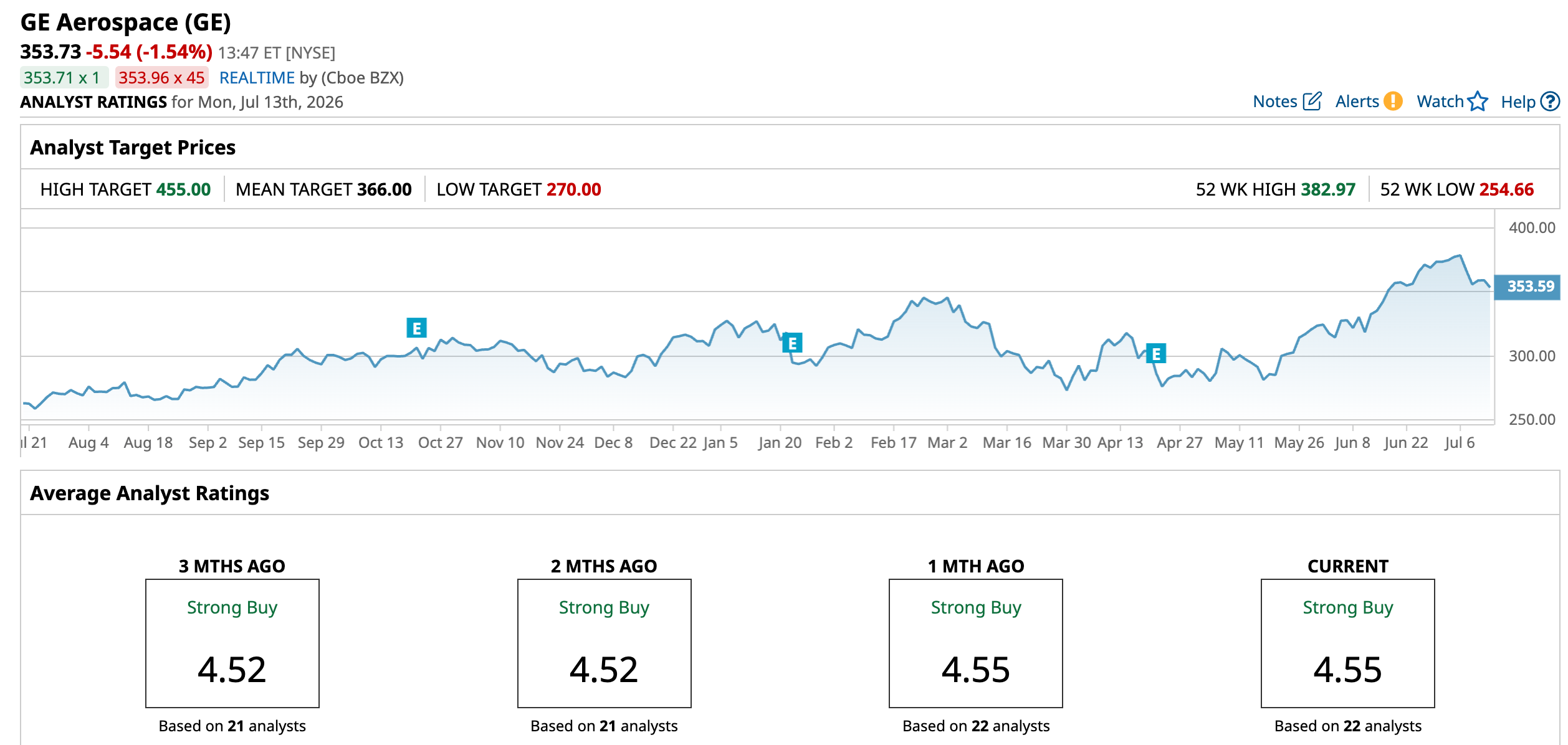

GE Aerospace (GE) is set to report its second-quarter 2026 earnings on Thursday, July 16. Strong demand across both commercial aviation and defense, and solid momentum across its high-margin aftermarket services business, has driven GE stock higher.

GE Aerospace designs and manufactures aircraft engines while generating recurring, high-margin revenue through long-term maintenance and service agreements. Its massive installed engine base creates a durable aftermarket business that delivers steady cash flow throughout the engine's life. With commercial air travel continuing to recover and defense spending rising, these structural tailwinds have led GE stock to hit an all-time high of $382.97 earlier this month.

The company entered the second quarter with considerable momentum. In Q1 2026, orders surged 87%, led by nearly a doubling in Commercial Engines & Services (CES) orders, while Defense & Propulsion Technologies (DPT) orders climbed 67%, marking the strongest defense order intake of the decade.

GE Aerospace’s revenue increased 29%, driven by robust services demand in CES and double-digit growth in DPT. Operating profit rose 18%, with both business segments delivering double-digit gains, while adjusted EPS climbed 25% to $1.86.

Heading into the Q2 report, GE Aerospace is likely to sustain its solid growth trajectory and could provide upbeat guidance. Another quarter of strong orders, services growth, and cash flow could strengthen the bullish investment case. However, with the stock already trading near record highs, valuation remains a concern.

GE Q2 Earnings: Can Aerospace Giant Deliver Another Earnings Beat?

GE Aerospace heads into its second-quarter earnings report with strong momentum, backed by surging demand for aircraft engine services, solid backlog, and resilient defense spending.

The company's Commercial Engines & Services (CES) business is expected to deliver solid growth. Airlines continue to invest in maintaining existing fleets amid recovery in global air travel demand, fueling higher demand for engine overhauls, spare parts, and long-term service agreements. This trend has translated into a commercial services backlog exceeding $170 billion, providing the company with strong multi-year revenue visibility.

Commercial services orders have climbed more than 30% over the past year, including an impressive 49% increase during the first quarter, reflecting the strength of the aftermarket business. Demand for spare parts also remains exceptionally strong. Spare parts, which account for a significant portion of the services revenue, have continued to outpace the company's ability to supply them.

Overall, order activity remains strong in the near term, and the momentum is likely to reflect in Q2. GE has 95% of its spare parts orders in backlog, and all planned shop visits for the quarter have been secured. As a result, service revenue will grow by the high teens in the second quarter.

The Defense & Propulsion Technologies (DPT) segment is also expected to contribute to quarterly growth, led by solid demand.

GE Aerospace has consistently outperformed Wall Street's expectations, delivering earnings beats in each of the past four quarters, including a 15.5% upside surprise in the fourth quarter of 2025. Profitability is also expected to improve during Q2. Wall Street currently expects second-quarter earnings of $1.86 per share, representing year-over-year (YOY) growth of 12.1%.

What’s Ahead for GE Stock?

GE Aerospace appears well-positioned to deliver another solid quarter, supported by its record services backlog, robust demand across commercial aviation, and a resilient defense business. These strengths should continue to support revenue growth and earnings momentum.

Nevertheless, much of this optimism is already reflected in the stock price. GE currently trades at a forward price-to-earnings multiple of 48.01 times, which is high. While Wall Street expects earnings to grow 17.4% in 2026 and another 15.9% in 2027, investors are already paying a significant premium for that growth.

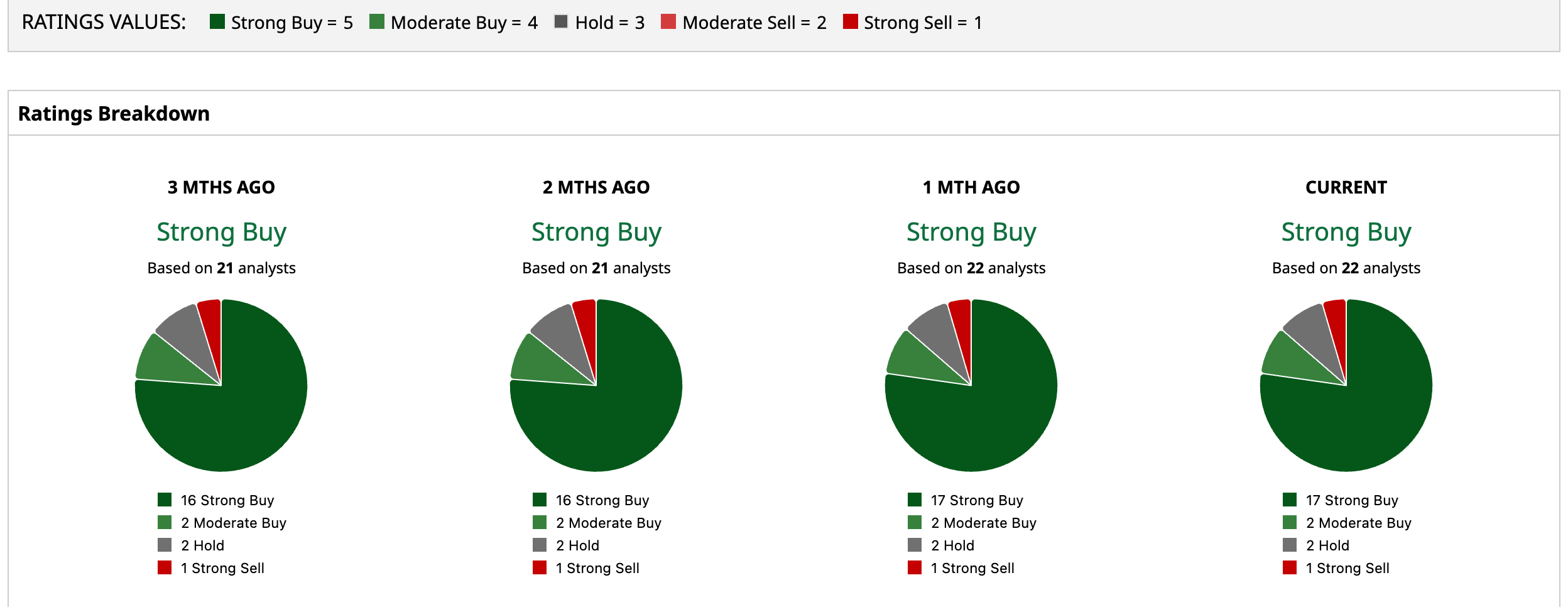

Overall, analysts remain bullish on GE Aerospace's prospects. However, given the stock's rich valuation, upside could remain capped until the company delivers a solid outlook, prompting analysts to raise their earnings forecasts.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)