/Applied%20Materials%20Inc_%20campus%20sign-by%20Sundry%20Photography%20via%20iStock.jpg)

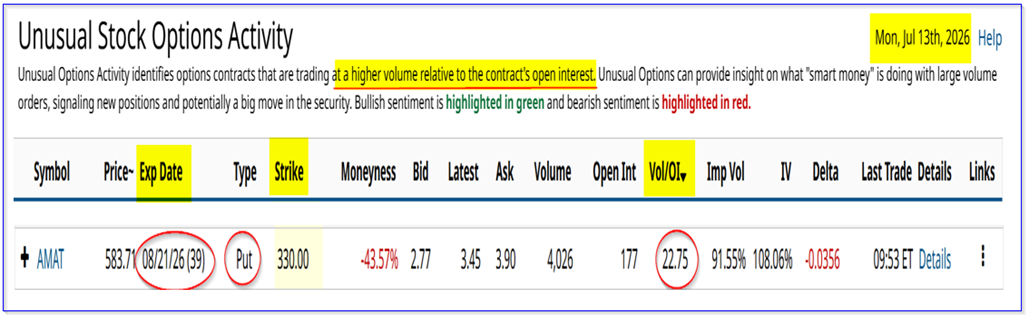

Applied Materials (AMAT), a semiconductor chip equipment and software maker, is showing highly unusual out-of-the-money (OTM) put options activity today. AMAT stock is off its highs. This could be a bullish signal ahead of earnings.

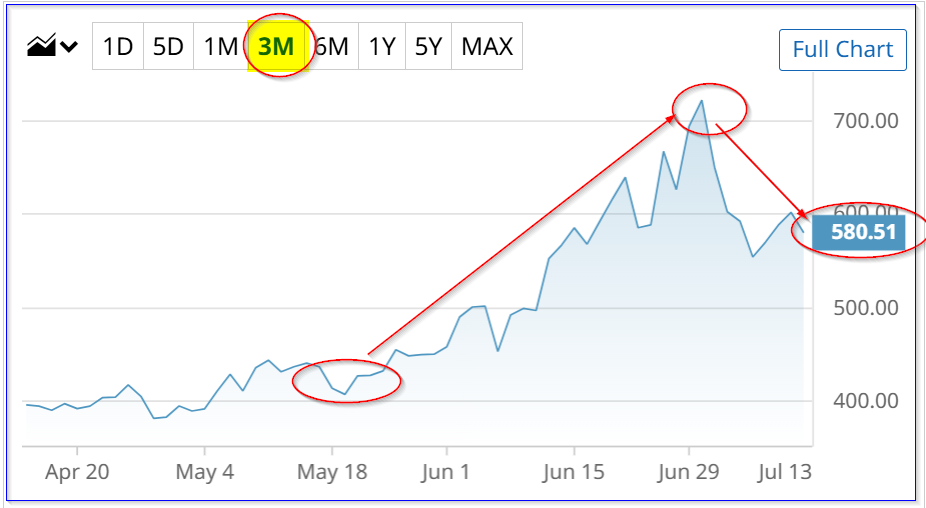

AMAT is down over 4.6% today at $575.11 per share. It's off from a peak price of $723.00 on June 30. However, since its last earnings release on May 14, where the company showed lower free cash flow (FCF), AMAT has risen over 30.5% ($440.56).

Applied Materials' fiscal Q3 earnings release is expected on Aug. 13. That's important in relation to today's unusual put option activity.

This involves a deep out-of-the-money (OTM) put contract expiring Aug. 21. That's a week after the upcoming Q3 earnings release.

Moreover, the strike price is $330.00, which is $245.11 lower than today's price, i.e., -42.6%.

So, buyers of these puts expect AMAT to tank after its upcoming earnings release. They must be expecting that the company will show extremely lousy results.

Or maybe Applied Materials will show negative free cash flow (FCF). That's the only way AMAT might tank this far. But is that likely? Probably not.

As a result, today's unusual put options activity is actually a bullish signal.

It shows that over 4,000 put contracts have traded at $330.00, almost 43% lower than today's price. Let's look further into what is going on with Applied Materials.

Applied Materials Free Cash Flow (FCF) Projections

Last quarter, due to heavy working capital, tax, and legal payments, Applied Materials posted lower cash flow. This was what the company said on page 21 of its earnings presentation.

So, it seems reasonable to assume the dip in free cash flow (FCF) last quarter was a one-time event (i.e., it posted just $210 million in FCF compared to $1.06 billion last year and $1.04 billion in the prior quarter).

As a result, analysts' higher revenue projections could lead to higher FCF. For example, Seeking Alpha reports that analysts are now projecting Q3 revenue of $9.01 billion for Q3 (ending July 28, 2026). That will be 23% higher than last year's $7.3 billion revenue.

Moreover, last year the company generated $2.05 billion in FCF, representing 28.07% of its revenue, according to Stock Analysis. So, if Applied Materials were to generate 28% of $9.01 billion in Q3 2026, FCF could exceed $2.52 billion.

If that occurs, don't expect AMAT stock to keep falling. In fact, as long as AMAT achieves at least a 20.35% margin over its trailing 12 months (TTM), which was its TTM FCF margin last year, the stock could stabilize (Stock Analysis data). Last quarter, the TTM figure was slightly lower at 18.41%.

Price Targets for AMAT Stock

Using analysts' revenue projections for the next 12 months (NTM), and applying a 20.3% FCF margin shows that AMAT may be too cheap.

For example, Seeking Alpha reports that the average analyst revenue forecast for the year ending October 2026 is $33.42 billion and $42.47 billion for next year. That means the NTM revenue average is $37.95 billion (compared to $28.37 last year, i.e., +33.7%).

So, assuming Applied Materials makes at least a 20.3% FCF margin, FCF could rise to $7.7 billion:

$37.95b NTM revenue est. x 20.3% = $7.704 billion FCF

That is 35% more than the $5.698 billion in FCF in 2025, and 44.2% higher than the $5.343 billion in TTM in Q1.

Since Yahoo! Finance shows that AMAT's market cap is $455.14 billion. That means that if Applied Materials were to pay out 100% of the past year's FCF, the yield would be 1.17%:

$5.323b / $455.14b = 0.01174 = 1.174% FCF yield

So, applying this to the NTM forecast, the potential market cap is $658.5 billion:

$7.704b / 0.0117 = $658.5 billion fair market value (FMV)

That is 44.5% higher than today's price. In other words, the price target (PT) for AMAT stock, based on its projected FCF, is over $831 per share:

$575.11 x 1.445 = $831.03 PT

Other analysts have higher price targets, although not as high as mine. Yahoo! Finance's survey shows a PT of $612.20 from 39 analysts, and Barchart's is $621.74. AnaChart's survey price is $561.98 from 23 analysts. The average of these three is $598.64, or 4% higher than today's price.

The bottom line is that these PTs show AMAT stock is too cheap.

Summary and Conclusion

That could be why the initiators of today's deep out-of-the-money (OTM) puts may be short-sellers. The premium they receive is $2.77 at the bid price and $3.45 at the latest price. That represents a short-put yield of 1.0% (i.e., $3.45/$330.00).

Moreover, the potential buy-in point is $326.55 (i.e., $330.00 - $3.45), or 12.94% lower than today's price.

That gives these short-sellers an attractive buy-in point, even if AMAT stock falls after the Aug. 13 earnings release. Moreover, the potential upside is high, assuming it reaches even analysts' $598 price target:

$598.64 / $326.55 -1 = 0.8388 = +88.9% upside

Even if there is only a 50% probability of this occurring, the expected return is 45%, a very attractive potential upside. That shows why today's unusual puts in AMAT stock are attractive to short-sellers.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)