/AI%20(artificial%20intelligence)/AI%20data%20center%20infrastructure%20by%20FOTOGRIN%20via%20Shutterstock.jpg)

Rackspace Technology (RXT) is a company that's really come onto the scene in recent months. This is thanks to a high-profile partnership with Palantir (PLTR) to roll out Rackspace's proprietary operating model framework. It will govern private cloud, sovereign cloud, on-premises infrastructure, and other key platforms that require data, governance, security, and outcome control.

The ability for Rackspace to essentially integrate its core technology into Palantir's Foundry and Artificial Intelligence Platform (AIP) technologies makes Rackspace's offerings immediately more valuable. Therefore, this stock's movement during recent months makes sense.

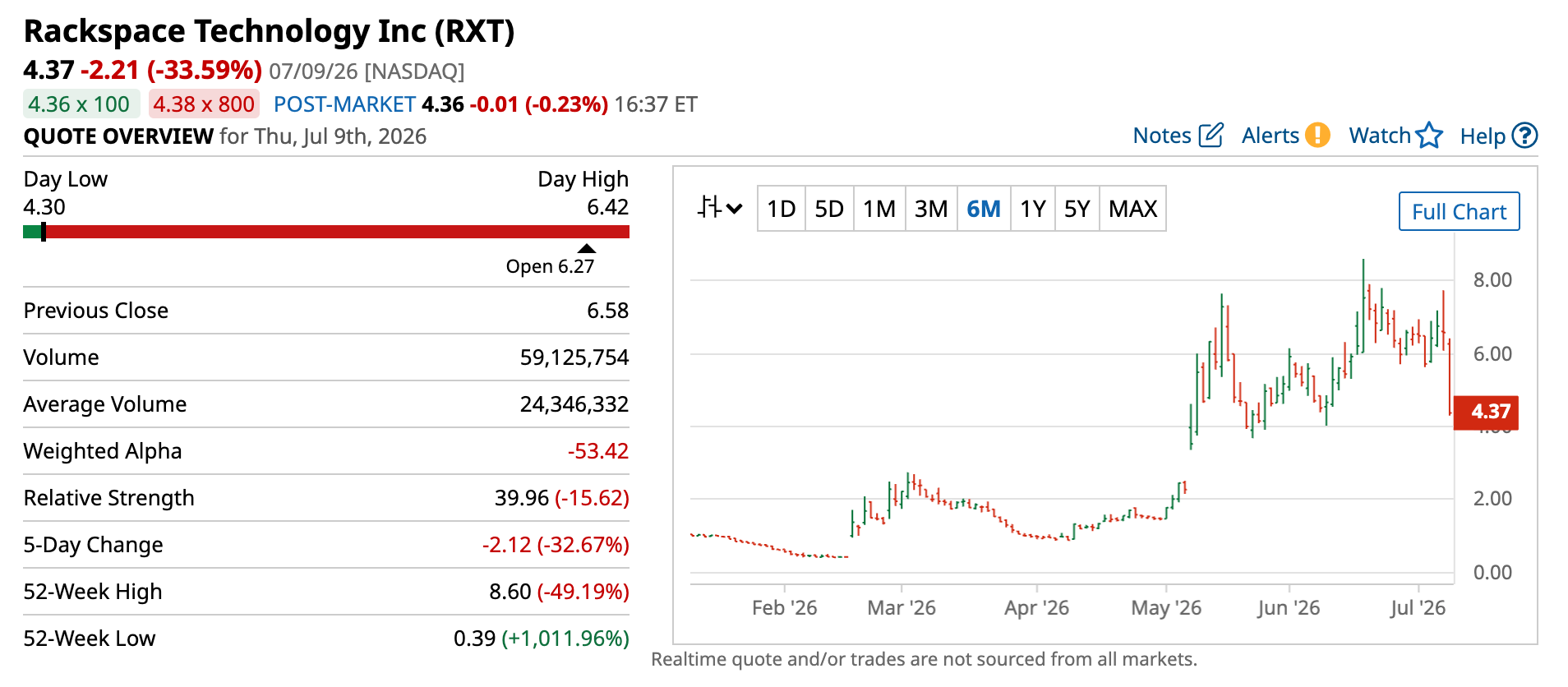

Nevertheless, after hitting a high of $8.60 per share in mid-June, RXT stock is back below the $5 level. Investors are now wondering whether this level is worth jumping on, or if this decline is likely to continue.

These questions have come to the fore even more of late, considering Rackspace's management team just announced it expects the framework provider's revenue to be $154 million light in 2026, with EBITDA likely to come in around $20 million lower than previously expected.

Why This Downgrade Matters

If this AI hype train (or bubble) was as powerful as many prognosticators have indicated, such revenue and earnings downgrades wouldn't be taking place. Indeed, for a company that's partnered with one of the most important companies in the AI race in Palantir, this earnings revision is one that does appear to have caught some investors offsides.

We'll have to see if Rackspace's management team is trying to sandbag its recent results, in order to set the table for a rock solid 2027.

Even so, given the pace at which companies like Rackspace have been able to grow, a slowing of growth in this specific early-stage AI company doesn't portend well for the industry as a whole. At least, that's my take on the market's reaction to RXT stock right now.

What Do the Fundamentals Suggest?

As an early-stage AI-focused company, one could argue that Rackspace's fundamentals don't matter. In a way, they don't.

This is a company without any meaningful GAAP earnings, though there did exist a pathway to profitability (and some free cash flow on the books). As such, one could make the argument that Rackspace is in a better financial position than most of its peers in this space. That's a fair assessment, with some strong underlying growth-driven fundamentals to point to as reasons to own this name at this stage of the AI market expansion.

Now, that's not to say that risks don't abound. In fact, they are everywhere. Whether or not we're analyzing mega-cap names like Palantir or the plethora of smaller companies looking to grab a slice of this quickly-expanding pie, it doesn't matter. Valuations are dropping as investor expectations around overall growth rates (and the amount of compute we'll ultimately need to power this revolution) quickly change.

Are Wall Street Analysts Still Bullish On Rackspace?

Overall, Wall Street analysts don't appear to be willing to throw in the towel on Rackspace, or the entire AI complex just yet.

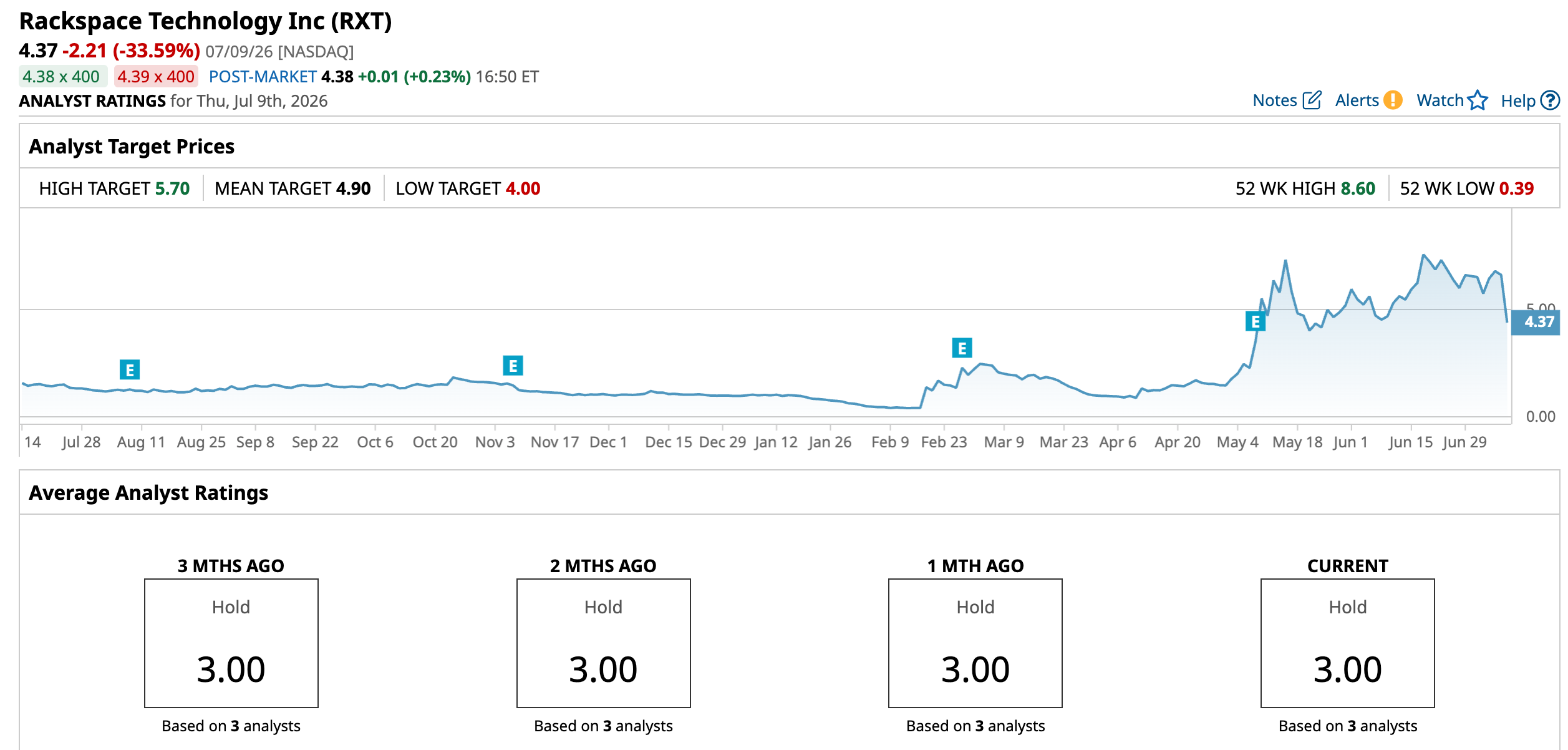

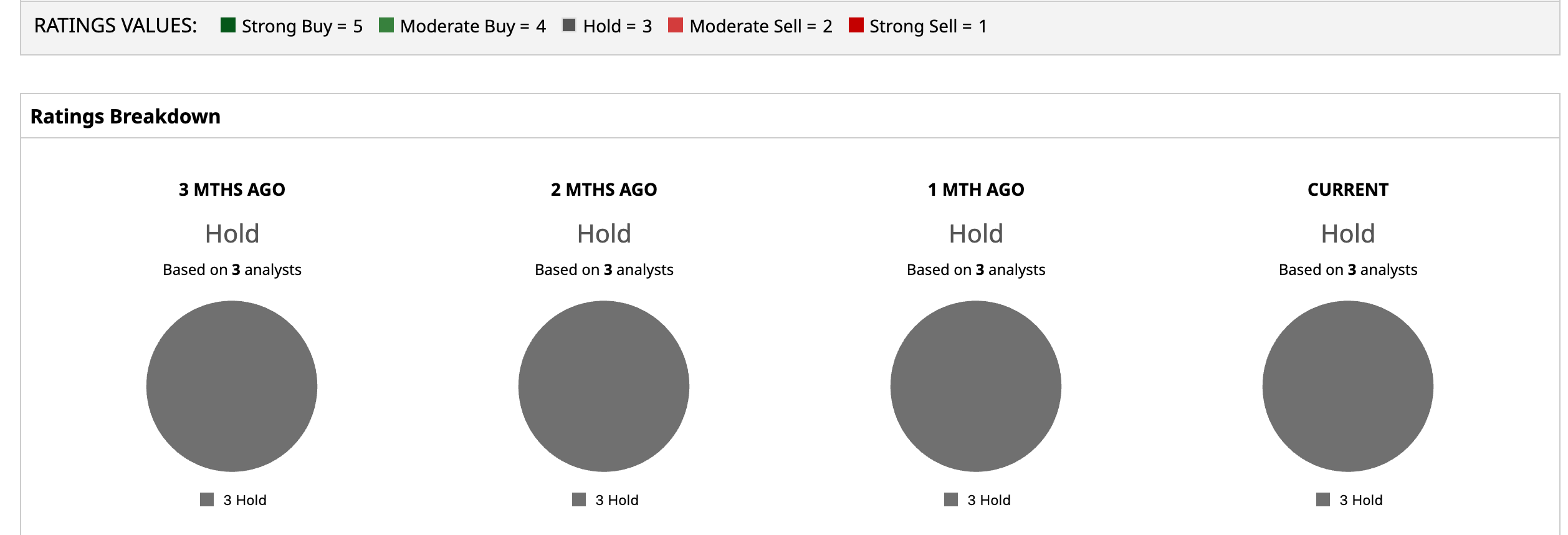

In fact, the three analysts covering RXT rate it a solid “Hold” and still have 12% upside built into their models for the stock, with the mean target price of $4.90. And the Street-high price target of $5.70 implies a potential of 30.4% upside from here.

I do think that companies like Rackspace that are still very early to the AI super cycle, and are building a name for themselves (with a growth road map that isn't as clear as other names in this developing sector) will provide both the highest risk, and highest upside, AI stocks have to offer. As such, I'm more inclined to “take the over” on Rackspace's prospects moving forward relative to its risk profile just yet.

Of course, some value-conscious and fundamentally-oriented investors simply may not place any investable dollars into a company like Rackspace until we see some EBITDA profitability and GAAP earnings. That makes sense. But for those looking to catch a major trend on the upswing, and are willing to put some speculative dollars to work in high-quality companies with world-class partnerships in the AI space, RXT stock is starting to look attractive (at least to me) right now.

On the date of publication, Chris MacDonald did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)