As investors and traders, we all spend a lot of time focusing on tactics. In the case of this article, consider it a complement to all of those ideas. Because stock picks, exchange-traded fund (ETF) trades, options setups, and the rest will only get you so far. If you don’t have a strategy.

To me, the most indispensable part of any strategy is to decide the answer to this simple question:

For every $100 I have invested, how much can I see it drop before I will become very uncomfortable?

We never want investing to become emotional. But if you are human, as I assume you are, it will happen. And it is more likely to occur if you didn’t have a premeditated concept of what would cause you to go into at least a little bit of a panic.

Identifying Your Risk Level

When I was much younger, the idea of losing $20 out of every $100 I had invested was no big deal. So what? Now, in my early 60s and semi-retired, my figure is closer to $5. That is, if my total portfolio drops by more than 5%, I’m going to be very angry. And I’ll have only one person to blame — myself!

Now, if you’re thinking that 5% is a bad two or three days in the stock market, which can happen at any time, that’s correct. So do note that my own portfolio is set up so that that 5% limit is more reasonable because I hedge most of my equity exposure against disaster. And I have a zero-coupon U.S. Treasury bond ladder, which I’ve written about here before, which has allowed me to lock in close to a 5% return on a large part of my portfolio.

Think of it this way. If, say, half of your portfolio is invested at 5% in bonds maturing at specific dates in the future, apart from the ever-present risk of inflation, your “nominal” return on the whole portfolio will be 2.5%, plus or minus how you do on the rest. I can lose 15% on a stock portfolio, average that in with my +5% on the bonds, and that’s a 5% loss.

This is what pre-determined parameters are about. And there are many ways to add some cushion around your stock market activities. In fact, I’ve argued for years that the best thing about things like bond ladders and equity portfolio hedges is that it allows me to be that much more aggressive with the rest of the asset base.

This is something that many newer investors are not taught to think about. Until now. It is the single most important rule I live by:

Manage risk like your life depends on it, with an absolute focus on ABL (Avoiding Big Loss).

How do you do that? There are many ways, but here is one.

Buying Put Options

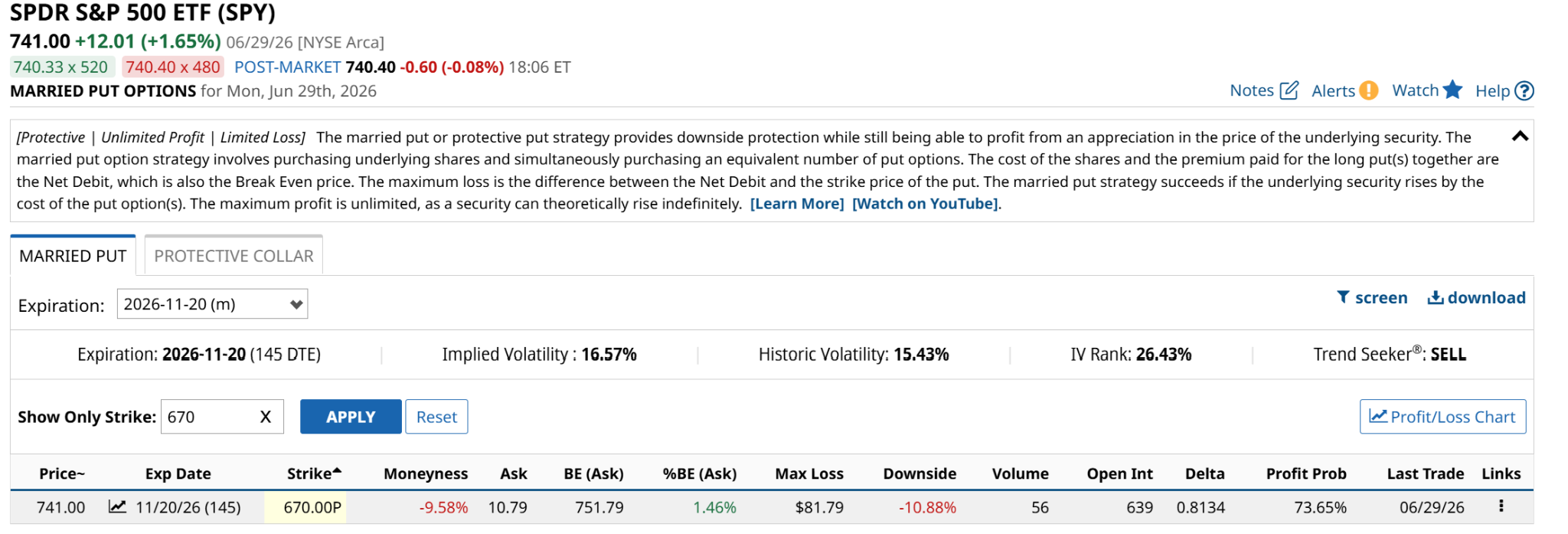

This is the simplest example I can think of to represent something I do actively to reduce the risk of the risk I’m taking in the stock market. It involves buying put options on the SPDR S&P 500 ETF (SPY) or other major market indexes. Just in case.

Let’s assume I own 100 shares of SPY. That’s currently worth roughly $74,000. If the market falls by 20% from here, that’s going to turn that into about $59,000. That’s $15,000 I could wait months, years, a decade, or longer, just to recover that short-term decline. That’s what market history tells us.

Is it worth paying about $1,100 now to put an ironclad low on that $74,000 of value at $67,000 from now until Nov. 20, which I intentionally chose to be after the U.S. midterm elections? I can’t answer that for you, but I suspect many investors would consider it. I do that type of active hedging all the time. Part of that is “laddering” my put hedges, if you will.

The Bottom Line

The decision is ultimately this: Is it worth $1,100 (the cost of the put options is $10.79 per contract, and one contract represents 100 shares of SPY) to know that my $74,000 can’t be worth less than $67,000 by late November? Since markets are capable of losing one-third of their value in a span of seven weeks (2020), or 25% in nine months (2022), or nearly 20% in six weeks (2025), something along those lines will appeal to more risk-averse types like me.

This is not about confidence in the stock market, or lack thereof. It is all about who you are as an investor. The more you self-diagnose in that regard, as the manager of your own money, the more prepared you are to play defense alongside your offense.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)