/Financial%20chart%20candlestick%20forex%20market%20screen%20background%20by%20Who%20is%20Danny%20via%20Adobe%20Stock.jpeg)

With a market cap of $24.5 billion, First Solar, Inc. (FSLR) is America's leading photovoltaic (PV) solar technology and manufacturing company and the only U.S.-headquartered firm among the world's largest solar manufacturers. The company develops advanced thin-film PV technology in its California and Ohio R&D labs, offering a high-performance, responsibly produced alternative to conventional crystalline silicon solar modules while maintaining an integrated manufacturing process independent of Chinese crystalline silicon supply chains.

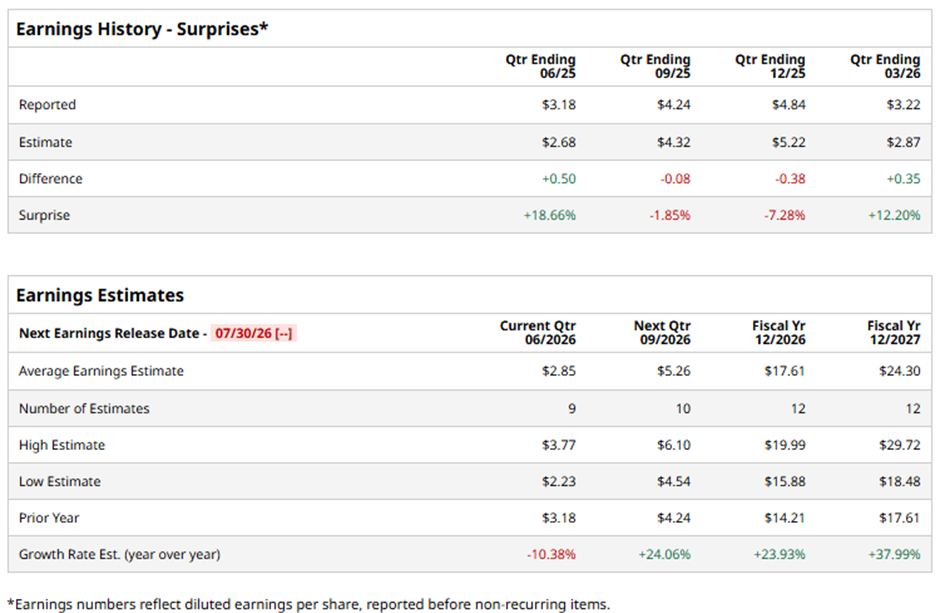

The Phoenix, Arizona-based company is slated to announce its fiscal Q2 2026 results soon. Ahead of this event, analysts expect FSLR to report a profit of $2.85 per share, a 10.4% decline from $3.18 per share in the year-ago quarter. It has exceeded Wall Street's earnings expectations in two of the past four quarters while missing on two other occasions.

For fiscal 2026, analysts project the largest U.S. solar company to report EPS of $17.61, an increase of 23.9% from $14.21 in fiscal 2025. In addition, EPS is anticipated to climb nearly 38% year-over-year to $24.30 in fiscal 2027.

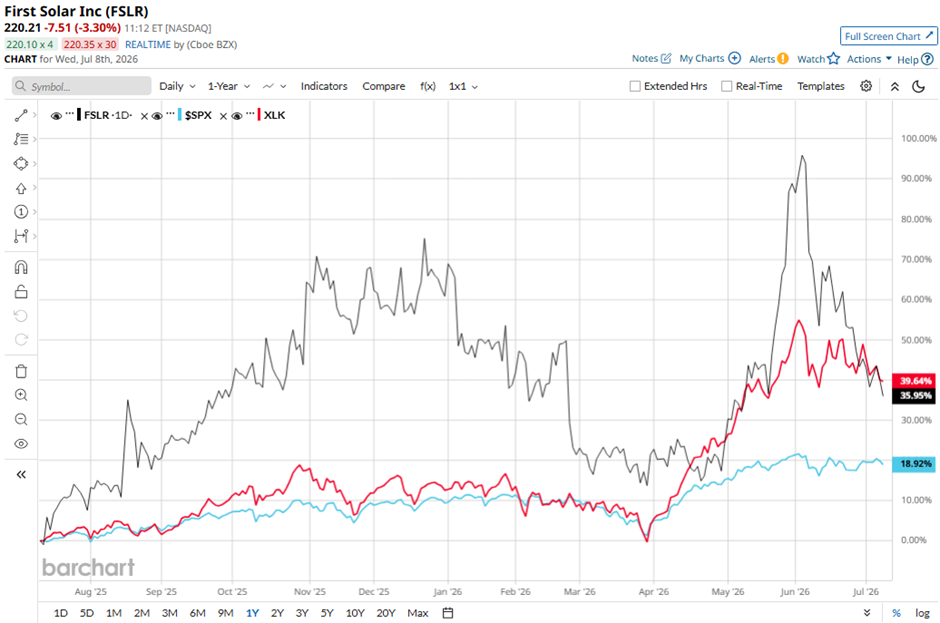

Shares of First Solar have soared 35.9% over the past 52 weeks, outperforming the broader S&P 500 Index's ($SPX) 19.9% gain. However, the stock has lagged behind the State Street Technology Select Sector SPDR ETF's (XLK) 40% return over the same period.

First Solar's shares rose 4.9% following its Q1 2026 results on Apr. 30 after the company reported record Q1 2026 revenue of $1.04 billion, up from $844.6 million a year earlier and in line with Wall Street expectations, while net income increased 65.4% year-over-year to $346.6 million. Investor sentiment was further supported by management's strong outlook, including Q2 module sales guidance of 3.4 GW - 4 GW and adjusted EBITDA of $400 million - 500 million, alongside record sales in India and meaningful margin expansion.

Additionally, higher U.S. tariffs and stricter trade enforcement on imported solar panels strengthened First Solar's pricing power by driving developers toward domestic suppliers, reinforcing confidence.

Analysts' consensus view on FSLR stock remains cautiously optimistic, with an overall "Moderate Buy" rating. Out of 33 analysts covering the stock, 17 recommend a "Strong Buy," three "Moderate Buys," 10 give a "Hold" rating, and three have a "Strong Sell." The average analyst price target is $252.93, suggesting a potential upside of 14.9% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)