Wolfspeed (WOLF) has spent the last year trying to convince investors that its turnaround story is real. Its overhaul included new leadership, a reorganized go-to-market plan, and a major debt deal — all supposed to change the narrative. However, Wall Street does not appear to be buying it. Not yet, anyway.

A growing crowd of short sellers is betting the silicon carbide wafer maker still has a long way to go before it proves it can turn profitable. Let's take a closer look.

Wolfspeed Tops List of Wall Street's Most Shorted Stocks

According to reports, Wolfspeed currently holds the top spot among heavily shorted U.S. stocks with market values above $2 billion. Almost 54% of its available shares are sold short, putting it well ahead of SoundHound AI (SOUN) and Intellia Therapeutics (NTLA).

The most shorted names on Wall Street often tend to cluster in software and biotech, which are industries known for ongoing losses, rich valuations, and heavy reliance on future growth rather than current profits. Wolfspeed, a semiconductor company, stands out from this crowd because its bear case is less about hype and more about basic math: How much cash is coming in versus how much is going out?

Wolfspeed makes silicon carbide chips and materials used in electric vehicles (EVs), industrial equipment, aerospace and, increasingly, AI data centers. According to the company, its mission is to power what it calls the "most disruptive innovations" through its silicon carbide platform.

Wolfspeed Stock Is Still Unprofitable

For the third quarter of fiscal 2026, Wolfspeed reported revenue of $150 million, which was in line with guidance according to CEO Robert Feurle. However, revenue was roughly flat compared with recent quarters, which is not a great sign for a company that needs growth to outpace its costs.

Wolfspeed reported a gross margin of -27% in Q3, wider than its -12% margin reported in the year-ago period. A negative gross margin indicates that Wolfspeed loses money on every chip it makes before we account for operating overheads.

CFO Gregor van Issum pointed to factory underutilization — roughly $46 million worth in the quarter — as the main culprit. In Q3, adjusted EBITDA landed at -$62 million while operating cash flow was -$84 million. Management expects Q4 2026 revenue between $140 million and $160 million, with gross margin remaining negative.

A Debt Overhaul Buys Wolfspeed Time, Not Certainty

To be fair, Wolfspeed did make one significant move during the quarter. It refinanced part of its expensive first-lien debt through a private placement that raised about $476 million in new convertible notes, stock, and warrants. The deal cut the senior secured note balance by roughly 43%, reduced total debt principal by about $97 million, and is expected to lower annual interest expense by around $62 million, according to van Issum.

Long-term debt fell from about $6.5 billion a year earlier to $1.7 billion. Total shareholder equity swung from deeply negative territory back to a positive $1 billion, helped partly by a Committee on Foreign Investment in the United States (CIFUS) clearance tied to Renesas (RNECY). Cash and short-term investments stood at roughly $1.2 billion at quarter-end, which gives Wolfspeed some runway, given its first debt maturity will begin in 2030.

Wolfspeed's balance sheet looks healthier than it did a year ago, largely due to lower debt levels. Total assets dropped sharply to $3.1 billion from about $6.85 billion in June 29, 2025, reflecting the accounting reset that accompanied the bankruptcy restructuring.

Is WOLF Stock a Good Buy?

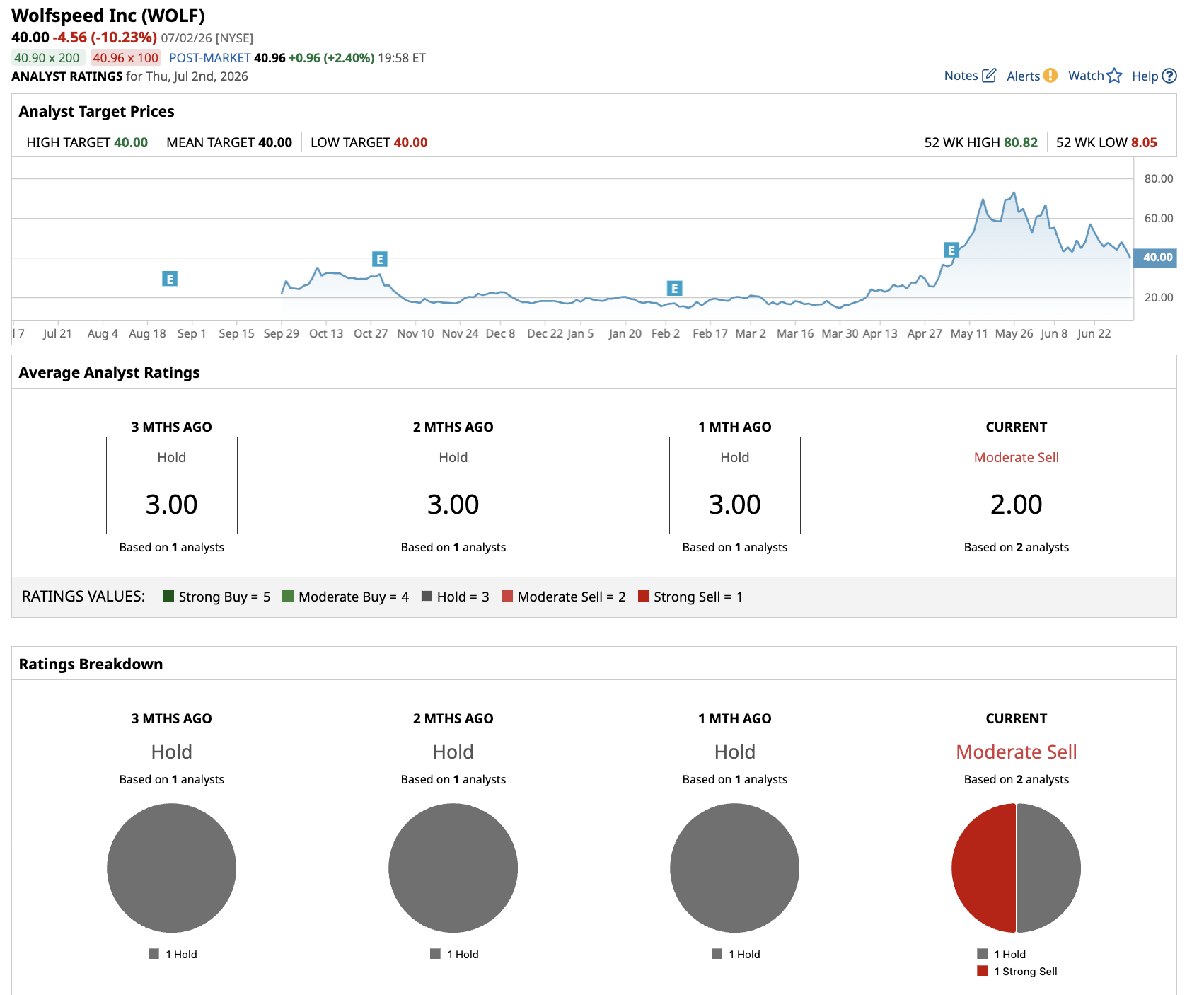

Overall, WOLF stock has a consensus “Moderate Sell” rating on Wall Street. Out of the two analysts covering the stock, one recommends a “Hold” rating while the other recommends a “Strong Sell." The average price target of $40 represents potential upside of 11% from current levels.

A combination of shrinking assets, persistent losses, and ongoing cash burn is what short sellers cite when they argue that a stock is overvalued relative to its risk. Wolfspeed's refinancing did not fix the underlying problem of a factory running well below capacity and a gross margin still in negative territory. Until the company shows a full quarter of positive gross margin and shrinking cash burn, expect the short interest crowd to stick around.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)