/Abstract%20close%20up%20electronic%20circuit%20board%20mainboard%20by%20pinglabel%20via%20Adobe%20Stock.jpeg)

Intel Corporation (INTC) has returned to being one of the most watched semiconductor stocks by Wall Street once again as HSBC raised its price target by 100% to $200, the highest target on the street. The broker kept its "Buy" recommendation, citing expectations of the positive development of the server CPU segment and the foundry business that is not yet priced in. INTC stock has gained more than 470% since reaching its 52-week low.

HSBC is making a bullish call amid the accelerating spending in the infrastructure of artificial intelligence (AI). While Nvidia Corporation (NVDA) has been dominating in AI graphics processing units, spending on CPUs, advanced packaging, and semiconductor manufacturing capacity becomes an increasingly crucial part of the AI supply chain. In this respect, HSBC believes that Intel can benefit from all three trends.

About Intel Stock

Intel Corporation is one of the largest semiconductor firms, producing processors for PCs, servers, networking devices, and AI workloads. It is increasingly manufacturing chips for other customers via Intel Foundry Services. The company has its headquarters in Santa Clara, California, and currently has a market cap of approximately $614 billion.

Although experiencing a modest retreat the past week, today in particular it is down over 10%, INTC remains among the best-performing stocks on the market over the last year. At the current level of around $108, the stock rose about 478% from its 52-week low of $18.97, but it is still lagging about 23% from its 52-week high of $142.35. The outperformance of the stock is driven by expectations of Intel's turnaround following Lip-Bu Tan's appointment to the CEO position.

However, the valuation already reflects great expectations. The company is trading at approximately 190 times forward earnings and 11.4 times sales, which are substantially above historical levels for diversified semiconductor companies. These multiples suggest that the market expects significant earnings acceleration from the company over the upcoming years. HSBC thinks that analysts' consensus estimates are too conservative as they fail to consider Intel's foundry business.

Intel Beats on Earnings

The latest quarterly earnings continue to prove the narrative of management. In the first quarter of 2026, Intel reported revenue growth of 7% year-over-year (YoY) to $13.6 billion, with non-GAAP EPS rising more than double to $0.29 as compared with $0.13 in the same quarter a year ago. The gross margin was also higher at 41.0% on a non-GAAP basis due to growing operational efficiency.

Intel guided Q2 revenue between $13.8 billion and $14.8 billion and non-GAAP EPS of approximately $0.20. Even though the guidance suggests some deceleration, management remains upbeat about future demand for AI infrastructure. CEO Lip-Bu Tan stated that the next wave of AI will become increasingly dependent on CPUs, wafer manufacturing capacity, and advanced packaging technologies as opposed to just GPU accelerators.

HSBC believes that the opportunity is much greater than is currently recognized by the market. For instance, analyst Frank Lee increased his 2026 server CPU shipment growth forecast from 20% to 25%, while 2027 is forecasted to be 30%. Moreover, HSBC projects 2026 revenues of the Data Center & AI division at $24.1 billion, 4% higher than Wall Street consensus. His estimate for 2027 revenue is $33 billion, which is 20% higher than the consensus estimate.

Even more importantly, HSBC became increasingly confident about the foundry business of Intel. For the first time, the firm has incorporated Intel Foundry Services in its valuation model, as the increased demand for alternative semiconductor manufacturing capacity, alongside restrictions on advanced packaging capabilities, can be a driver of substantial earnings. Intel has already won contracts with its foundry customers, such as Apple (AAPL) and Terafab, while discussing agreements with Google (GOOG) (GOOGL) and Nvidia. Additionally, HSBC highlighted the EMIB packaging technology of Intel, which has greater scaling potential. According to the sensitivity analysis of the firm, wider adoption of EMIB alone can add 23% to Intel's 2028 EPS versus the base case assumptions.

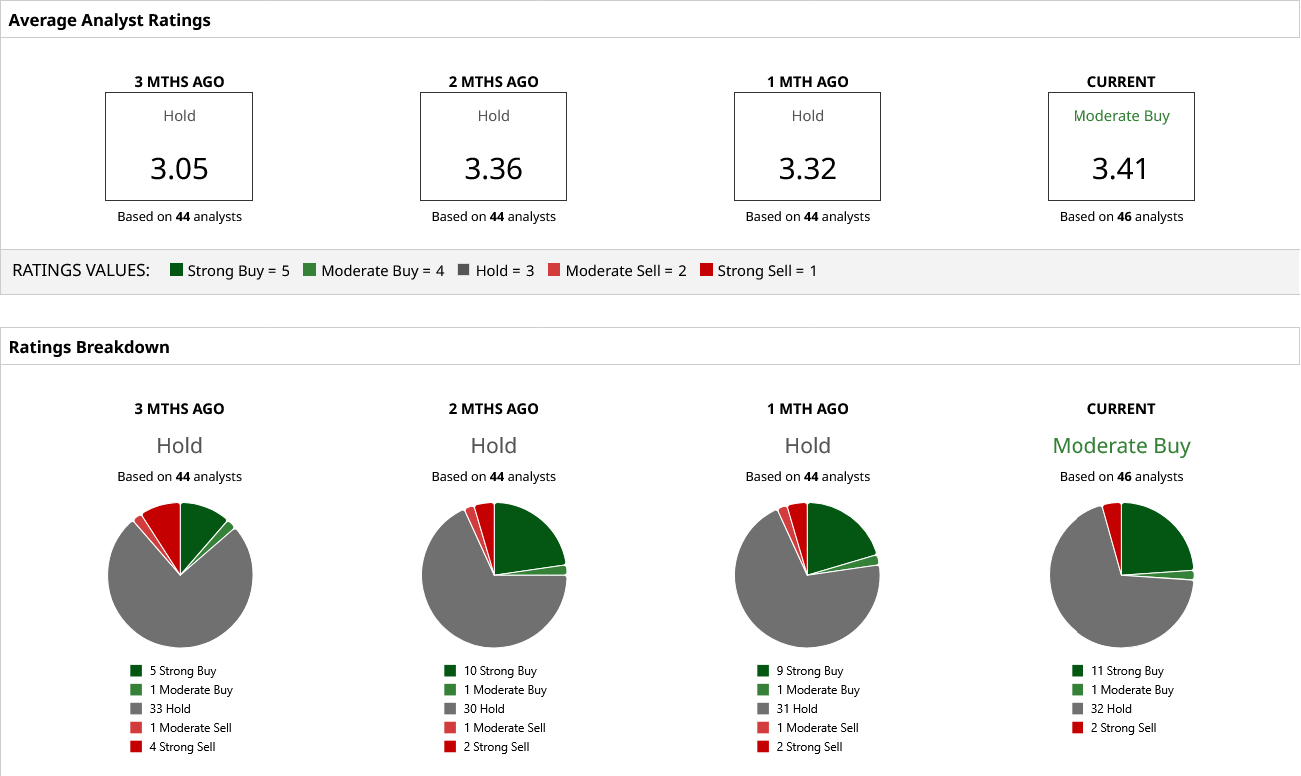

What Do Analysts Expect for INTC Stock?

Analysts assign a “Moderate Buy” rating for INTC, and the stock has a mean price target of $102.87 as compared with HSBC's Street-high target of $200. Considering the current level of shares at around $108, the mean target of $102.87 suggests a potential downside of approximately 5%.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)