With a market cap of $27.6 billion, FirstEnergy Corp. (FE) is a diversified energy company that generates, transmits, and distributes electricity through its subsidiaries across the United States. Operating through its Distribution, Integrated, and Stand-Alone Transmission segments, the company serves customers in six states with a mix of coal, nuclear, hydroelectric, wind, and solar energy sources.

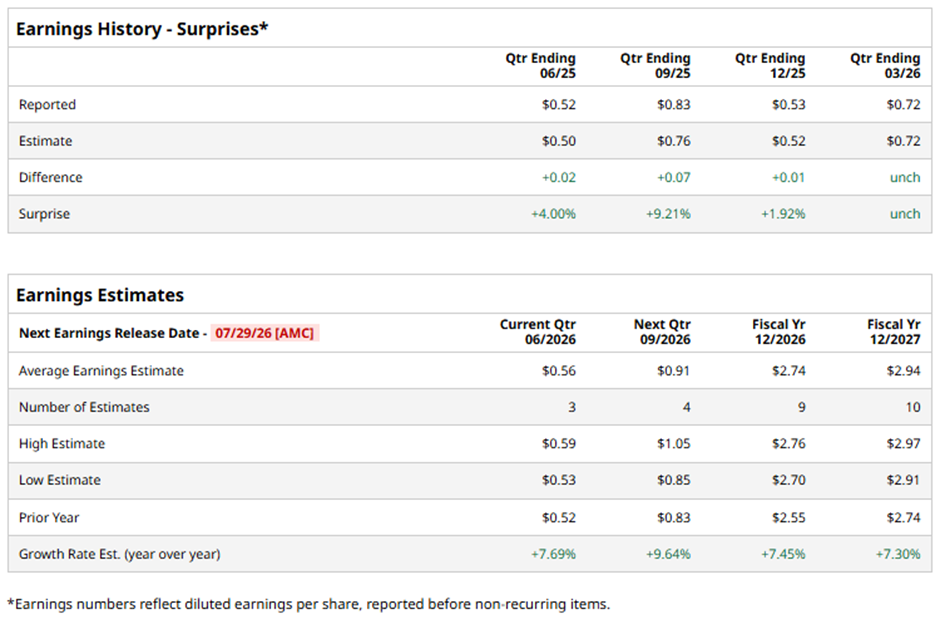

The Akron, Ohio-based company is slated to announce its fiscal Q2 2026 results after the market closes on Wednesday, Jul. 29. Ahead of this event, analysts expect FirstEnergy to report an adjusted Core EPS of $0.56, up 7.7% from $0.52 in the year‑ago quarter. It has exceeded or met Wall Street's earnings expectations in the past four quarters.

For fiscal 2026, analysts expect the utility company to report adjusted Core EPS of $2.74, a rise of 7.5% from $2.55 in fiscal 2025.

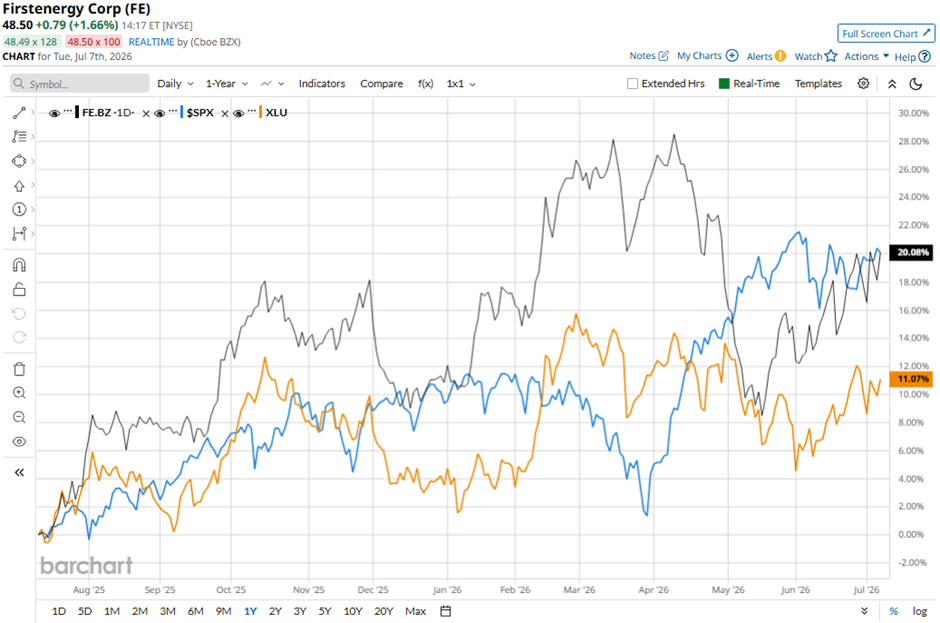

Shares of FirstEnergy have soared 21.4% over the past 52 weeks, outperforming the broader S&P 500 Index's ($SPX) 20.7% return and the State Street Utilities Select Sector SPDR ETF's (XLU) 11.5% gain over the same period.

FirstEnergy reported Q1 2026 results on Apr. 28, with profit of $405 million, or $0.70 per share, up 12.5% from $360 million, or $0.62 per share, a year earlier, driven by higher electricity rates and growing demand from power-intensive data centers. The company also reported revenue of $4.2 billion, up from $3.7 billion a year earlier, and reaffirmed its 2026 core EPS guidance of $2.62 - $2.82, supported by a $6 billion capital investment plan for 2026 focused on grid modernization, distribution upgrades, and transmission reliability.

Additionally, FirstEnergy expanded its 2026 - 2030 capital investment plan to $36 billion, nearly 30% above its previous plan, with the company expecting it to generate about 10% compounded annual rate-base growth. However, the stock fell 1.3% the next day.

Analysts' consensus view on FE stock remains cautiously optimistic, with an overall "Moderate Buy" rating. Out of 17 analysts covering the stock, seven recommend a "Strong Buy," one "Moderate Buy," and nine "Holds." The average analyst price target is $52.64, indicating a potential upside of 8.5% from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)