With a market cap of $16.5 billion, Mid-America Apartment Communities, Inc. (MAA) owns, manages, acquires, develops, and redevelops high-quality apartment communities across the Southeast, Southwest, and Mid-Atlantic regions of the United States. As of March 31, 2026, the company held ownership interests in 104,629 apartment units, including communities under development, spanning 16 states and the District of Columbia.

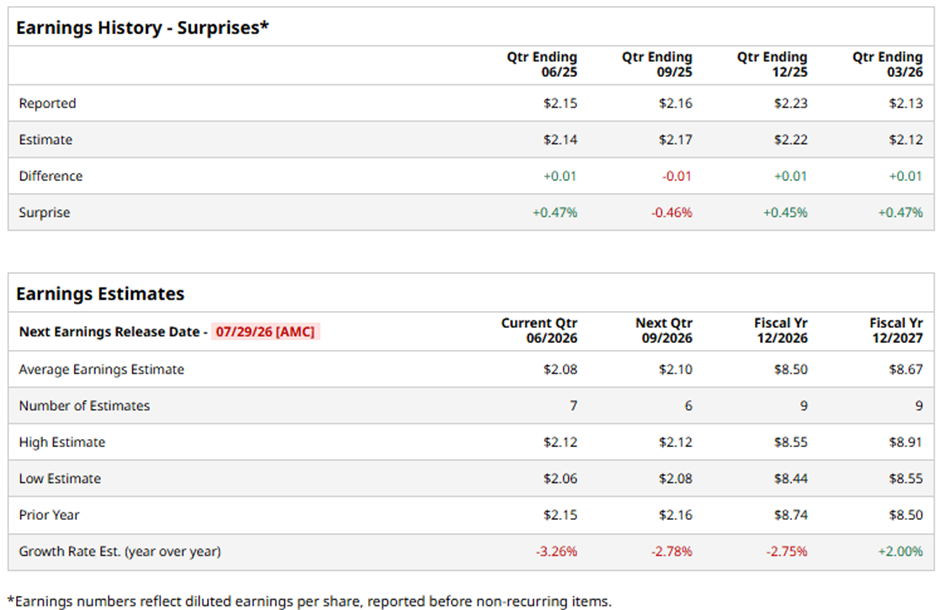

MAA is expected to release its fiscal Q2 2026 results after the market closes on Wednesday, Jul. 29. Ahead of this event, analysts project the REIT to report a core FFO of $2.08 per share, a 3.3% decrease from $2.15 per share in the year-ago quarter. It has exceeded Wall Street’s core FFO expectations in three of the past four quarters while missing on another occasion.

For fiscal 2026, analysts forecast the Germantown, United States-based company to post a core FFO of $8.50 per share, a 2.8% decline from $8.74 per share in fiscal 2025. However, core FFO is anticipated to rise 2% year-over-year to $8.67 per share in fiscal 2026.

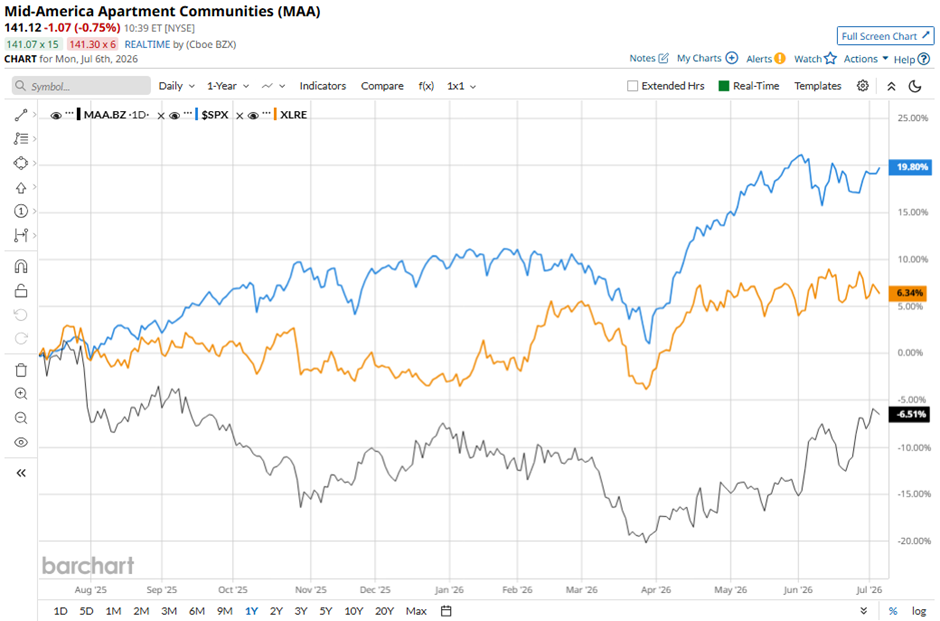

Shares of Mid-America Apartment Communities have dropped 6% over the past 52 weeks, underperforming the broader S&P 500 Index's ($SPX) 19.7% increase and the State Street Real Estate Select Sector SPDR ETF's (XLRE) 6.3% return over the same time frame.

Shares of MAA fell marginally following its Q1 2026 results on Apr. 29 despite reporting core FFO of $2.13 per share, which slightly beat the consensus estimate, as investors focused on weaker operating fundamentals, including rental and other property revenues of $553.7 million, which missed expectations. Sentiment was further pressured by declining same-store performance, with same-store revenues down 0.4%, same-store NOI down 1.3%, average effective rent per unit falling to $1,685, and same-store physical occupancy slipping 10 bps year-over-year to 95.5%, alongside a 13.8% increase in interest expense.

Analysts' consensus view on MAA stock is cautiously optimistic, with an overall "Moderate Buy" rating. Among 26 analysts covering the stock, nine suggest a "Strong Buy," one gives a "Moderate Buy," 13 recommend a "Hold," and three advise "Strong Sell." The average analyst price target of $141.76, indicating a marginal potential upside from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)