/Dell%20Technologies%20by%20Gustianto%20via%20Shutterstock.jpg)

Dell Technologies (DELL) stock still looks undervalued, based on free cash flow analysis and analysts' revenue forecasts. Moreover, shorting 2-week puts at a 6% out-of-the-money (i.e., lower) DELL strike price yields over 3.8%. This article will show how this play works.

DELL closed at $392.32 on Thursday, July 2, off from a June 1 peak of $465.96 (i.e.,-15.8%), after its May 28 Q1 earnings release., But it's well up from May 27, when it closed at just $305.32 (+28.5%).

Higher FCF and FMV Estimates for Dell Stock

I have written two Barchart articles, showing what DELL stock could be worth (i.e., its fair market value or price target), as well as a strategy to play it: i.e., short one-month out-of-the-money puts.

For example, in a June 1 Barchart article, “Dell Stock Could Be Worth 30% More - Based on Strong AI Demand and FCF,” I showed that DELL stock could be worth $544.47 per share. That was based on analysts' 2027 revenue forecasts on a 7.05% FCF margin, to reach a $13.0 billion FCF estimate. Next, after applying a 3.5% FCF yield metric (and discounting the price target by 5% for the time value of money), the fair market value (FMV) was estimated to be $371.4 billion.

(Today, its market cap, according to Yahoo! Finance, is $254.79 billion.)

However, since then, analysts have raised their revenue forecasts to $190.31 billion, so using a 7% FCF margin, 2027 FCF would be:

$190.31b x 0.07 = $13.32 billion '27 FCF

After applying a higher 3.70% FCF yield (i.e., multiplying FCF by 27x) (i.e., a slightly lower metric) and discounting it by 5%, the FMV is $341.7 billion:

$13.32b x 27 = $359.64b x 0.95 = $341.658b FMV

That's almost $87 billion higher than today's market cap of $254.79 billion, or 34% higher. In other words, the price target (PT) is 34% higher than last week's close:

$392.32 price x 1.34 = $525.71 price target (PT)

Analysts Agree DELL is Undervalued

Analysts have raised their PTs in the last 2 weeks. For example, in my June 16 Barchart article, “Dell Stock Looks Cheap Here With Higher Analyst Forecasts - Short Put Plays Are Attractive,” Yahoo! Finance reported that the average of 27 analysts was $483.83. Now, that average is up to $485.09.

That PT is 23.6% over last week's closing price. Similarly, Barchart's mean analyst survey PT has risen from $485.95 to $486.86, which represents a 24% upside for DELL stock.

The bottom line is that, either based on its future FCF estimates or analysts' price targets, DELL still looks very cheap.

However, as I pointed out in my last Barchart article, there is no guarantee that DELL stock will rise right away to that PT. So, one way to set a lower buy-in is to sell short out-of-the-money (OTM) puts in nearby expiry periods.

Shorting OTM DELL Puts for High Yield and Lower Buy-In

For example, in my June 16 Barchart article, I suggested shorting the $370 put option strike price contract that expires on July 17. At the time, that was about 9.5% below Dell's price, and it sold at a $18.20 premium. That gave short-put investors a one-month yield of 4.92% (i.e., $18.20 / $370.00).

Today, that premium has fallen to $14.18 at the midpoint. So, for the next two weeks, an investor can still make a 3.83% yield (i.e., $14.18/$370.00). This can be seen in Barchart's July 17 option chain table below:

This strike price is just over 6% below the closing trading price (i.e., out-of-the-money), so, there is no danger just yet that the investor's collateral would be assigned to buy 100 shares at $370.00. However, the delta ratio is fairly high at -0.3151, implying over a 31% chance that DELL could drop to $370 in the next two weeks.

Nevertheless, even if the account is assigned at $370, the net breakeven point is much lower:

$370 - $14.18 income already received = $355.82 breakeven buy-in point

That is 9.76% below last week's closing price, so it provides a good entry point for value investors.

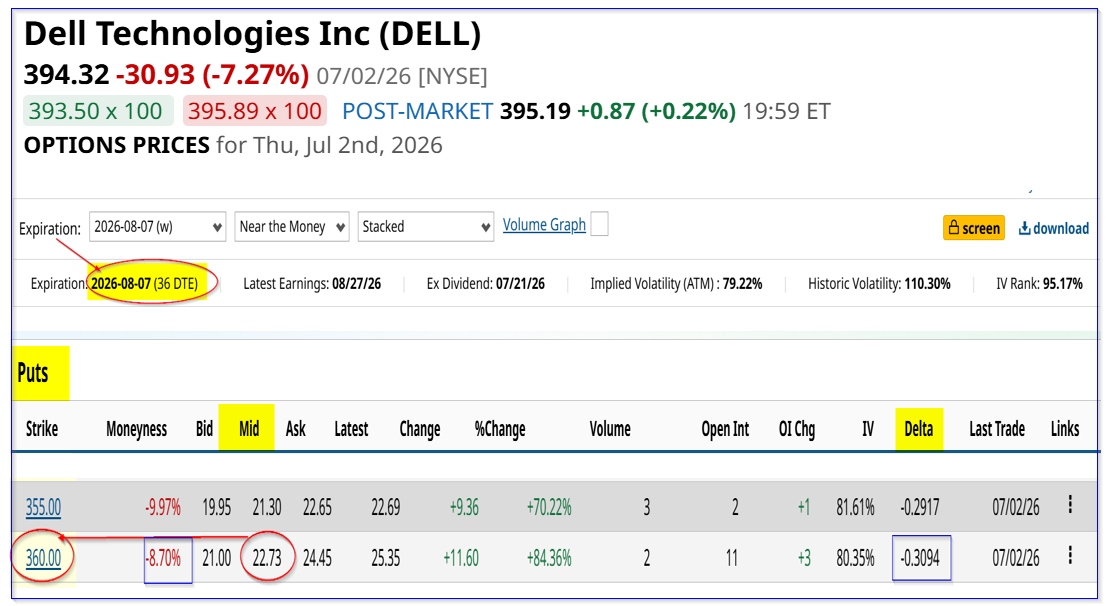

However, it might make more sense for new investors to short a one-month out DELL put at a lower strike price. Look at the table below.

It shows that for the Aug. 7 expiry period, a lower $360 strike price put option, with a similar delta ratio (i.e., risk of assignment), has a higher premium of $22.73.

That gives the investor a higher short-put yield for the same risk:

$22.73 / $360.00 = 6.3139% one-month yield. Granted, that is lower than repeating the 3.83% 2-week short-put play above (i.e., 3.83% x 2 = 7.66%). But, the strike price is lower, i.e., 8.70% below today's price, and the net breakeven point is much lower:

$360.00 - $22.73 = $337.27 breakeven, i.e., -14.5% below today's price

As a result, either of these two short-put plays is very attractive to value investors.

For example, if an investor can repeat this one-month 6.3% short-put yield for the next 6 months, the expected return (ER) is 37.8%. That is higher than my 34% higher-price-target expected return over the next year. (Note that there is no guarantee an investor can repeat this one-month short-put yield each month for the next six months.)

The bottom line here is that DELL stock looks deeply undervalued. Since its two-week and one-month put option premiums are very high, it makes sense to short them to make high yields.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)