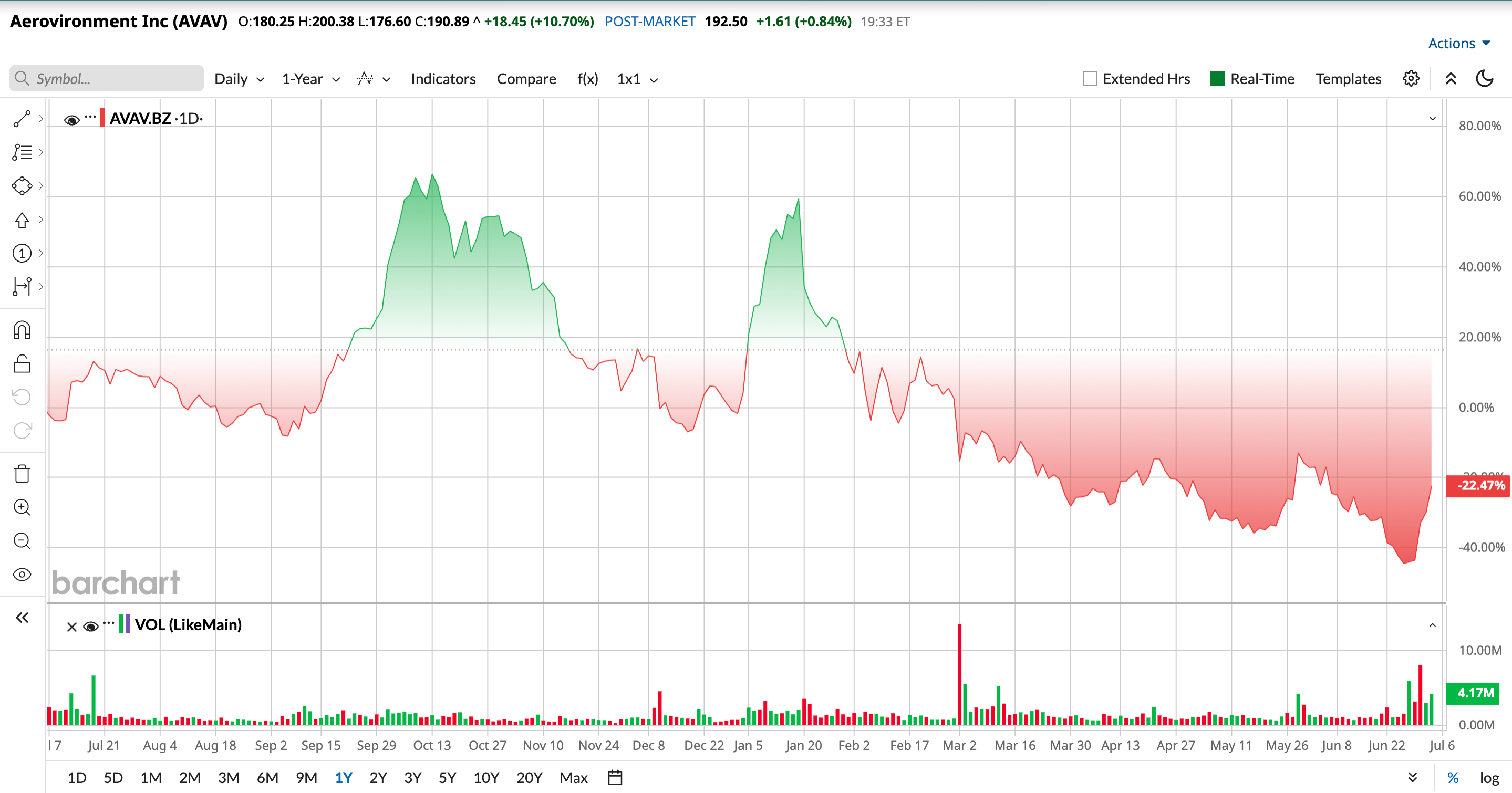

AeroVironment’s (AVAV) stock jumped 18.76% on June 30 after an earnings update gave investors something solid to react to. The fiscal fourth‑quarter report showed roughly $642 million in revenue, a record that beat prior results and analyst expectations.

The backdrop is messy. Earlier this year, AVAV sank after management disclosed an $89 million goodwill calculation error in its space unit, forcing a restatement and raising doubts about its numbers. And this week, it faces a securities‑fraud class action over alleged misstatements tied to the cancellation of its SCAR contract, adding legal risk to the mix.

So the stock is now moving higher on strong earnings while still carrying accounting and legal baggage. However, is AeroVironment’s latest pop a chance to buy into a mispriced defense growth story or just another headline‑driven spike best watched from the sidelines?

AeroVironment’s Latest Earnings Numbers

Arlington, Virginia-based AeroVironment develops unmanned aircraft systems, missile systems, and related technologies for defense and intelligence customers.

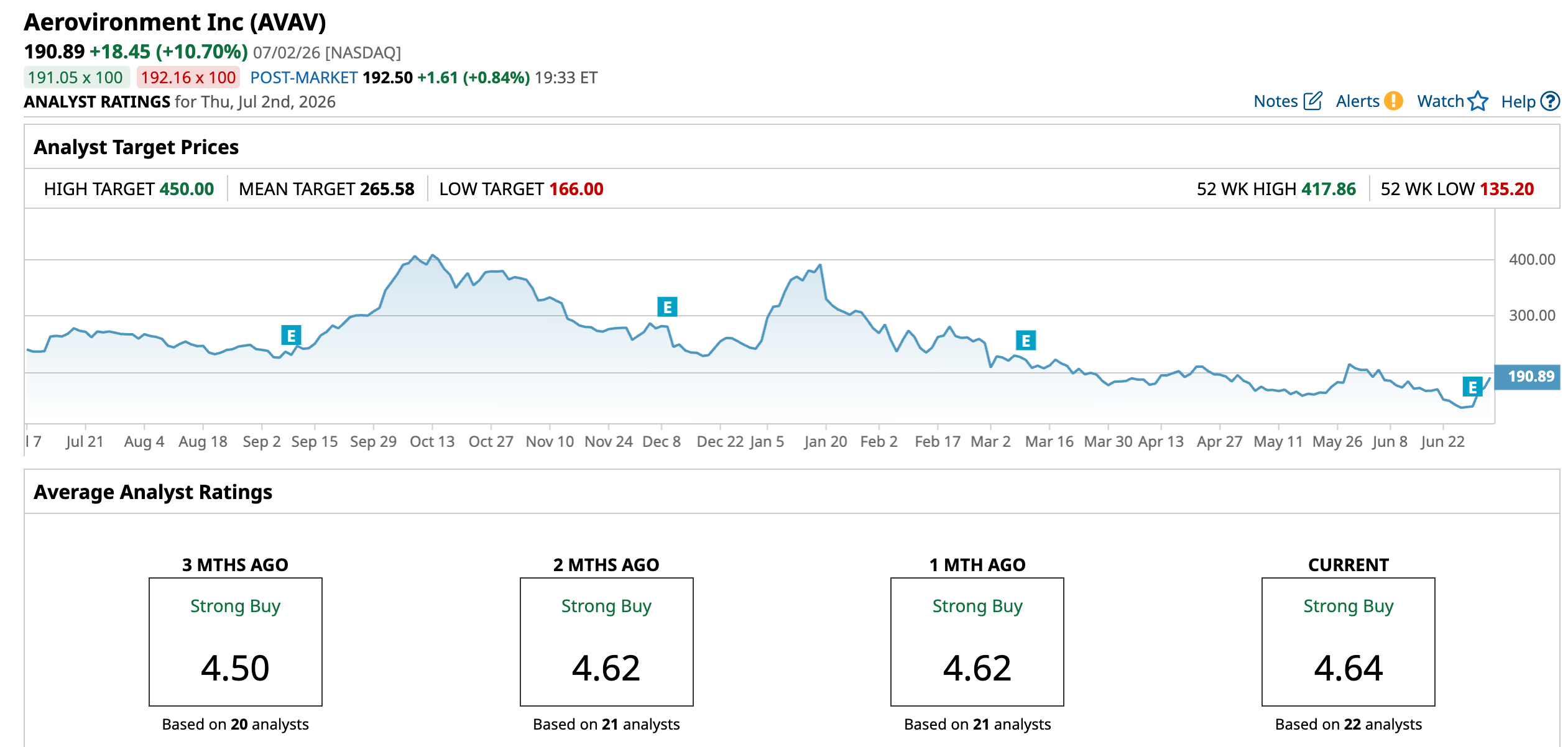

It has a market value of $9.66 billion, and the stock is down 21.1% year‑to‑date (YTD) and 22.5% over the past 52 weeks.

The company is valued at 58.92 times trailing price-to-earnings and 57.47 times forward price-to-earnings, compared with sector medians of 22.85 times and 20.99 times, so investors are clearly paying up for this name.

AeroVironment’s latest earnings numbers help explain why the stock reacted sharply higher. Their Q1 calendar 2026 results, released on June 29, showed revenue of $641.6 million against analyst estimates of $559.4 million, roughly 133% growth year-over-year (YOY) and a 14.7% beat.

This strength was not just about sales. AVAV reported adjusted EPS of $1.84 versus $1.47 expected, a 25% upside surprise that points to good operating leverage as more contracts flow through.

Their profitability looks solid as well, as adjusted EBITDA came in at $140.1 million versus estimates of $125.7 million, a 21.8% margin and an 11.4% beat. Also, its operating margin improved to 8.9% from 5% a year earlier, showing that costs and mix are moving the right way as larger programs ramp.

AVAV's free cash flow also flipped from ‑$8.79 million a year ago to $55.43 million, a shift that makes the earnings story feel more durable.

AeroVironment’s Defense Pipeline

AeroVironment’s growth pipeline is quietly building a case. The company has a memorandum of understanding with Taiwan’s Ubiqconn Technology to develop a common controller ecosystem for Taiwan’s indigenous unmanned aircraft systems program. This framework is meant to standardize ways in which different drones are operated and integrated into the country’s defense network.

On top of that, management is pushing beyond the air into ground robotics. The TOM‑50 RE is a backpackable unmanned ground vehicle aimed at rapid reconnaissance and explosive ordnance disposal. They are built for small units that need to deploy quickly and operate from a safer distance in high‑risk areas.

The company is also making sure it can physically deliver on bigger orders. Capacity is being scaled through expansions in the Dayton area and Huntsville, lifting advanced production for next‑generation systems like the Freedom Eagle‑1 interceptor and other high‑speed intercept technologies.

Longer‑dated projects round out the picture. AeroVironment has a $20 million contract to advance ceramic materials research for the U.S. Air and Space Forces. This contract will be focused on high‑performance ceramics that can withstand extreme heat and stress in advanced aerospace applications.

Taken together, these give AeroVironment a more visible growth runway.

What are the Analysts Saying

Analysts are not just reacting to the last quarter. They’re already leaning into what comes next for AeroVironment. For the current quarter ending July 2026, the average earnings estimate sits at $0.53 per share, as opposed to the $0.32 recorded in the same period last year. That gap translates to an expected YOY growth rate of 65.63%.

Guidance from the company tells a slightly different story. AVAV is calling for EBITDA of $315 million at the midpoint for financial year 2027, a number that trails external estimates of $357.7 million. This mismatch suggests management is a bit more cautious than the Street.

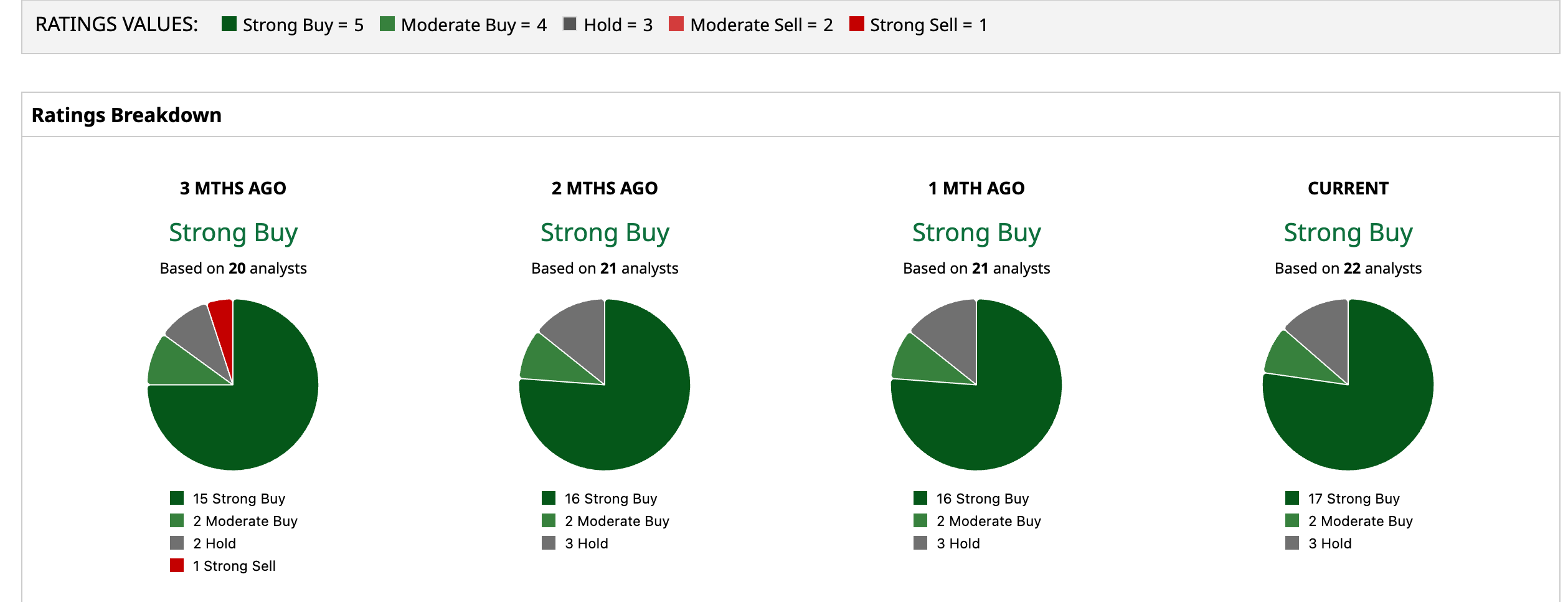

Even with that softer guide, the broader view on the stock is still strong. Analysts following AVAV have collectively reached a “Strong Buy” consensus rating. The average price target of $265.58 implies a substantial 39.1% upside from here.

Conclusion

AeroVironment has earned its post-earnings pop with real growth, stronger margins and a deep pipeline, but the stock is not a slam dunk buy at any price. At today’s levels it looks more like a high quality name for investors who can tolerate defense headline risk and a premium valuation than a classic bargain. Its shares seem more likely to drift higher over time than fall apart, as long as contracts and execution hold up, though the path will probably be bumpy rather than smooth.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)