/A%20concept%20image%20of%20space_%20Image%20by%20Canities%20via%20Shutterstock_.jpg)

AI infrastructure construction fever is turning semiconductor equipment companies into the market's most successful players, and few have benefited from that trend as much as Applied Materials (AMAT). AMAT stock hit new highs after the investment bank KeyBanc Capital Markets hiked its price target to $750, and then Sesquania followed up with a $900 price target—the highest among all Wall Street analysts. These price hikes are based on AMAT's strong potential for long-term earnings and undervaluation compared to rivals.

But just a few weeks ago, Applied Materials reported another record earnings period while raising its forecast for the semiconductor equipment market as hyperscalers, memory manufacturers, and foundries increase their spending on AI infrastructure construction. This has made many wonder whether the stock run has already peaked or if there is room left for further growth.

Applied Materials Stock Overview

Applied Materials is the world's largest manufacturer of semiconductor processing equipment, offering deposition, etch, inspection, metrology, and packaging technologies for the fabrication of advanced logic, DRAM, and NAND chips. The company is headquartered in Santa Clara, California, and has a market capitalization of about $551.5 billion, which makes it one of the leaders in the industry's capital equipment segment.

Despite some volatility as of this writing, AMAT stock is one of the market's strongest performing stocks. On Tuesday, its shares reached a new 52-week high of $739.67, gaining over 370% from last year's low point and nearly 15% over the past five trading sessions. That outperformance of the semiconductor market and S&P 500 Index ($SPX) was caused by investors' realization of the stock being one of the biggest beneficiaries of the spending on AI infrastructure construction.

The spectacular surge notwithstanding, AMAT stock's valuations may be less excessive than they might appear based on its multiples. Applied Materials is valued at about 51.8x forward P/E and 17.5x sales, which might look high compared to average historical multiples. But analysts began valuing semiconductor equipment companies based on normalized earnings several years ahead instead of near-term results. New KeyBanc target price of $750 is based on the estimate of fiscal 2028 EPS of $24.17, implying that analysts believe the company's future growth will catch up with current valuation due to its investments into AI infrastructure.

Besides growing earnings, the company also distributes dividends and performs share repurchases. Last quarter, Applied Materials paid out $765 million, including $400 million in shares and $365 million in dividends.

Applied Materials Beats on Earnings

Applied Materials announced another great quarter when it reported fiscal second-quarter 2026 results on May 14. Its revenues rose 11% year-over-year (YoY) to a record $7.91 billion, while GAAP EPS and non-GAAP EPS were $3.51 and $2.86, respectively, increasing 20% YoY. Moreover, gross margin reached an impressive 50%, which demonstrates the strong pricing power of the company even despite its continuous industry growth.

But perhaps even more important than good financial results were comments from management. CEO Gary Dickerson noted that the company now expects its semiconductor equipment business to increase more than 30% in calendar 2026 due to fast-growing demand from AI infrastructure investments. Moreover, the company highlighted that leadership in leading-edge logic, DRAM, and advanced packaging would support long-term revenue and earnings growth.

Applied Materials has also announced new partner engagements at its EPIC Center, which aims to speed up the commercialization of future semiconductor manufacturing technologies. Additionally, the company's management increased production plans and inventory levels and improved logistics capabilities to support increasing demand from its customers due to growing spending on AI infrastructure.

All those comments confirm a trend that was discussed throughout the industry in the past few years. While previously focused mostly on GPUs, spending on AI infrastructure is spreading through the whole semiconductor manufacturing market, positively affecting companies that provide equipment for the production of advanced chips. Applied Materials seems to be the key player in that trend.

Analysts' Outlook for AMAT Stock

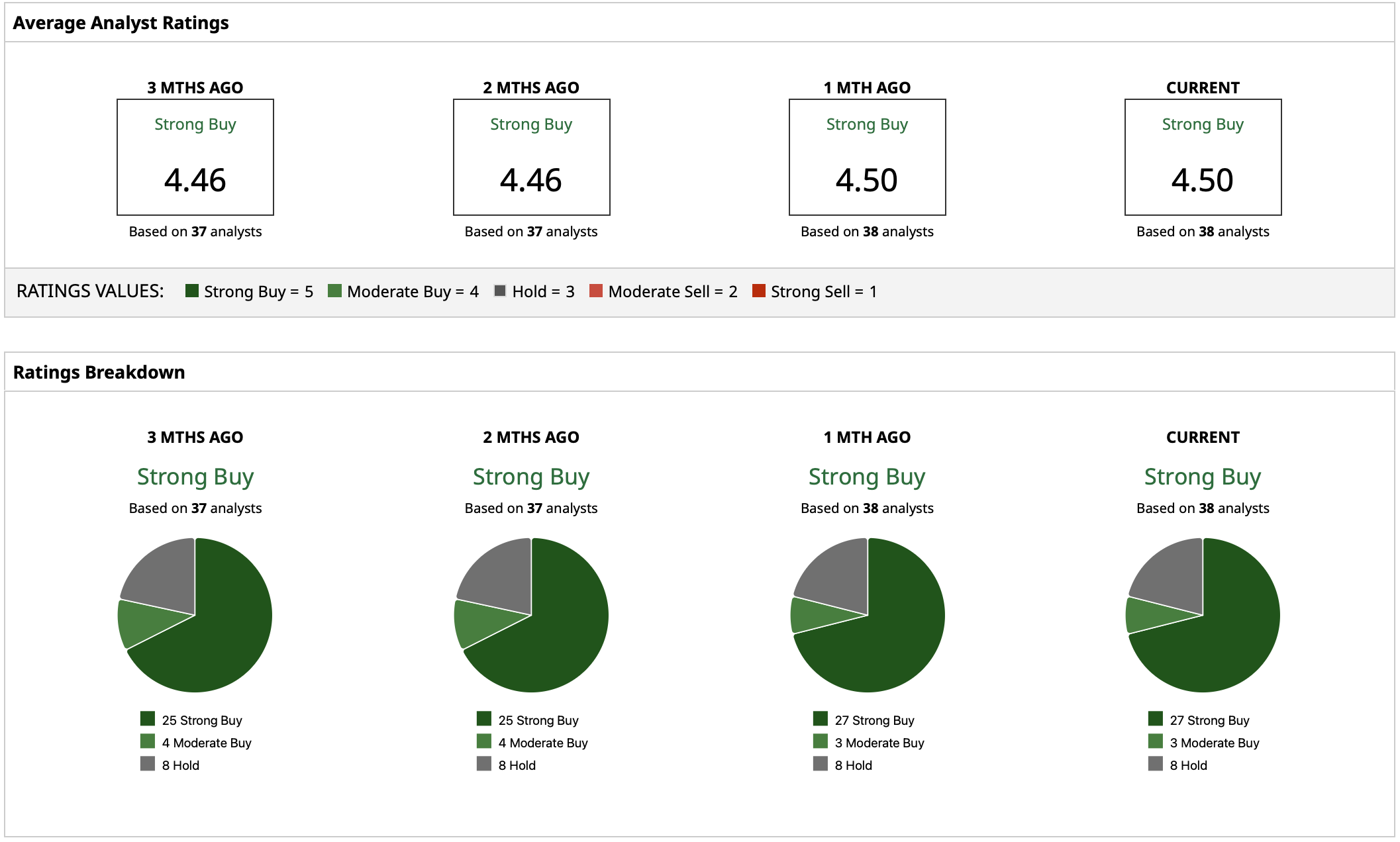

Wall Street is still very positive on AMAT stock with a "Strong Buy" rating consensus, with analysts continually increasing both earnings estimates and price targets due to its strong results. Currently, the consensus mean price target stands at $594.21, which is below the current price after the recent surge. But usually consensus estimates lag major price movements. KeyBanc set a new price target of $750, but Sesquania went one step further and set a new price target of $900, which is now the highest price target among Wall Street analysts. KeyBanc reiterated its “Overweight” recommendation, stating that Applied Materials is significantly undervalued compared to other semiconductor equipment stocks while still retaining leadership in various growth segments. And Sesquania kept its “Positive” rating.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)