With a market cap of $52.4 billion, Baker Hughes Company (BKR) is a global energy technology firm that provides a broad portfolio of products and services across the oil, gas, and industrial value chains. Operating through its Oilfield Services & Equipment and Industrial & Energy Technology segments, the company supports customers from upstream to downstream with advanced equipment, digital solutions, and lifecycle services.

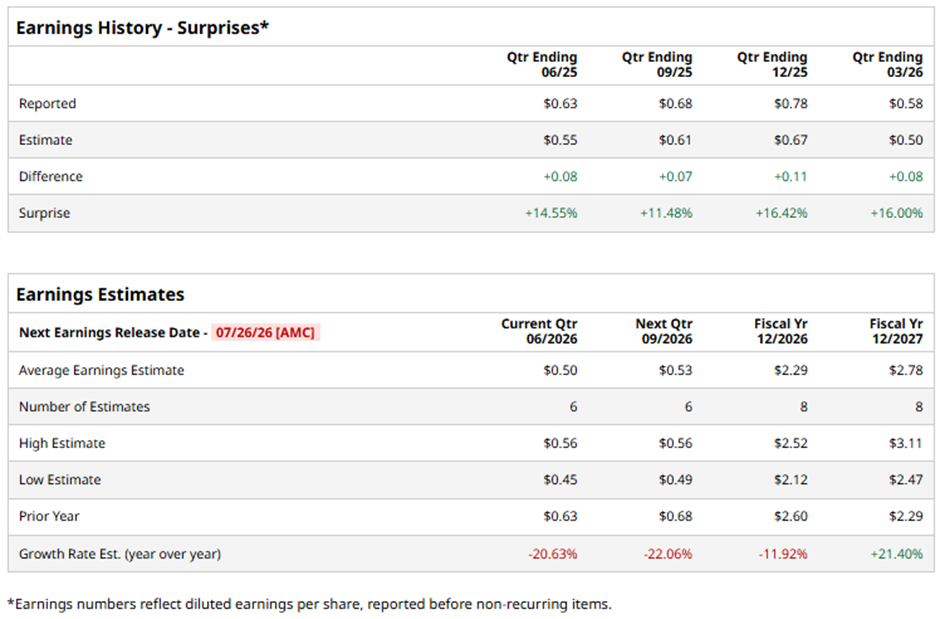

The Houston, Texas-based company is set to announce its fiscal Q2 2026 results after the market closes on Sunday, Jul. 26. Ahead of the event, analysts expect BKR to report an adjusted EPS of $0.50, a decrease of 20.6% from $0.63 in the year-ago quarter. However, the company has surpassed Wall Street's bottom-line estimates in each of the past four quarters.

For fiscal 2026, analysts forecast the oilfield services provider to post adjusted EPS of $2.29, down 11.9% from $2.60 in fiscal 2025. Nevertheless, adjusted EPS is anticipated to grow 21.4% year-over-year to $2.78 in fiscal 2027.

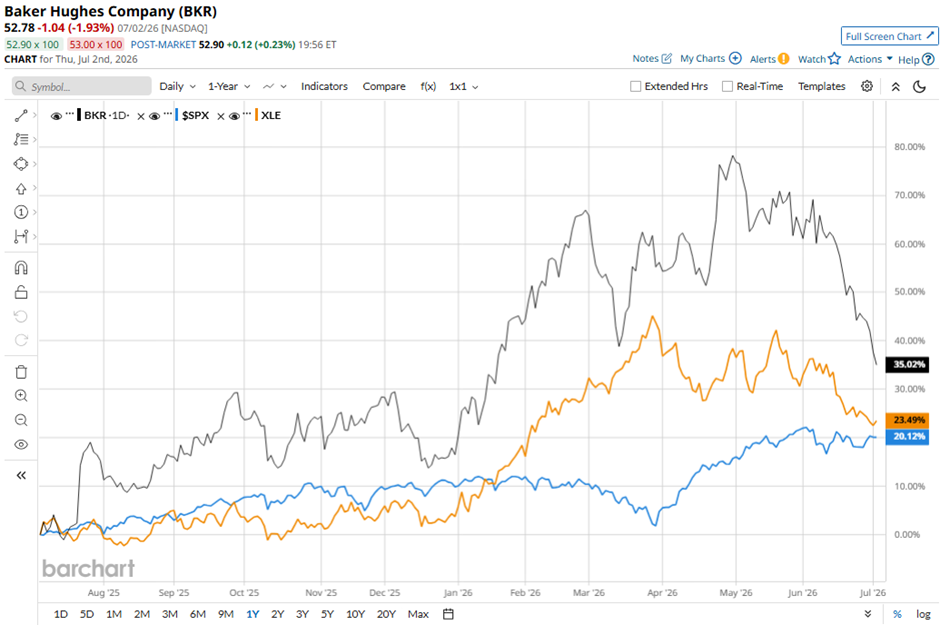

Shares of Baker Hughes have increased 32.5% over the past 52 weeks, surpassing the S&P 500 Index's ($SPX) 20.2% gain and the State Street Energy Select Sector SPDR ETF's (XLE) 22.4% return over the same time frame.

Baker Hughes' shares soared 6.9% following its Q1 2026 results on Apr. 23 after the company reported stronger-than-expected adjusted EPS of $0.58 and revenue of $6.59 billion. Investor confidence was further supported by the strong performance of its Industrial & Energy Technology (IET) segment, where orders increased 54% year-over-year to $4.89 billion from $3.18 billion, driven by robust demand from data centers, LNG projects, gas infrastructure, and grid equipment.

Although Oilfield Services & Equipment (OFSE) revenue declined 7% year-over-year to $3.24 billion and Middle East/Asia revenue fell 19% to $1.15 billion due to regional disruptions, the better-than-expected earnings and strong IET order growth outweighed concerns over weakness in oilfield activity.

Analysts' consensus rating on BKR stock is cautiously optimistic overall, with an overall "Moderate Buy" rating. Out of 20 analysts covering the stock, 14 recommend a "Strong Buy," one has a "Moderate Buy" rating, four give a "Hold" rating, and one advises a "Strong Sell." The average analyst price target is $72.48, suggesting a potential upside of 37.3% from the current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)