EQT Corporation (EQT), headquartered in Pittsburgh, Pennsylvania, operates as a natural gas production company. With a market cap of $32.8 billion, EQT is an integrated energy company with emphasis on Appalachian area natural-gas supply, transmission, and distribution, offering its products to wholesale and retail customers. The leading independent natural gas producer is expected to announce its fiscal second-quarter earnings for 2026 in the near term.

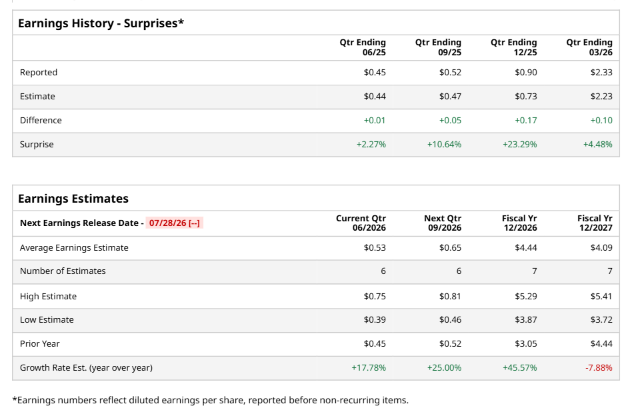

Ahead of the event, analysts expect EQT to report a profit of $0.53 per share on a diluted basis, up 17.8% from $0.45 per share in the year-ago quarter. The company beat the consensus estimates in each of the last four quarters.

For the full year, analysts expect EQT to report EPS of $4.44, up 45.6% from $3.05 in fiscal 2025. However, its EPS is expected to fall 7.9% year over year to $4.09 in fiscal 2027.

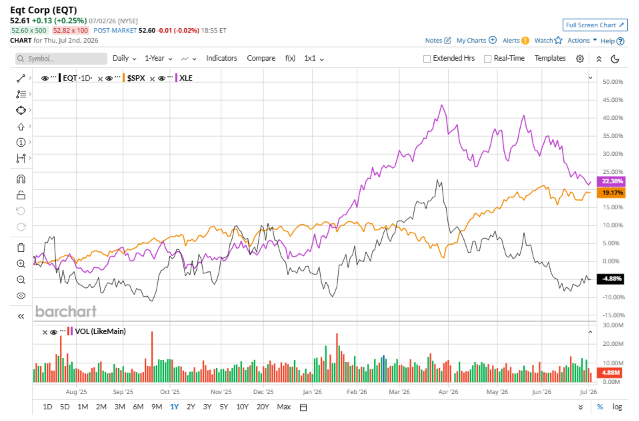

EQT stock has underperformed the S&P 500 Index’s ($SPX) 20.2% gains over the past 52 weeks, with shares down 6.3% during this period. Similarly, it underperformed the State Street Energy Select Sector SPDR ETF’s (XLE) 22.4% returns over the same time frame.

On Apr. 21, EQT reported its Q1 results, and its shares closed up more than 3% in the following trading session. Its revenue stood at $3.4 billion, up 94.2% year over year. The company’s adjusted EPS increased 97.5% from the year-ago quarter to $2.33.

Analysts’ consensus opinion on EQT stock is bullish, with a “Strong Buy” rating overall. Out of 25 analysts covering the stock, 20 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and four give a “Hold.” EQT’s average analyst price target is $68.92, indicating a notable potential upside of 31% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)