/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)

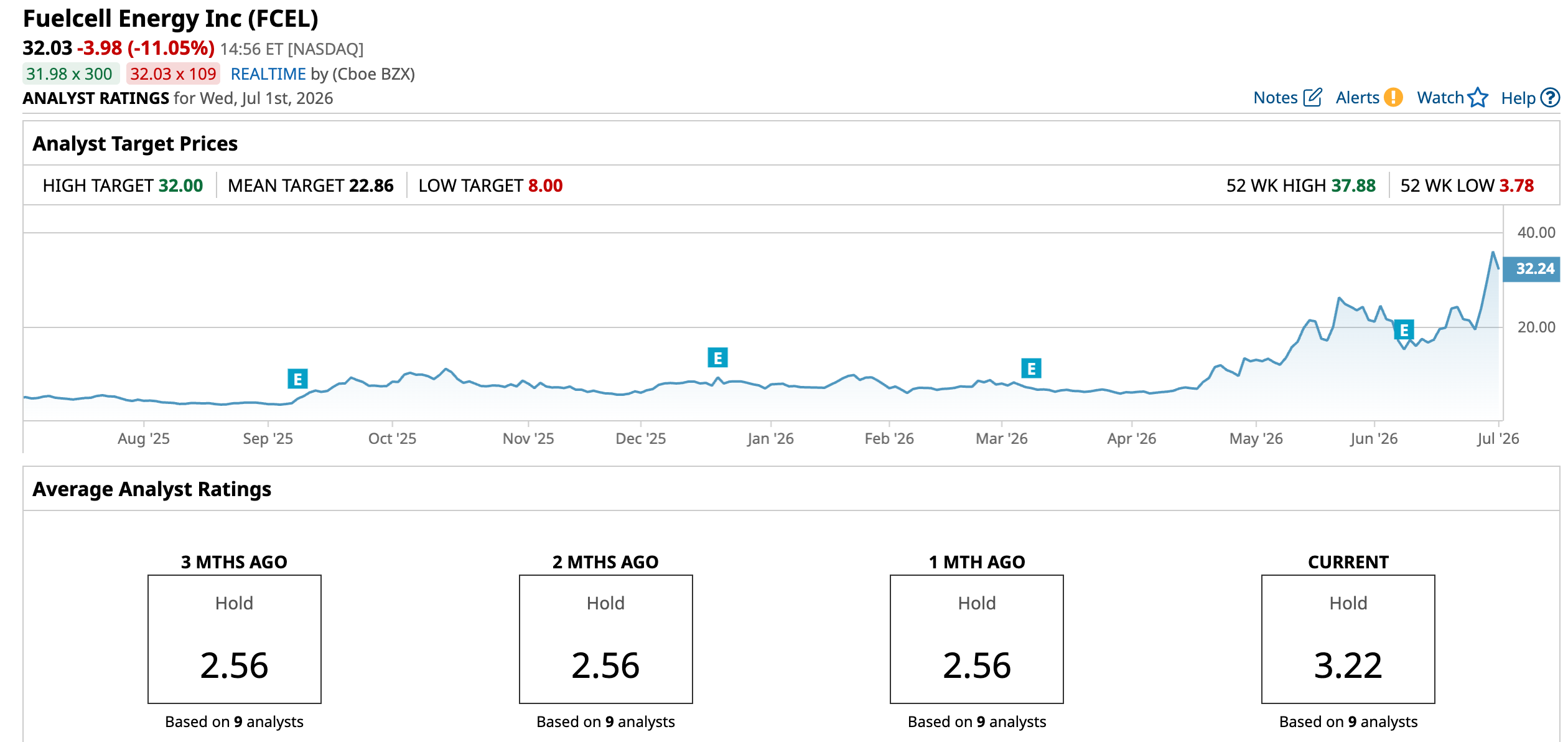

B. Riley analyst Ryan Pfingst recently upgraded his FuelCell Energy (FCEL) rating from “Neutral” to “Buy,” while significantly raising the firm’s price target from $13 to $32. The upgrade follows a new agreement with Fit Energy USA to deploy up to 380 megawatts of power for AI data centers. Fit Energy USA is backed by the investment firm Fit Ventures. The company focuses on delivering power to data centers through fuel cell technology and natural gas turbines. The deal has made Pfingst confident that FuelCell can convert major data center operators as its customers.

The agreement covers multiple power delivery structures, including behind-the-meter solutions, grid-connected models, and microgrids. Unlike FuelCell’s competitors, offering single delivery model, the company’s ability to serve different configurations makes it more versatile. Given the significant variance in size and setup of data centers, this flexibility offers FuelCell a genuine competitive advantage over its peers. The analyst also predicted a positive EBITDA beginning in the second half of 2027. If this comes true, FuelCell’s financial trajectory will shift considerably. On the same day, the Export-Import Bank of the United States approved a $49 million financing package for the company.

About FuelCell Energy Stock

FuelCell Energy is a clean energy company that designs, manufactures, and operates fuel cell platforms for low-emission power generation. Its product portfolio includes fuel cell power systems, carbon capture technology, combined heat and power solutions, and hydrogen production systems. Founded in 1969 and led by CEO Jason Few, the company is headquartered in Danbury, Connecticut.

Over the last 12 months, FuelCell Energy stock has skyrocketed 514.3%, significantly outperforming the S&P 500 Index’s 21% gain during the same period. The rise is primarily driven by FuelCell’s strategic pivot towards powering AI data centers. Most recently, the growth has accelerated further due to multiple analyst upgrades, the Fit Energy deal, and the Export-Import Bank financing. The stock, sitting at its 52-week high, has lately increased 48.7% in the last five trading sessions.

FuelCell Energy’s valuation is difficult to assess by traditional measures. The forward GAAP price-to-earnings ratio is not meaningful since the company is not yet profitable. The forward price-to-sales ratio of 15.70 times sits nearly double the company’s own 5-year average of 8.28 times. The significant premium to its historical norm reflects how dramatically the stock has recently surged. The EPS trajectory looks promising for a company that is currently loss-making. The losses are expected to shrink 62% in 2026, with healthy improvements expected in the next couple of years. A further EPS growth of 93% in 2029 means the company could potentially be turning profitable by then.

The capital structure also remains strong, with FuelCell being net cash positive by over $214 million. For a company with significant expansion plans, the balance sheet looks reassuring. However, the current valuation appears to be a best-case scenario, which is consistent with B. Riley’s bullish price target still sitting below the company’s current stock price.

FuelCell Energy’s Pipeline Surge Overshadows Weak Quarter

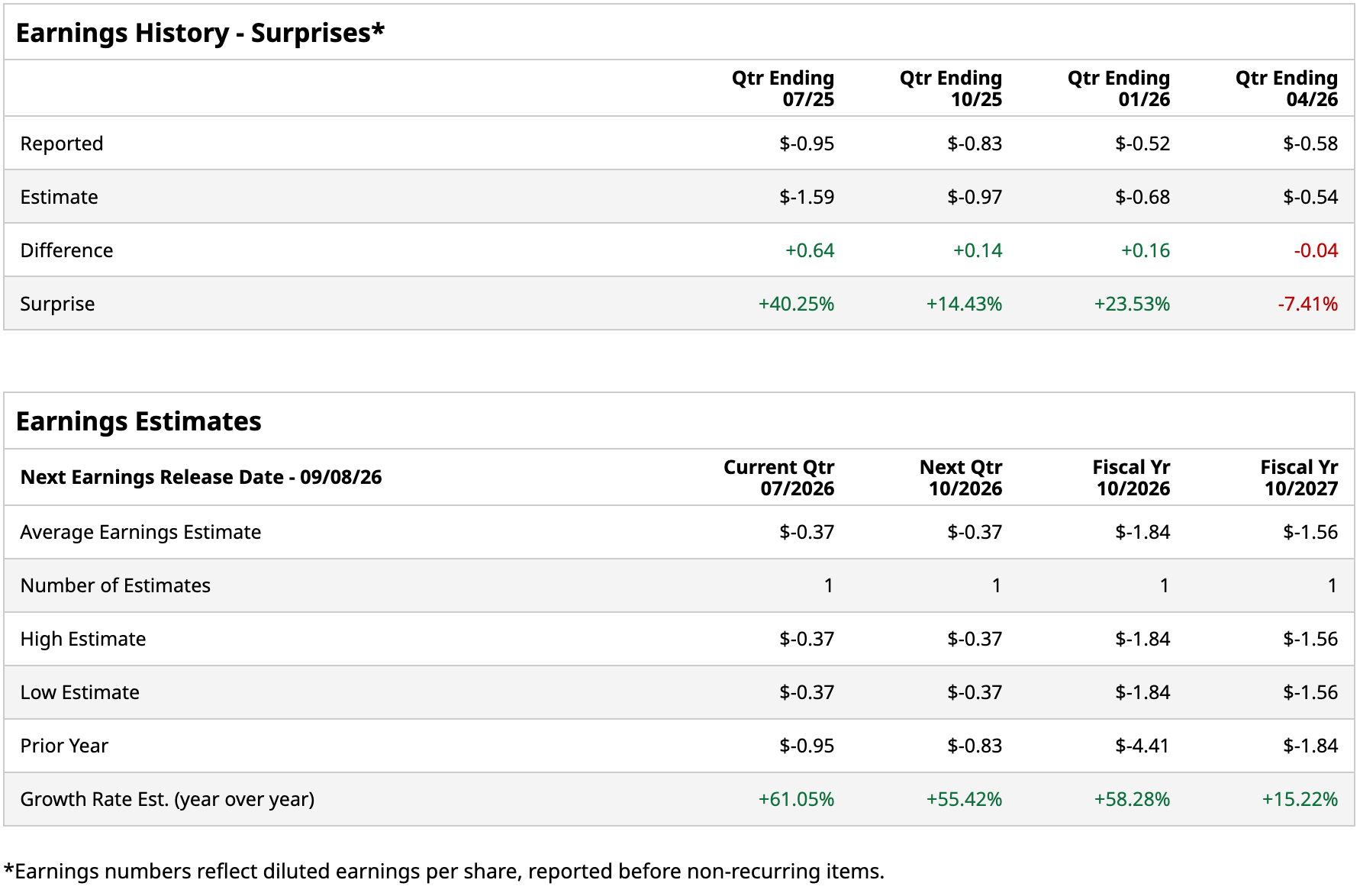

FuelCell Energy reported its second-quarter fiscal 2026 earnings on June 8. Based on this quarter alone, the firm had a rather below-par performance. Revenue of $35.6 million, missed the analyst consensus of $40.51 million and declined 5% year-over-year (YOY). The net loss increased drastically from $38.8 million to $78.7 million. The net loss per share was reported at $1.45, vastly underperforming the $0.43 consensus. Despite the results missing most estimates, CEO Jason Few described the quarter as reflecting strong commercial momentum and disciplined operating execution. The CEO also stated that the firm has had continued progress in its data center strategy.

The outlook explains why the stock price has risen sharply despite weak numbers. FuelCell’s sales pipeline surged 267% quarter-over-quarter to 4 gigawatts, with approximately 89% of submitted proposals tied to AI data centers. The company ended the quarter with nearly $441 million in cash. The CEO believes that this positions FuelCell to successfully fulfill the pipeline opportunities and create long-term value for shareholders. The Torrington facility in Connecticut is being expanded to support up to 500 MW of annualized production capacity. FCEL management believes that the negative $17.1 million EBITDA reported last quarter will turn positive once the annualized production volumes reach or exceed 100 MW.

What Are Analysts Saying About FuelCell Energy Stock?

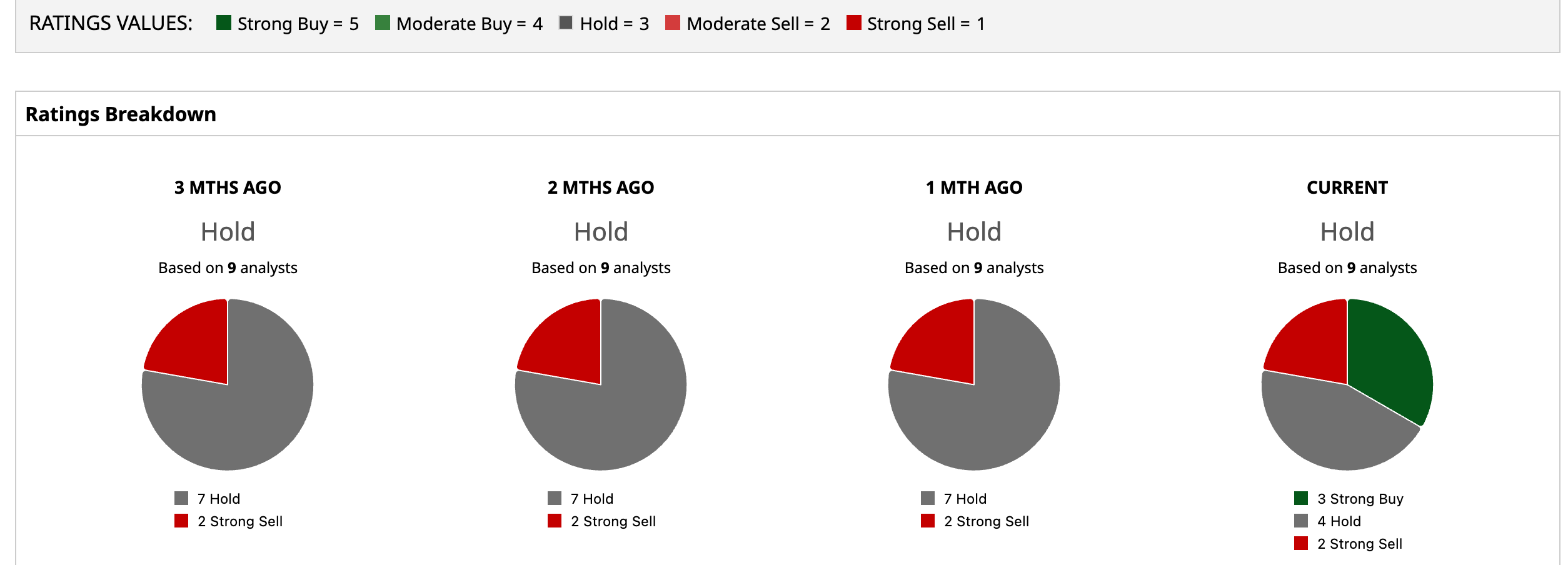

Before B. Riley’s upgrade from “Neutral” to “Buy” with the price target raised to $32, other analysts have recently increased the firm’s price targets as well. Jefferies analyst Julien Dumoulin Smith also upgraded FuelCell’s rating from “Hold” to “Buy,” increasing the price target from $16 to $24. On the same day as the Jefferies upgrade, UBS analyst Manav Gupta nearly tripled his price target from $7.5 to $22, reflecting growing confidence in the company’s data center power strategy.

Based on the nine Wall Street analysts' estimates, the company has a consensus “Hold” rating with a mean price target of $22.86, indicating a 28.6% downside. The lowest price target is just $8.00, while even the highest price target of $32.00 sits below the current stock price. This suggests that the stock’s extraordinary recent surge has moved significantly ahead of where the Wall Street analysts believe it should be valued.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)