The Hartford Insurance Group, Inc. (HIG), based in Connecticut, is a two-century-old insurance company with a market capitalization of $36.7 billion. Serving individuals, businesses, and institutions across the U.S., the U.K., and select international markets, the company offers a broad mix of coverage through its Business Insurance, Personal Insurance, Employee Benefits, and Property & Casualty operations.

Built on a legacy of financial strength and disciplined underwriting, The Hartford has earned a reputation for dependable service, customer trust, and ethical business practices. Today, it continues to blend its long-standing expertise with a focus on innovation, sustainability, and long-term value creation.

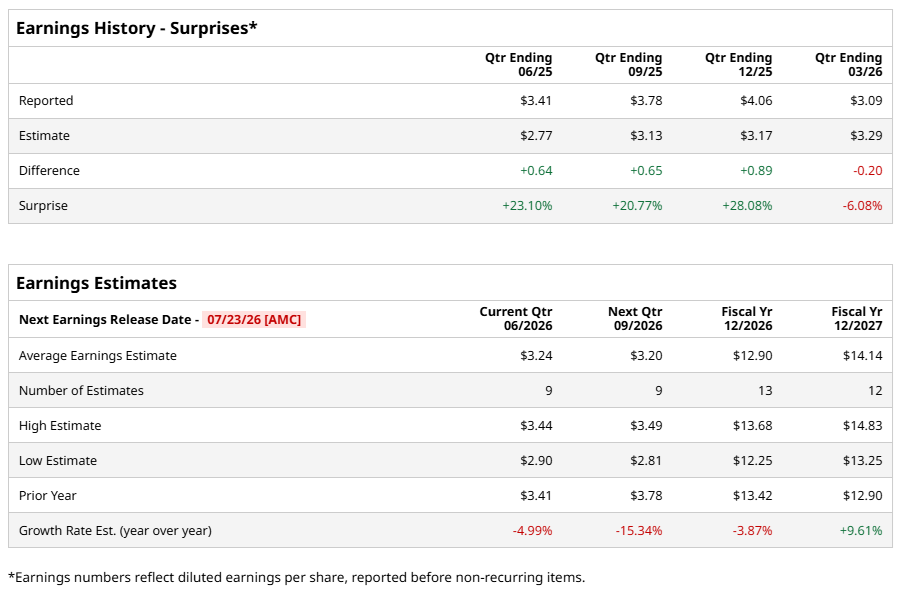

The insurance and financial services company is expected to announce its fiscal second-quarter earnings for 2026 on Thursday, July 23, after the market closes. Ahead of the event, analysts expect Hartford Insurance to report a profit of $3.24 per share on a diluted basis, down 5% from an EPS of $3.41 in the year-ago quarter. The company has a mixed history of earnings surprises, surpassing Wall Street’s EPS estimates in three of four quarterly reports and missing on one other occasion.

Looking ahead to fiscal 2026, analysts expect Hartford Insurance to report EPS of $12.90, up 3.9% from $13.42 in fiscal 2025. However, its EPS is expected to rise 9.6% YOY to $14.14 in fiscal 2027.

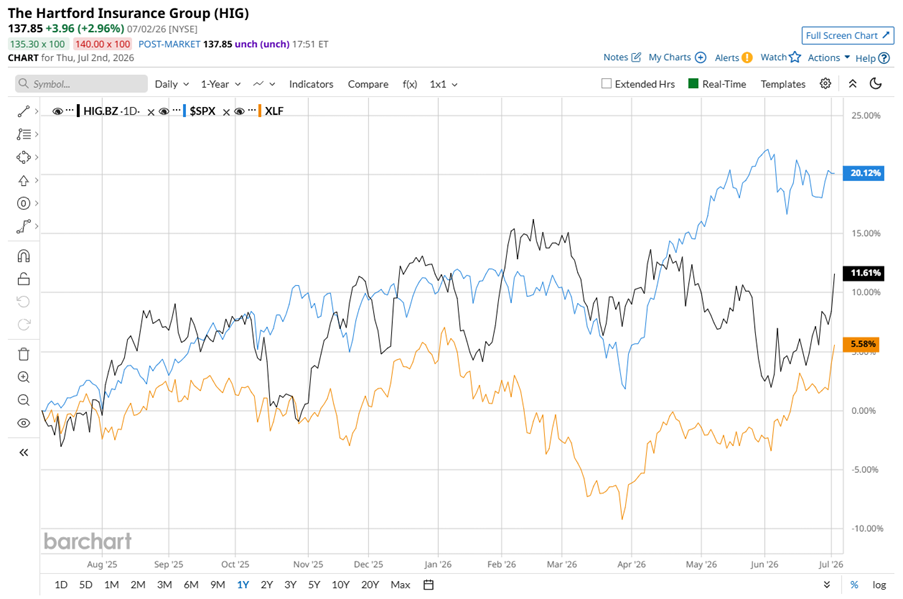

Shares of Hartford Insurance have underperformed the S&P 500 Index’s ($SPX) 20.2% gains over the past 52 weeks, with shares up only 12.2% during this period. However, HIG outperformed the State Street Financial Select Sector SPDR ETF’s (XLF) 5.7% gains over the same period.

Hartford has not given investors many reasons to chase the stock lately. A setback came after its first-quarter 2026 earnings, when core EPS of $3.09 missed Wall Street’s expectations, even though it rose 40% annually. While operating revenue rose 7% YOY to $5.09 billion, it also came in below estimates, suggesting that growth was not as strong as investors had hoped.

The report also highlighted rising cost pressures. Total benefits, losses, and expenses climbed; the Employee Benefits expense ratio increased to 26.7%, driven by higher staffing costs and higher technology costs; and the Business Insurance combined ratio reached 94.8, coming in above expectations. Those numbers raised concerns that higher claims and operating costs could weigh on profitability, helping explain why HIG has lagged the broader market.

Analysts’ consensus opinion on HIG stock is moderately bullish, with a “Moderate Buy” rating overall. Out of 26 analysts covering the stock, 11 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and 14 give a “Hold.” HIG’s average analyst price target of $148 suggests that the stock has upside potential of 7.4% from current price levels.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)