U.S. stocks are set to close the first half of the year in the green despite turmoil from the Iran war and the resultant rise in gas prices, intermittent fears of an artificial intelligence (AI) bubble, trade tensions, and noise over China’s slowdown. However, the tide hasn’t lifted all boats.

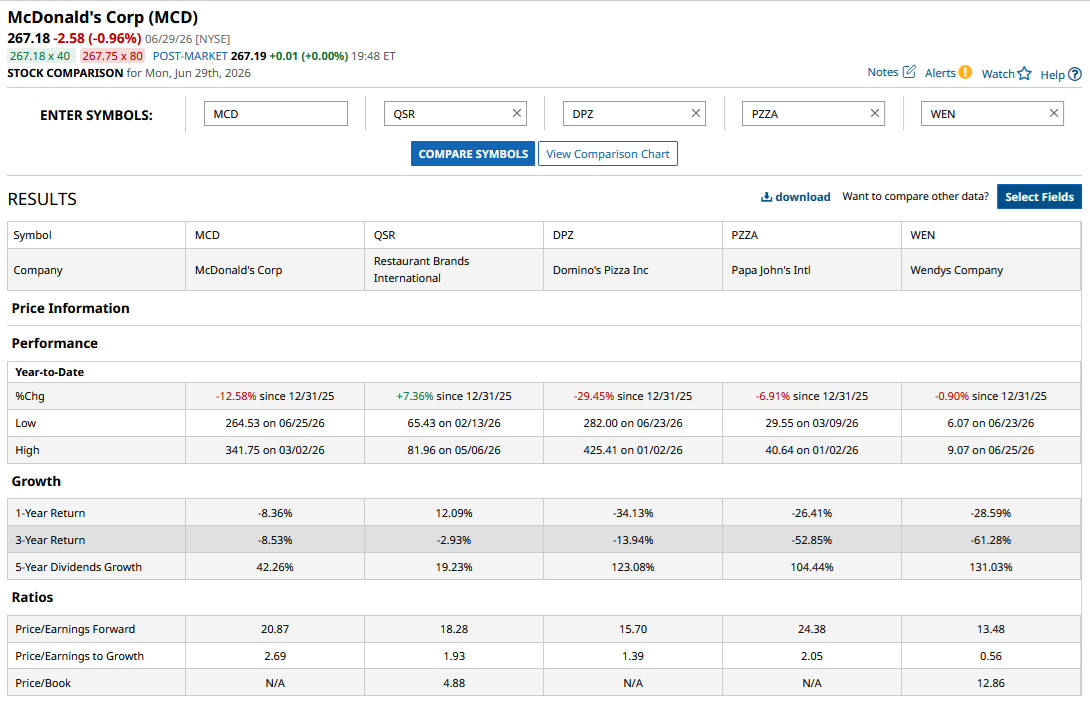

McDonald’s (MCD) is down more than 11% so far this year. MCD stock is trading near its 52-week low and also down 7% over the last three years, underperforming its average S&P 500 Index ($SPX) peer by a wide margin during the period. Back in May, I noted that MCD stock did not look like a buy yet despite the crash. With shares coming off those levels, let’s take a look at whether McDonald's stock is in the buy zone now.

McDonald’s Dividend History

To begin, let’s look at the dividend history of the company. McDonald's started paying a dividend in 1976 and has increased it every year since. It is currently a “Dividend Aristocrat” and on the verge of becoming a "Dividend King," meaning it will join a group of roughly five dozen companies that have raised their dividends for 50 consecutive years.

Over the last five decades, there have been some major financial crises, including the dot-com bust, the 2008 housing market crash, and the Covid-19 pandemic, not to mention many recessions and wars. However, McDonald’s has continued to raise dividends over this time.

The company’s dividend payout ratio is around 58.4%, which looks comfortable and leaves some scope for growth as well as share buybacks. Currently, McDonald’s pays a quarterly dividend of $1.86, which implies a dividend yield of 2.78%. The payouts have risen at an annualized pace of 7.4% over the last five years, and while the growth is not eye-popping, it’s decent considering the company’s mature business.

Valuations Have Corrected

While McDonald’s has been gradually increasing its dividends, MCD stock has sagged, which has pushed its dividend yield to a multi-year high. At the same time, its valuations have also corrected. The stock is the cheapest it has been in years at a forward price-to-earnings (P/E) multiple of 20.6 times.

McDonald’s is a free-cash-flow powerhouse, so it would be pertinent to look at that metric as well. In 2025, the company generated free cash flow (FCF) of $7.2 billion, up about 8% from the previous year. Based on 2025 FCF, McDonald's has a trailing price-to-FCF multiple of 26.7 times. The valuations of MCD stock appear reasonable even though they are not mouthwateringly cheap yet.

What Do Analysts Think of MCD Stock?

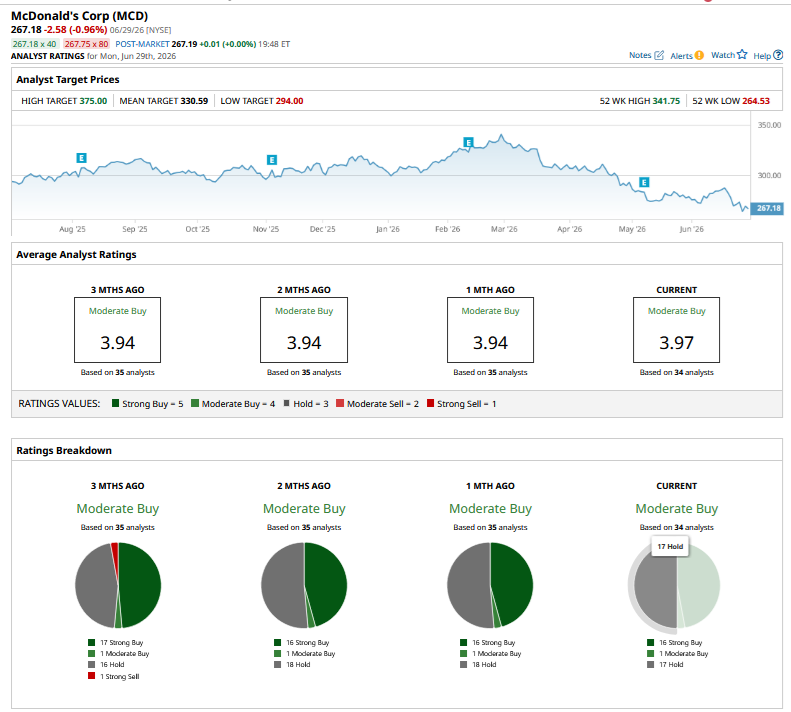

Currently, MCD stock trades below its Street-low target price of $286 per share, while the mean target of $329.88 implies 22% potential upside from current price levels. While a stock trading below what even the most bearish sell-side analyst thinks it is worth may signal a tempting buy, the price targets of analysts are fluid and subject to revision.

The recent trend in MCD price targets has been downward, with KeyBanc lowering its target from $330 to $315 on June 29 while maintaining an “Overweight” rating. Previously, several brokerages — including Wells Fargo, JPMorgan Chase, and RBC — also lowered their target prices following the company's first-quarter 2026 earnings report in May.

While McDonald's reported better-than-expected earnings in Q1, management’s cautious tone on the Q2 outlook spooked markets. The company highlighted that higher gas prices are impacting its customer base, which is hurting sales. On the Q1 earnings call, commenting on consumer sentiment, CEO Christopher Kempczinski said that “it's certainly not improving, and it may be getting a little bit worse.”

Will Things Get Better for McDonald’s in H2?

Crude oil prices are now near pre-war levels, which is a big relief not only for consumers but also for many countries, as higher oil prices were putting pressure on their fiscal positions. While an Iran peace deal would always be fragile, markets don’t see it taking a major toll on energy prices, at least for the time being.

With gas prices coming down, pressure on monthly budgets should also ease, which is positive for restaurant chains like McDonald’s. As for the outlook of MCD stock, I am on the same page as fellow Barchart contributor Mark Hake, who believes that MCD might have bottomed. While I don’t expect a stellar back-half rally in McDonald's stock, I believe dividend investors can start accumulating shares at these levels while using any weakness amid the broader market correction to add more shares.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)