Shares of GE Aerospace (GE) have been on an impressive run, fueled by strong demand across the commercial aviation and defense markets. The company, which retained the iconic "GE" ticker after General Electric completed its historic three-way split in 2024, inherited the conglomerate's aerospace operations and has since emerged as a pure-play aviation leader. That strategy is paying off, with GE Aerospace building an impressive backlog of more than $210 billion, including over $170 billion in commercial services, providing significant long-term revenue visibility.

The company continues to benefit from powerful industry tailwinds. A sustained recovery in global air travel, the replacement of aging aircraft with newer, more fuel-efficient models, and rising U.S. defense spending over the past several years have created significant growth opportunities across both its commercial and defense businesses. As one of the world's leading manufacturers of jet engines, GE Aerospace is well positioned to capitalize on strong demand for aircraft propulsion systems and the high-margin aftermarket services that support them.

With the stock now trading near record highs and the aerospace industry enjoying favorable demand trends, investors are now awaiting the company's next major catalyst. GE Aerospace is scheduled to report its fiscal 2026 second-quarter earnings before the market opens on Thursday, July 16, making it an opportune time to take a closer look at the stock.

About GE Aerospace Stock

GE Aerospace is a leading global aerospace company that designs, develops, manufactures, and services aircraft engines, integrated aircraft systems, and advanced aerospace technologies for commercial, defense, and business aviation customers. The company's roots trace back to General Electric, founded in 1892, while its aviation business began in 1917 with the launch of its aircraft engine division. In April 2024, GE Aerospace emerged as an independent, publicly traded company following the separation of General Electric into three standalone businesses.

Operating across key segments of the aerospace industry, including commercial aviation, military and defense, business and general aviation, and advanced aerospace technologies, GE Aerospace has established itself as a global leader in aviation innovation. Today, the company generates more than $30 billion in annual revenue and provides a comprehensive portfolio of engines, systems, and services.

It designs, develops, and manufactures jet engines, components, and integrated systems for military, commercial, business, and general aviation aircraft, as well as aero-derivative gas turbines for marine applications. Beyond manufacturing, GE Aerospace is also the world's leading integrated engine maintenance resource, delivering maintenance, repair, and overhaul services that help customers maximize engine performance, reliability, and operational efficiency throughout their lifecycle.

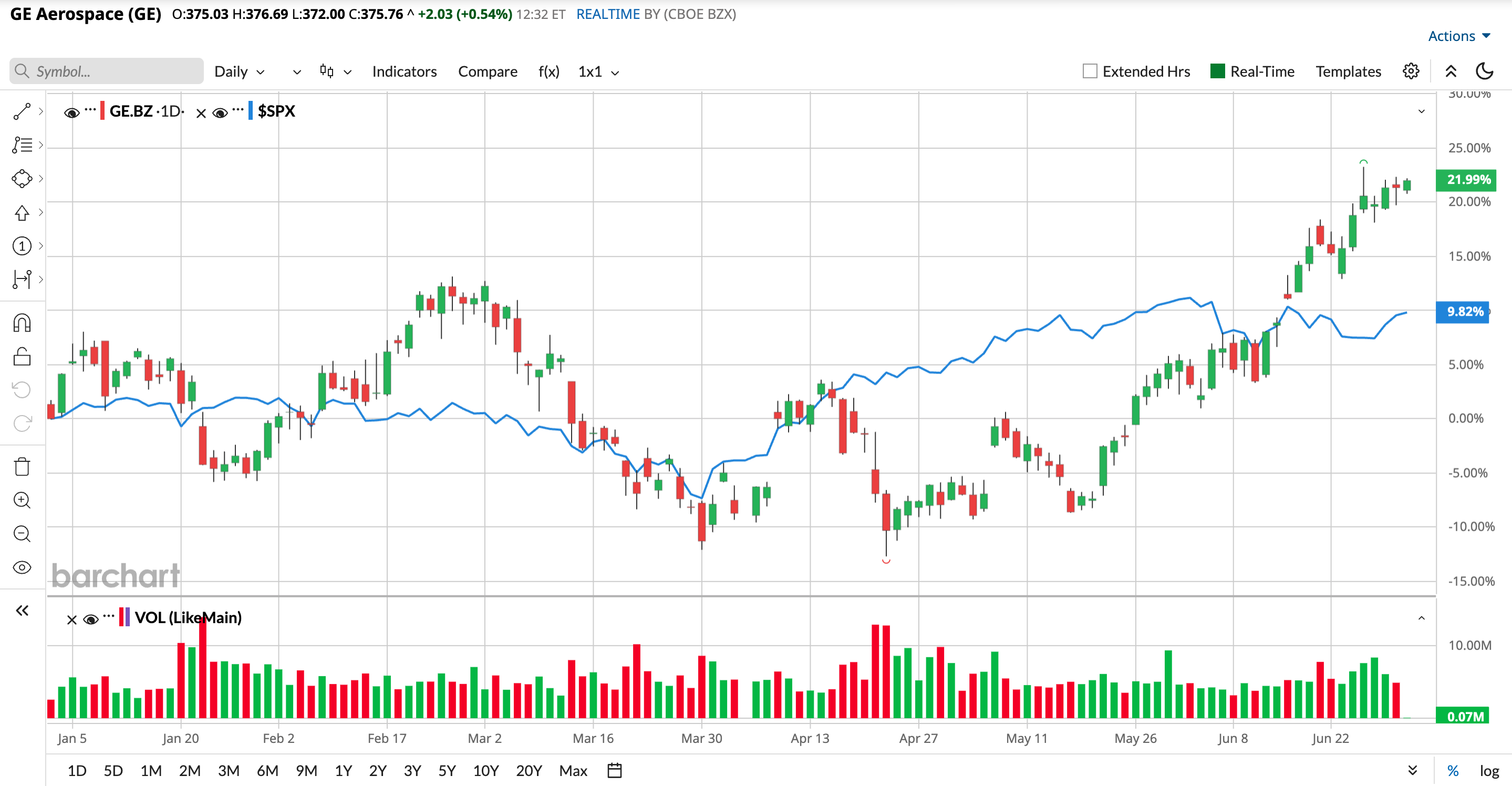

Investor enthusiasm has propelled GE Aerospace to new heights. With a market capitalization of $389.9 billion, the aerospace and defense giant has significantly outpaced the broader market. Over the past year, GE shares have rallied 50.9%, handily beating the S&P 500 Index's ($SPX) 21.2% gain. The momentum has remained intact in 2026, with the stock advancing 22% year-to-date (YTD), compared with the broader market's 9.7% return. GE Aerospace also climbed to a record high of $379.67 on June 25 and currently sits a marginal 0.98% below that peak, underscoring its strong upward trajectory.

Inside GE Aerospace’s Q1 Earnings Report

GE Aerospace kicked off fiscal 2026 on a high note, delivering a first-quarter earnings report on April 21 that comfortably surpassed Wall Street's top- and bottom-line expectations. The strong performance was fueled by relentless global demand for aircraft engine servicing and a significant expansion in defense contracts. Total GAAP revenue surged 25% year-over-year (YOY) to $12.4 billion, while adjusted revenue climbed an even stronger 29% to $11.6 billion, handily exceeding analysts' consensus estimate of $10.64 billion.

Profitability was equally impressive. Powered by high-margin aftermarket services, GE Aerospace reported adjusted earnings per share (EPS) of $1.86, up 25% from $1.49 a year ago and well ahead of Wall Street's estimate of $1.61. The results highlighted the company's strong pricing power and operating leverage as robust demand continued to drive higher-margin service revenue.

The standout performer was the Commercial Engines & Services (CES) segment, where total orders nearly doubled, soaring 93% YOY to $17.3 billion. Revenue climbed 34% to $8.9 billion, driven by broad-based strength across the business. Services revenue increased 39%, supported by a 35% rise in internal shop visit revenue and spare parts revenue growth of more than 25%. Equipment revenue also advanced 20%, benefiting from a 50% increase in unit volumes, partially offset by customer mix.

Momentum was equally strong in the Defense & Propulsion Technologies (DPT) segment. Quarterly orders jumped 67% to $6.2 billion, while revenue rose 19% to $3.2 billion. Defense & Systems revenue increased 14%, reflecting growth in both services and equipment, including a 24% rise in deliveries. Meanwhile, Propulsion & Additive Technologies revenue climbed 29%, with growth across all businesses led by Avio Aero.

Beyond the strong operating performance, GE Aerospace's cash generation remained a key highlight. Free cash flow increased 14% YOY to $1.66 billion in the quarter, underscoring the strength of the company's business model. In addition to this robust start to the year, management said full-year fiscal 2026 results are trending toward the higher end of its guidance. This calls for operating profit of up to $10.25 billion, adjusted EPS of $7.10 to $7.40, and is supported by a commercial services backlog exceeding $170 billion, leaving the company well positioned to navigate a dynamic macroeconomic environment.

How Do Analysts View GE Aerospace Stock?

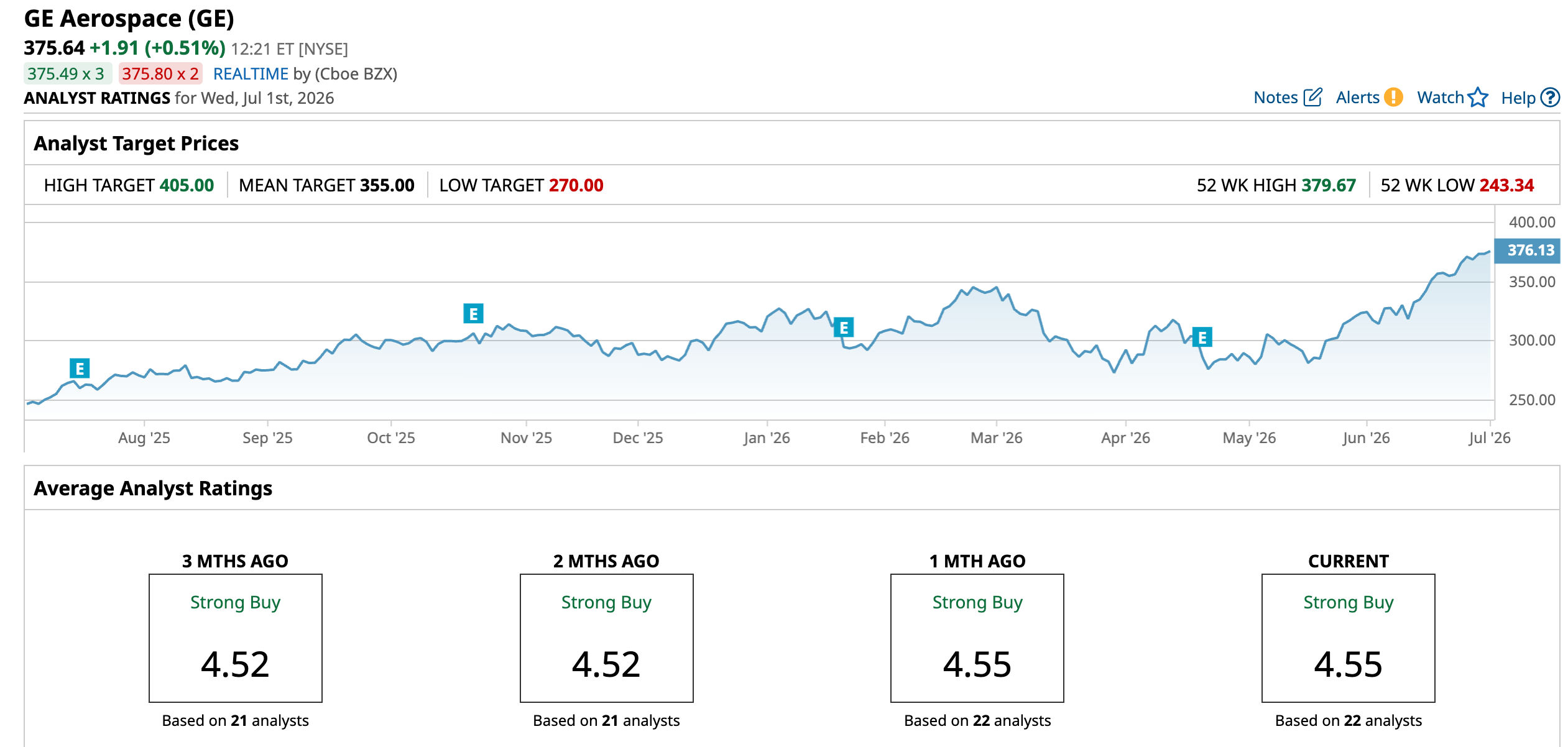

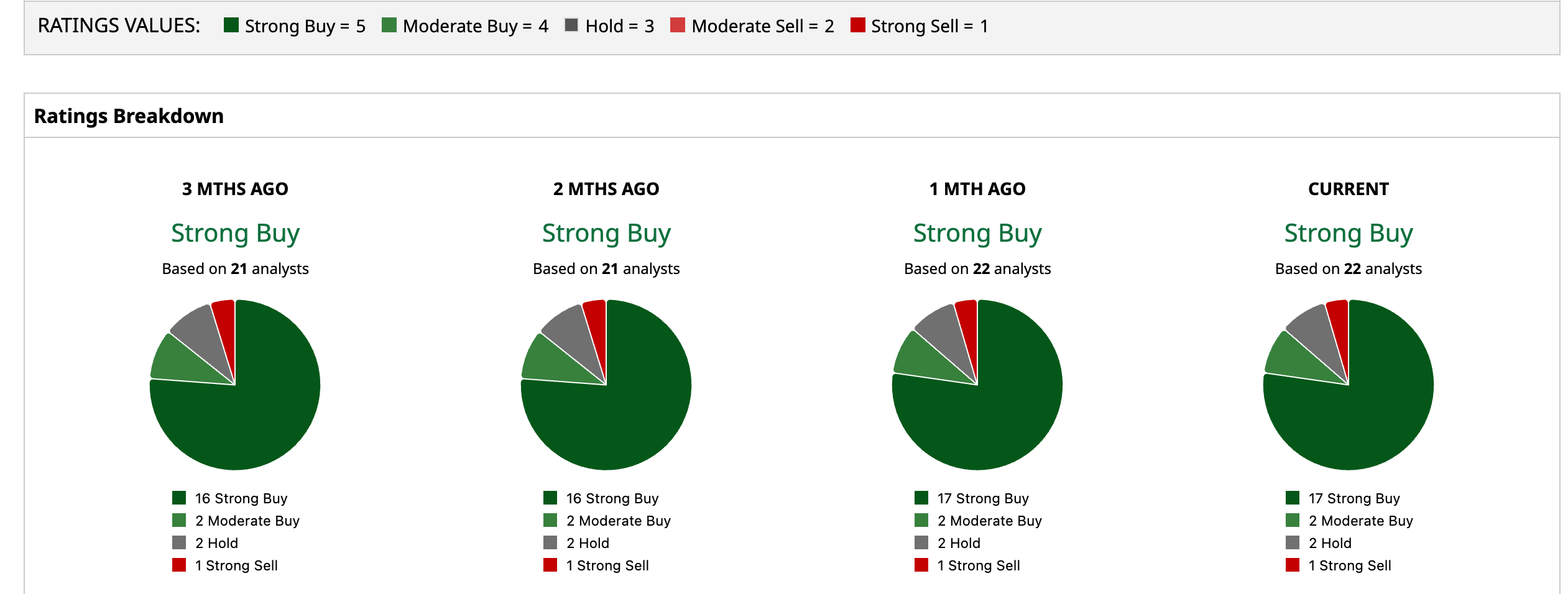

As GE Aerospace gears up to report its second-quarter earnings later this month, Wall Street's confidence in the aerospace giant remains firmly intact. The stock carries a consensus "Strong Buy" rating, with 17 of the 22 analysts covering the company recommending a "Strong Buy." Another two rate it "Moderate Buy," two maintain "Hold" ratings, and only one analyst remains bearish with a "Strong Sell" recommendation.

Notably, GE Aerospace has already surpassed the Street's average price target of $355, reflecting the stock's powerful rally. However, the highest price target on Wall Street stands at $405, suggesting there could still be 7.82% upside from current levels.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)