/The%20Adobe%20logo%20on%20a%20smartphone%20screen%20by%20filins%20via%20Adobe%20Stock.jpeg)

Adobe (ADBE) recently announced a definitive agreement to acquire Topaz Labs, which is poised to fit well into its business. While Adobe’s Firefly platform generates new content from scratch, Topaz Labs makes models that improve existing visual content. Accordingly, the acquisition will allow Adobe to offer both content creation and content enhancement, giving users a more complete creative workflow. The deal is expected to close in the second half of 2026, with Topaz Labs CEO Eric Yang set to continue leading post-acquisition.

RBC Capital Markets analyst Matthew Swanson sees this news as positive, providing a price target of $285 for ADBE stock and an “Outperform” rating. He believes Adobe is making the right strategic decision by focusing on content quality rather than quantity. Swanson also believes that professional users and enterprises will be willing to pay for high-end features for a considerable upgrade in the quality of their work. The analyst added that proving clear value from AI tools should drive long-term growth for Adobe.

Adobe made other strategic changes prior to the Topaz Labs deal as well. At the Cannes Lions 2026 event, the company announced agentic AI partnerships with the world’s leading marketing firms, including Accenture (ACN), Omnicom (OMC), Stagwell (STGW), and WPP (WPP). These firms are using Adobe’s content, data, and AI platforms to help major brands improve content and track how customers engage with it. Adobe considers itself the unifying AI layer across the creative and marketing industry — and with the Topaz Labs acquisition, it has added another powerful tool to strengthen that vision.

About Adobe Stock

Adobe is a software company that develops digital media, marketing, and creative solutions globally. Its product portfolio includes Photoshop, Acrobat, Premiere Pro, Adobe Experience Cloud, Illustrator, and Firefly, among others. Founded in 1982, the company is headquartered in San Jose, California, and currently led by CEO Shantanu Narayen. In March 2026, Narayen announced that he would be stepping down after an 18-year tenure once a successor is appointed.

Over the last 12 months, ADBE stock has almost halved, dropping 47% and significantly underperforming the S&P 500’s ($SPX) 21% rise during the same period. Currently near its 52-week low of $190.12, the stock has continued to decline after major leadership changes, with the CEO set to step down and CFO Daniel Durn’s sudden departure in June. Still, shares were already suffering due to concerns around AI and tools like Canva replacing Adobe’s subscription products.

By most measures, investors seem to be undervaluing Adobe. The forward price-to-earnings (P/E) ratio of 10.2 times sits at less than a third of both the sector median and the company’s own five-year average, indicating the stock is trading at a considerable discount to historical norms. The price-to-sales (P/S) ratio of 3.3 times also sits well below the five-year average of roughly 10 times. For a company of this scale and position, that is genuinely cheap. Adobe's EPS growth trajectory is expected to remain positive for years to come, with growth of 15% expected in fiscal 2026 and 13% in fiscal 2027. Capital structure isn’t a major concern, either, with net debt of $1 billion against an $82 billion market capitalization.

Despite all this and Adobe's strong revenue and earnings performance, the company's leadership changes and “freemium ”strategy — which is expected to initially reduce paid subscriptions — have made investors reluctant to bet on ADBE stock. However, with a mean price target implying 34% potential upside from current levels, most on Wall Street believe this might be a good time for investors to enter.

Adobe Reports Strong Earnings, But ADBE Stock Continues to Slide

Adobe reported second-quarter fiscal 2026 earnings on June 11. Revenue came in at $6.62 billion, beating the analyst consensus estimate of $6.45 billion, up 13% year-over-year (YOY). Non-GAAP EPS of $5.96 also outperformed the $5.81 consensus estimate, up 18% YOY. Narayen credited “strong AI-driven demand” for the record quarterly revenue as well as for the full-year fiscal 2026 guidance raise. Adobe’s AI-first ARR also surpassed the $500 million milestone during the period, tripling YOY. On the earnings call, management announced a shift toward a “freemium” model, acknowledging that acquiring new users would lower second-half ARR growth expectations.

For Q3, Adobe guided revenue of $6.67 billion to $6.72 billion and non-GAAP EPS of $6.05 to $6.10. For the full year, Adobe also raised its guidance to $20.5 billion to $20.6 billion in revenue and non-GAAP EPS of $24.35 to $24.45. Interim CFO Steven Day attributed the firm's conservative ARR 10.2% growth target to the Semrush acquisition and the strategic decision to prioritize freemium growth over short-term subscription revenue. When asked about continuity amid Adobe's major leadership changes, Narayen expressed confidence in existing leadership to transition smoothly without disrupting its operations.

What Are Analysts Saying About Adobe Stock?

Following earnings, Stifel Nicolaus analyst J. Parker Lane drastically reduced the firm's price target from $350 to $200 while also downgrading ADBE stock from a “Buy” to a “Hold” rating. The analyst cited low organic ARR guidance for the second half of the year as a reason for the downgrade. Lane also highlighted that the recent CFO departure adds uncertainty to Adobe’s leadership. Meanwhile, Phillip Securities analyst Paul Chew set a much higher target of $385 on ADBE stock while maintaining a “Buy” rating, citing strong Creative Cloud Pro adoption and an increase in freemium users positively contributing to Adobe’s growth and valuation.

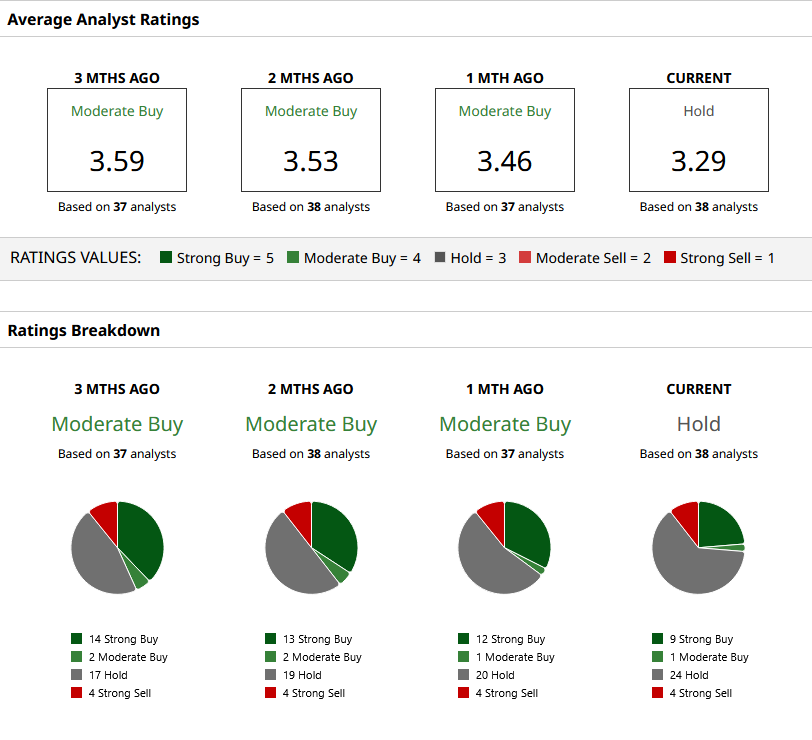

Based on 37 analysts with coverage, Adobe has a consensus “Hold” rating with a mean price target of $273.97, indicating 34% potential upside. Adobe stock currently sits near the low price target of $190. Still, with a high price target of $460 and healthy upside expected, many analysts believe investors are undervaluing a company that has consistently beaten on revenue and earnings.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)