Valued at $26 billion by market cap, Fiserv, Inc. (FISV) is a leading financial technology company that provides payment processing, banking, and digital financial services to banks, credit unions, merchants, and businesses worldwide. The Milwaukee, Wisconsin-based company’s solutions span core banking software, card and payment processing, digital banking, e-commerce, and point-of-sale systems. Through its well-known platforms, including Clover and Carat, Fiserv helps financial institutions and merchants process transactions, manage accounts, and deliver digital payment experiences.

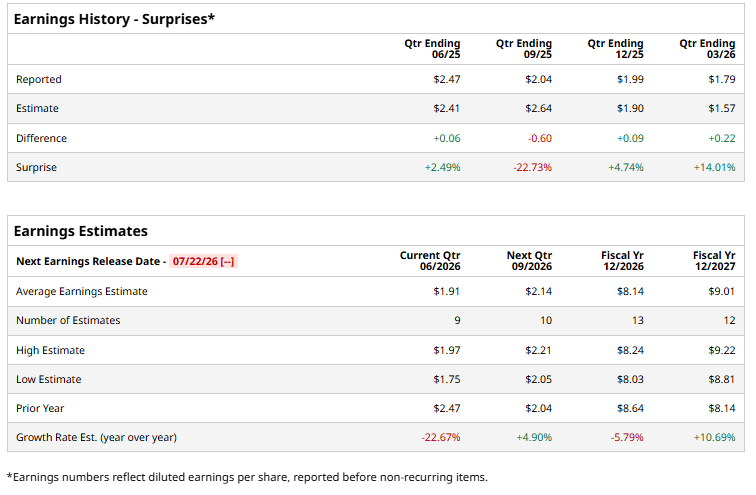

The fintech giant is expected to announce its fiscal 2026 second-quarter earnings in the near term. Ahead of the event, analysts expect FISV to report a profit of $1.91 per share on a diluted basis, down 22.7% from $2.47 per share in the year-ago quarter. The company beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

For the current year, analysts expect FISV to report EPS of $8.14, down 5.8% from $8.64 in fiscal 2025. However, its EPS is expected to rise 10.7% year over year to $9.01 in fiscal 2027.

Over the past 52 weeks, FISV has been a notable underperformer, with shares tumbling 71.6%. In comparison, the S&P 500 Index ($SPX) gained 20.9%, while the State Street Technology Select Sector SPDR Fund (XLK) advanced 50.5% during the same period.

On June 17, Fiserv shares rose 2.9% after the company launched a cash tender offer to repurchase up to $2.75 billion of its senior notes, a move aimed at refinancing debt with lower-cost euro-denominated notes. Investor sentiment was further boosted by multiple insider stock purchases, helping restore confidence following the recent surprise resignation of the company's CEO.

Analysts’ consensus opinion on FISV stock is cautious, with a “Hold” rating overall. Out of 34 analysts covering the stock, four advise a “Strong Buy” rating, two suggest a “Moderate Buy,” 25 give a “Hold,” and three recommend a “Strong Sell.” FISV’s average analyst price target is $66.75, indicating a potential upside of 36.1% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)