/Wall%20Street%20sign%20in%20New%20York%20City%20financial%20district%20by%20ChayTee%20via%20Adobe%20Stock.jpeg)

BTIG analyst Andrew Harte initiated coverage of Robinhood Markets (HOOD) with a “Buy” rating, estimating that the platform’s assets will achieve extraordinary growth of over 20% annually over the next decade. Harte identified four key growth drivers for his positive outlook. First, because Robinhood’s user base largely consists of youngsters, the audience will earn and invest more as they mature. Second, existing users are becoming more engaged with the platform than before. Third, new customers are joining at a healthy rate. And fourth, the company’s product and international expansion.

The analyst stated that Robinhood, processing 818 million options contracts, is already comfortably ahead of the analysts’ estimate of 671 million. Harte also expects additional growth opportunities with Robinhood introducing Trump Accounts, prediction markets, and potentially removing pattern day restrictions that currently limit how frequently smaller investors can trade. The company is also diversifying into countries other than the U.S., increasing its total addressable market. Robinhood has also been expanding into agentic AI, giving users the ability to let AI manage their banking and trading activities.

Meta Platforms (META) also recently announced plans to build a competing prediction markets app. Harte, however, believes Robinhood’s growth prospects remain exceptional for several years and feels confident in his “Buy” rating.

About Robinhood Stock

Robinhood is a financial services company that allows retail investors to trade stocks, ETFs, options, and cryptocurrencies through its mobile app and online platform. The company also offers digital banking, credit cards, crypto wallets, and retirement accounts. Founded in 2013, Robinhood is headquartered in Menlo Park, California, and is led by co-founder, Chairman, and CEO Vlad Tenev.

Robinhood’s stock story has been fairly dramatic. Over the last 12 months, the stock has increased just a little over 20%, almost matching the S&P 500’s ($SPX) 20% during the same period. HOOD stock has been volatile throughout the year and had a freefall, crashing nearly 40% from mid-January to early February after crypto prices fell sharply. Some positive momentum was built leading up to the SpaceX (SPCX) IPO as trading activity increased due to the resulting hype. The company also announced just before the IPO that it had received regulatory approval to operate as an IPO underwriter in the future.

Robinhood’s valuation reflects the market’s confidence in its long-term growth potential rather than current earnings. The forward GAAP P/E of 50.10x is difficult to interpret given Robinhood’s recent path to profitability. The forward price-to-sales (P/S) ratio of 16.79x is a more meaningful metric, trading at a premium to its 5-year average of 10.84x. The premium is driven primarily by Trump Accounts, prediction markets, and international expansion, opening new growth opportunities for the firm.

The near-term EPS trajectory shows a modest 9% decline in 2026 due to the $100 million investment in building Trump Accounts infrastructure. As the new products begin increasing revenue, the EPS is estimated to strongly recover, with a 37% growth in 2027. The capital structure offers further justification for the premium, with Robinhood having $19.27 billion in cash against $13.61 billion in debt. For a company with an $87.52 billion market cap, being $5.66 billion net cash positive is an exceptional position to be in.

Robinhood Misses Wall Street Consensus

Robinhood reported its first-quarter fiscal 2026 earnings on April 28. The firm missed analyst consensus on both key metrics but still improved year-on-year (YoY). A revenue of $1.07 billion was reported, representing a 15% YoY growth. The diluted EPS also increased to $0.38, up 3% from the same quarter last year. Apart from the cryptocurrency revenue being 47% down, the firm saw revenue growth in most segments. Robinhood Gold subscription revenue increased 32% to $50 million. Other transaction revenue, driven primarily by event contracts revenue, skyrocketed 320% to $147 million. CEO Vlad Tenev stated that record levels were seen in Prediction Markets, Futures, Index Options, Shorting and Margin. Tenev also mentioned that since the last earnings, Robinhood Banking has grown five times.

For the second quarter, the management has guided revenue of approximately $1.23 billion and an EPS of $0.45, reflecting a positive outlook. CFO Shiv Verma noted that the company is off to a good start in April, with equity and trading volumes on track to be the highest of the year. The company is investing $100 million into building Trump accounts, with the CFO stating that the revenue is expected to exceed costs. Prediction Markets are also recovering strongly, with volumes in April on track to hit approximately $3 billion. Verma said that Robinhood investing for the long term and shipping products faster than ever brings massive growth opportunities moving forward.

What Analysts Are Saying About HOOD Stock

BTIG analyst Andrew Harte initiated coverage with a “Buy” rating, projecting the annual asset growth to be over 20% for the next decade. Argus analyst Stephen Biggar also raised his price target from $90 to $110 while maintaining a “Buy” rating. Similar to Harte, Biggar also expects Robinhood to be in high-growth mode for the next few years. The analyst raised his EPS estimates due to lower headcount costs expected after Robinhood announced a 10% workforce reduction.

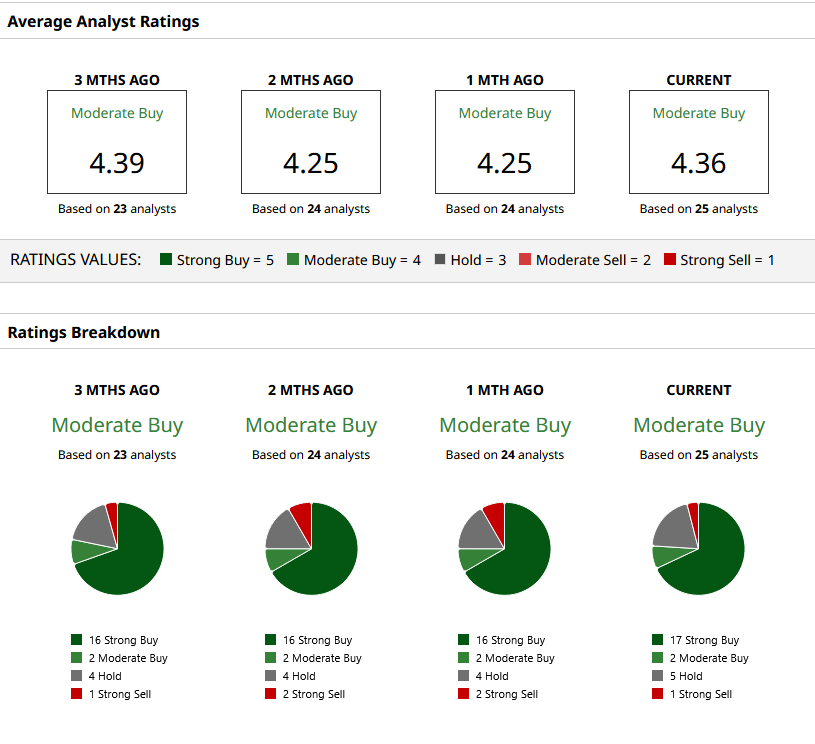

Based on the 25 Wall Street analysts tracked by Barchart, HOOD stock holds a consensus “Moderate Buy” rating with a mean price target of $105.08, indicating a 5% upside. Out of those 25 analysts, 17 suggest a “Strong Buy” and only one suggests a “Strong Sell,” reflecting that confidence in Robinhood's stock remains strong on Wall Street.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)