/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

Microsoft (MSFT) is a legacy tech player that has been in business for over 51 years. It develops software, cloud computing services, artificial intelligence (AI) platforms, business applications, gaming products, and hardware. MSFT stock, which has returned roughly 629% over the last decade, has taken a hit so far this year, with shares down 22% year-to-date (YTD).

June has been the company's worst month, with the stock reaching a new low of $349.20 last week. But that doesn’t mean Microsoft’s business suddenly deteriorated. Instead, the decline was fueled by a broader selloff in AI and mega-cap tech stocks. While the market is repricing MSFT stock, savvy investors should see this as a long-term opportunity to scoop up this legacy tech giant’s shares.

What Triggered the June Selloff?

The June tech selloff echoes the market rotation that happened earlier this year. Investors are once again moving out of lofty-priced AI giants as focus shifts from geopolitical tensions to whether Big Tech’s massive spending can generate enough profits to justify the rich valuations.

Ironically, while investors have punished Microsoft over concerns about its massive AI spending, Goldman Sachs believes hyperscaler investment is only accelerating. The investment bank predicts that AI infrastructure spending will enter a multiyear "capex supercycle," reaching $757 billion in 2026, before climbing to $920 billion in 2027. In fact, the firm says that combined capex from four tech giants, Meta (META), Microsoft, Amazon (AMZN), and Alphabet (GOOG) (GOOGL), is expected to reach $5.3 trillion by the end of 2030.

Microsoft alone has guided for roughly $190 billion in capital expenditures in fiscal 2026, an enormous increase from prior years, as it builds AI data centers and infrastructure. Goldman Sachs believes that Microsoft's aggressive investment may ultimately strengthen its long-term competitive position despite weighing on the stock in the short term.

But MSFT Stock Is No Longer Too Expensive

While valuation has been a concern for the June tech selloff, MSFT stock currently trades at 22x forward earnings, much lower than its five-year average of 30x. For a company expected to grow earnings per share (EPS) more than 23% this year, Microsoft's valuation doesn't look lofty anymore. So, why is the stock falling? Basically, investors now aren’t willing to pay any premium until Microsoft proves that its $190 billion of AI capex translates into much higher earnings.

Essentially, Microsoft entered 2026 with a premium valuation, but months of selling have now compressed its valuation. In fact, Benchmark analyst Yi Fu Lee said that Microsoft’s forward P/E of 22x, versus a technology sector median of roughly 32x, has created an attractive valuation rather than an overvalued one. Lee strongly believes that MSFT stock remains “one of the highest-quality ways” to gain exposure to the AI boom.

What’s Happening With the Business?

Microsoft’s underlying business continues to grow stronger than ever, with rapid adoption of its AI products. In the third quarter of fiscal 2026, Microsoft Cloud revenue grew 29% year-over-year (YoY) to $54.5 billion, and its AI business surpassed $37 billion in annual recurring revenue (ARR), soaring 123% YoY.

Azure, the company's cloud computing engine, continues to rank second in the global cloud computing industry, with a 21% share. Azure grew 40% YoY as customer demand across AI and non-AI workloads continues to exceed available capacity. Despite aggressively expanding its infrastructure, management expects supply to remain constrained throughout 2026. In the third quarter, total revenue increased 18% YoY to $82.9 billion, while EPS climbed 21% to $4.27, comfortably exceeding expectations. However, free cash flow dipped to $15.8 billion as Microsoft ramped up AI infrastructure spending. The company spent $31.9 billion in capital expenditures in the quarter, with roughly two-thirds allocated to GPUs and CPUs. Management defended the $190 billion in capex for 2026 by claiming that these expenditures are supported by stronger demand signals, increased AI product adoption, and improved platform efficiency, while maintaining confidence in achieving attractive long-term returns.

Ironically, while the companies footing the bill for AI infrastructure are facing investor skepticism, many of their suppliers continue to rally. Goldman Sachs has identified a few select tech companies that are poised to benefit from this multiyear AI capex cycle. With Azure demand still exceeding supply, AI revenue growing at triple-digit rates, commercial backlog reaching $627 billion, and management guiding for another year of double-digit growth, the underlying fundamentals remain intact. In my opinion, this pullback is a great opportunity to buy a quality AI stock whose performance continues to outpace the market's near-term concerns.

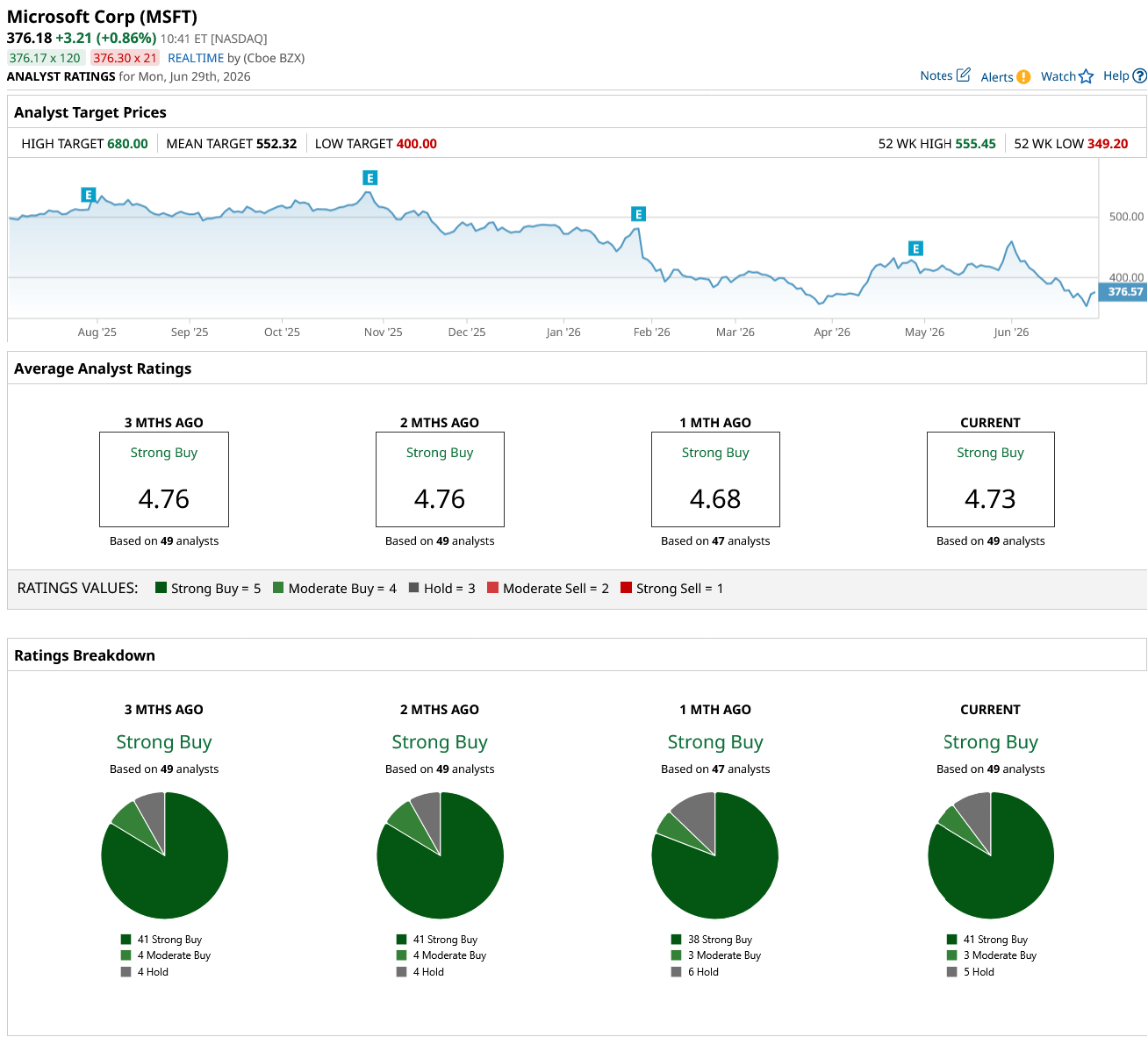

Overall, MSFT stock remains a “Strong Buy” on Wall Street. Of the 49 analysts covering the stock, 41 rate it a “Strong Buy,” three say it is a “Moderate Buy,” and five rate it a “Hold.” Although the stock has fallen 16% so far in June, analysts see the stock rebounding around 47% to hit $552.32. Plus, its high price estimate of $680 implies the stock has an upside potential of 81% over current levels.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)