/AI%20(artificial%20intelligence)/3D%20Graphics%20Concept%20Big%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Sunrun (RUN) shares soared on Wednesday after the residential solar firm announced a framework agreement with Tesla (TSLA) and Renew Home to aggregate more than 16 GW of flexible energy capacity for hyperscalers and utilities.

The partnership pools hundreds of thousands of home battery systems operated by RUN and TSLA with more than 8 million smart thermostats and devices managed by Renew Home — creating what the companies describe as the country’s largest distributed power plant.

Importantly, the arrangement requires no additional hardware, software, interconnection, water, or land from offtakers, allowing deployment in months rather than years.

Despite its meteoric rally on June 24, Sunrun stock remains down more than 30% versus its YTD high.

Sunrun Stock Looks Poised for Continued Gains

Sunrun’s deal with Tesla and Renew Homes is squarely aimed at the explosive electricity demand from artificial intelligence (AI) data centers.

Goldman Sachs projects U.S. data center power demand will reach 41 GW this year and 66 GW in 2027, creating a structural supply gap that traditional centralized generation can hardly fill quickly enough.

The Department of Energy further estimates that data centers could account for up to 12% of total U.S. electrical demand by 2028, underscoring the urgency of the opportunity RUN stock is targeting.

Should You Load Up on RUN Shares Today?

In Virginia’s Data Center Alley, the partners already have more than 300 megawatts available for immediate deployment, with a target of at least 500 MW by the end of this decade.

These three firms have also committed capacity to PJM’s proposed Reliability Backstop Process, which could unlock over a gigawatt for peak shaving, locational grid relief, and ancillary services.

Capacity for hyperscalers will be allocated on a first-come, first-served basis, further reflecting the urgency of demand.

The partnership reframes Sunrun’s business narrative from a struggling residential solar installer into a potential distributed-grid operator with recurring revenue tied to AI-driven power demand.

Its Q1 results already showed momentum, with revenue of $722 million representing 43% year-over-year growth and a record 73% storage attachment rate.

A Brattle Group analysis referenced by the partners estimates that better grid utilization could reduce U.S. electricity bills by at least $110 billion over the next decade, reinforcing the “value proposition” for both hyperscalers and residential customers.

Sunrun Remains Buy-Rated Among Wall Street Firms

Retail sentiment on Sunrun turned visibly bullish after the Tesla-Renew Home deal, with short-squeeze speculation emerging on social media platforms.

However, investors should recognize important caveats as well. This is a capacity framework, not a collection of signed hyperscaler sales contracts, and execution depends on customer enrollment, utility program approvals, and regulatory clearance.

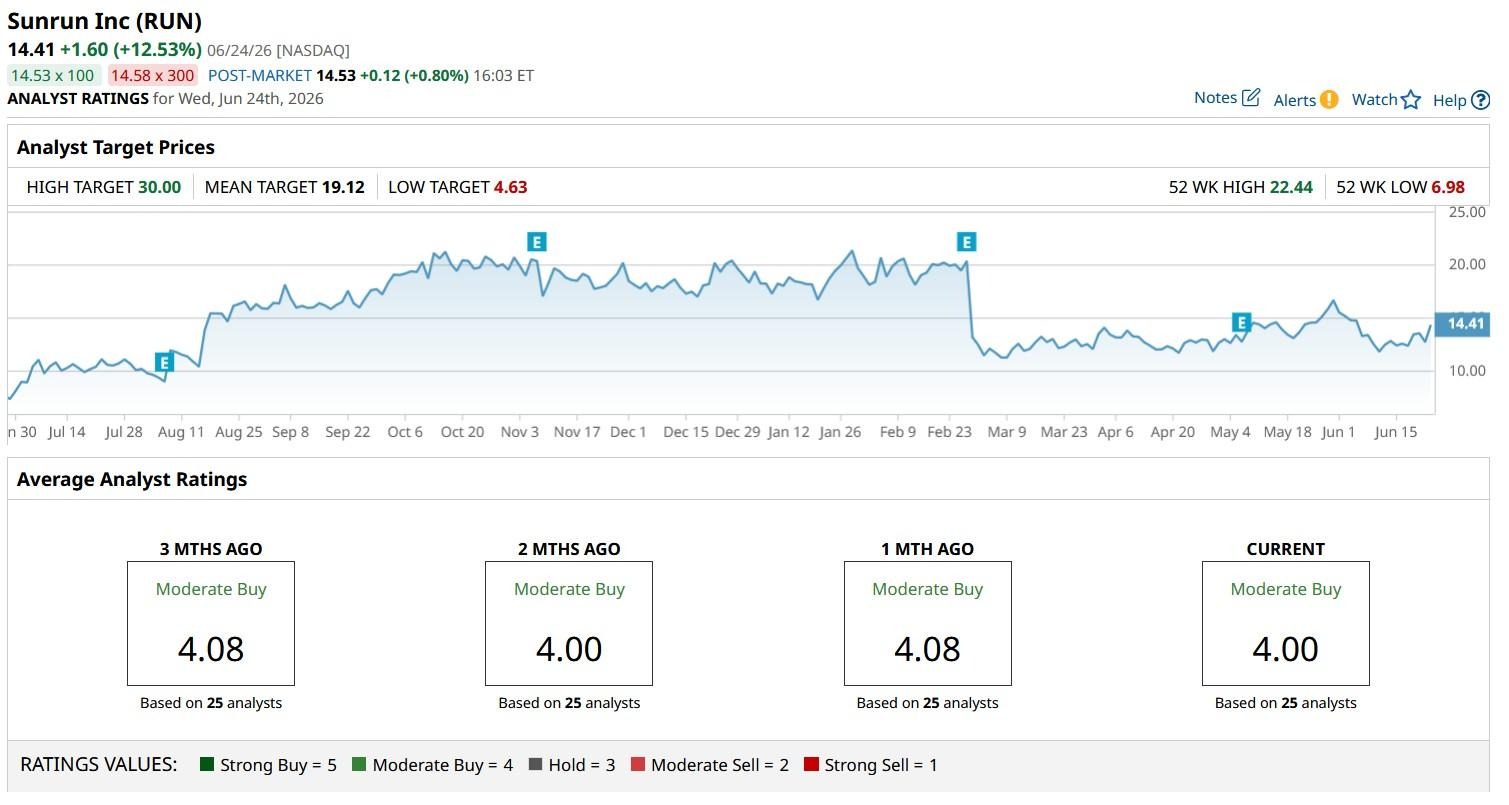

That said, Wall Street continues to rate Sunrun stock at “Moderate Buy,” with the mean price target of $19.12 indicating potential upside of another 32% from here.

The key metric to watch going forward is whether the Virginia capacity deployments, PJM allocations, and any named hyperscaler offtake agreements convert from framework commitments into firm, revenue-generating contracts.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)