/Applied%20Materials%20Inc_%20campus%20sign-by%20Sundry%20Photography%20via%20iStock.jpg)

Wells Fargo has turned more bullish on chip equipment supplier Applied Materials (AMAT) as the AI-led demand for advanced chipmaking continues to gain momentum. Raising the price target to a Street-high of $715 (implying 22% upside from current levels), and maintaining a firm “Overweight” rating means they believe it should outperform the broader market. In a research note, the firm stated that it continues to expect positive semi-cap results.

About Applied Materials Stock

Applied Materials is a global supplier of equipment, software, and services used to make semiconductors, displays, and other advanced electronics. Its tools help chipmakers build, test, and improve the tiny components that power phones, computers, data centers, and many industrial products.

The company works closely with customers across the semiconductor manufacturing process, supporting innovation, efficiency, and scale. With a market capitalization of $508.28 billion, Applied Materials is headquartered in Santa Clara, California.

Investors have rewarded it due to its stronger demand for semiconductor equipment, especially from advanced chipmaking tied to AI and more complex chip architectures. The company has also benefited from broad market confidence in its leadership across deposition, etch, and inspection tools, as well as expectations of continued growth in equipment sales.

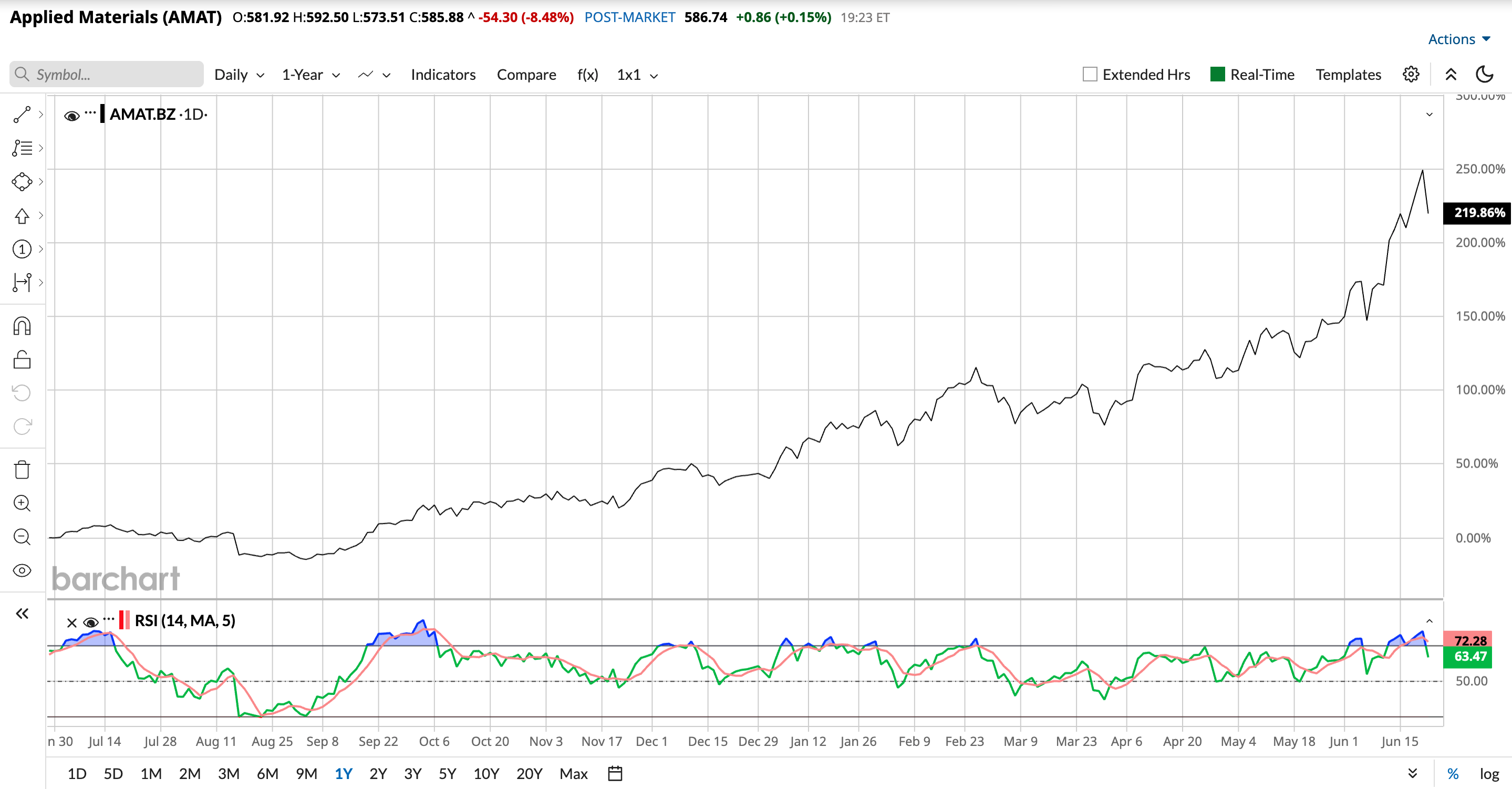

Over the past 52 weeks, AMAT’s stock has gained 240.71%, while it has been up 127.98% year-to-date (YTD). The company’s shares reached a 52-week high of $641.18 on June 22 and are down 8.6% from that level. Over the past month, AMAT has soared 35.57%.

Applied Materials has a 14-day relative strength index (RSI) of 63.44, which sits in healthy territory. On a forward-adjusted basis, its price-to-earnings (non-GAAP) ratio of 52.32 times is stretched compared to the industry average of 23.62 times.

Applied Materials Delivered Strong Q2 on Solid Semiconductor Demand

For the second quarter of fiscal 2026 (quarter ended April 26), Applied Materials reported a record revenue of $7.91 billion, reflecting 11% year-over-year (YOY) growth. Semiconductor systems revenue climbed by 10% YOY to $5.97 billion. Its non-GAAP EPS increased 20% to $2.86.

The quarter was also marked with several EPIC Center engagements with chipmakers and partners, aimed at reducing the time required to commercialize breakthrough technologies. Moreover, with a better inventory position, logistics capacity, and build plan, the company is seeing long-term visibility from its customers.

Applied Materials expects its Q3 FY2026 revenue to be $8.95 billion, +/- $500 million. This figure is above the average analyst estimate of $8.09 billion, while adjusted profit is expected to be $3.36 per share, +/- $0.20, which also exceeds the consensus analyst estimate of $2.88 per share. Given the rapid global AI buildouts, AMAT expects its semiconductor equipment business to grow by more than 30% in CY2026.

Wall Street analysts expect Applied Materials’ EPS to grow by 28.5% YOY to $12.10 for the current fiscal year, followed by a 31.9% expansion to $15.96 in the next fiscal year.

What Do Analysts Think About Applied Materials’ Stock?

In addition to the price target from Wells Fargo, Applied Materials has also received price target raises from other Wall Street analysts. Citi analysts recently raised AMAT’s price target from $550 to $710, citing their bullishness on NAND equipment demand. Citi analysts project total revenue growth of 30% and 22% YOY in CY2027 and CY2028, respectively, with Silicon contributing 35% and 25% growth.

This month, Barclays analysts raised the price target from $500 to $590, while maintaining an “Overweight” rating on the stock. Analyst Tom O’Malley expects wafer fab equipment spending to be better than expected and pointed to growing confidence in the industry's long-term growth outlook. A day earlier, Cantor Fitzgerald analysts raised the price target from $575 to $650, while also maintaining an “Overweight” rating, as analysts believe the semiconductor equipment industry is in the “early innings of a multi-year supply-constrained and durable upcycle.”

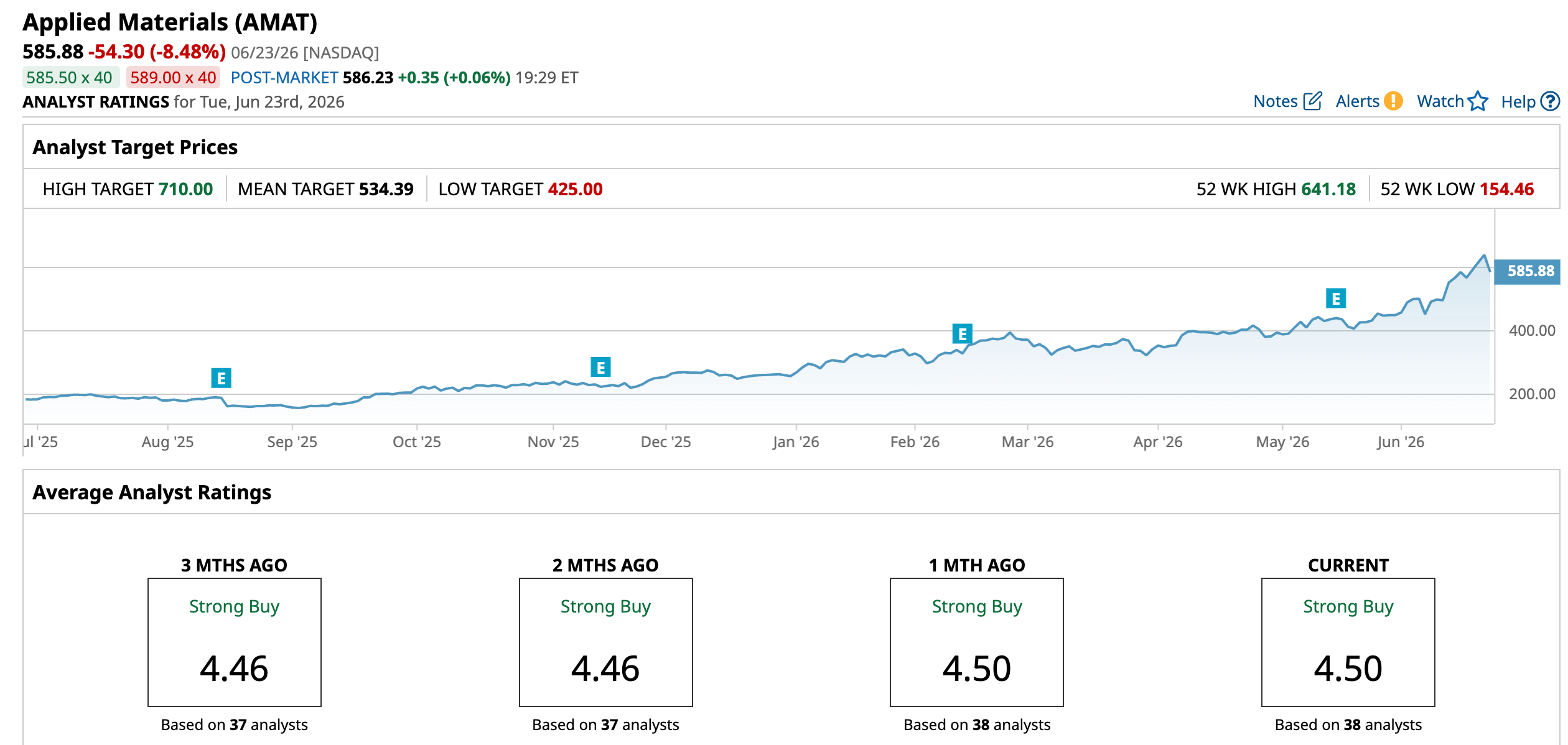

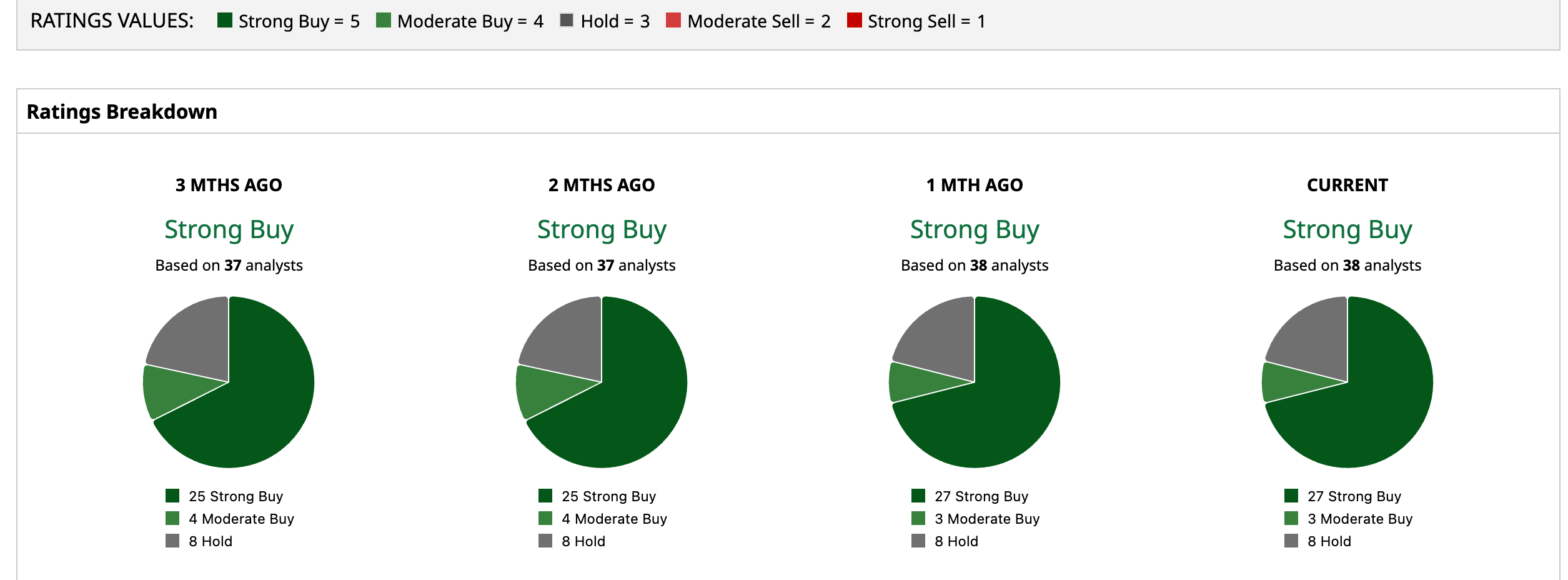

Chip giant Applied Materials is an extremely popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 38 analysts rating the stock, a majority of 27 analysts have given it a “Strong Buy” rating, three analysts rated it “Moderate Buy,” while eight analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $534.39 represents an 8.8% downside from current levels. But, the Street-high target of $710 means AMAT stock can increase 21.2% over the next 12 months.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)