/AI%20(artificial%20intelligence)/Businessman%20touching%20the%20brain%20working%20of%20Artificial%20Intelligence%20(AI)%20Automation%20by%20Suttiphong%20Chandaeng%20via%20Shutterstock.jpg)

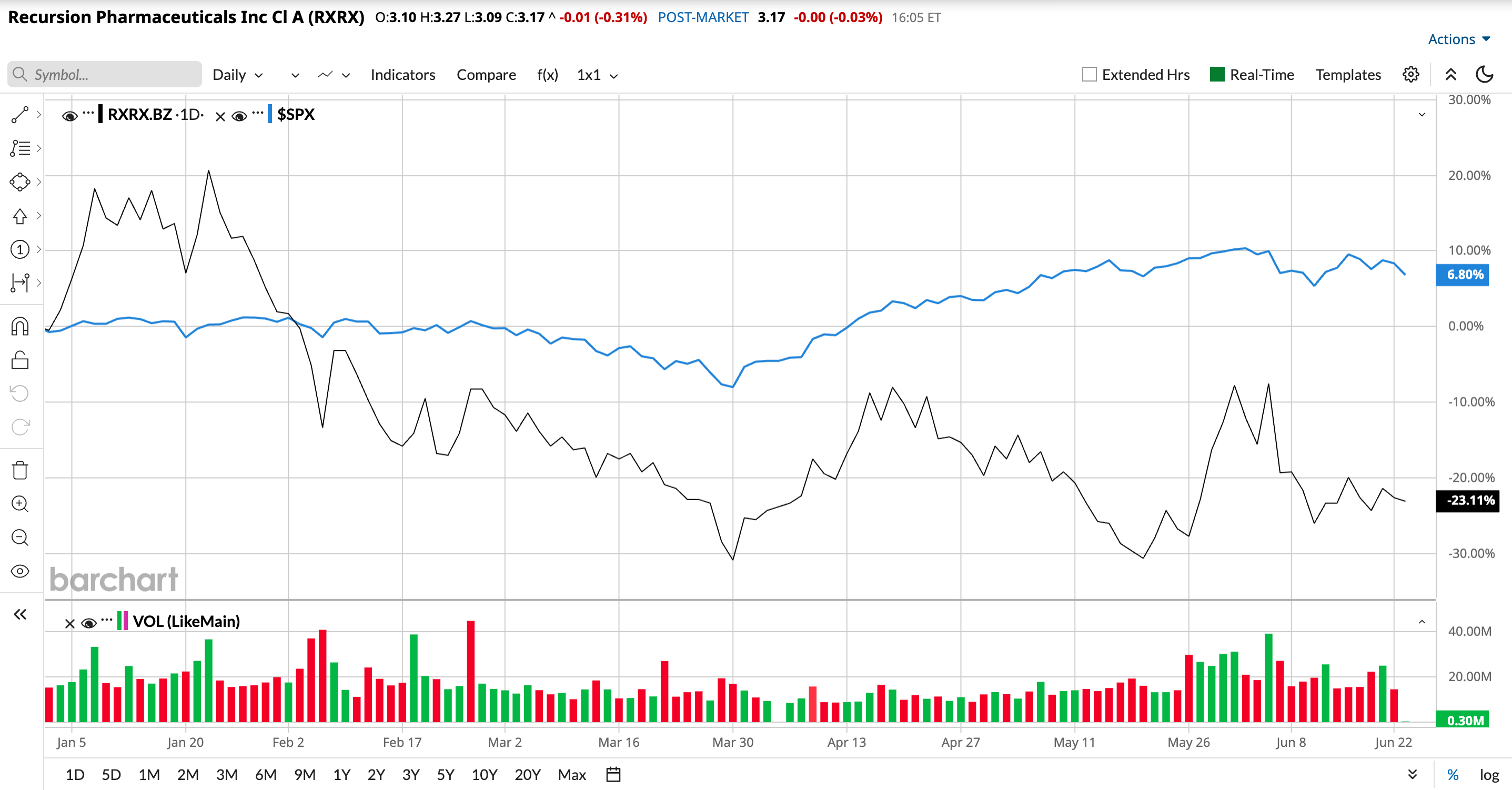

Artificial intelligence (AI) is not only boosting the business for tech companies. Healthcare and biotech industries are also taking full advantage of AI to redesign the ways in which drugs are discovered and developed. One such AI story belongs to a non-tech company, Recursion Pharmaceuticals (RXRX). It is a clinical-stage “TechBio” company that uses AI, automation, and large biological datasets to discover and develop new medicines.

Let’s find out if Recursion is a good AI stock to buy now.

This Is an AI Story Built Around Drug Development

Recursion's platform, known as the Recursion OS, aims to accelerate and improve drug discovery. It is an AI-powered, end-to-end drug discovery and development platform that covers biology, chemistry, and clinical development. The Recursion story is now getting interesting as it begins to reveal pipeline proof rather than just platform ambition. Its first clinical proof of concept has come from REC-4881, an allosteric MEK 1/2 inhibitor targeting familial adenomatous polyposis (FAP).

The company highlighted significant reductions in precancerous polyps and emphasized the durability of the response seen so far. This is important because many FAP patients often face life-altering surgeries, as there are no treatment options available on the market. And without surgery, the risk of cancer increases significantly. Recursion is now working with the U.S. Food and Drug Administration (FDA) to determine the next steps for REC-4881. The company expects to provide updates on this in the second half of 2026.

Recursion’s story doesn’t just rely on this one program. The company’s pipeline now includes five wholly owned programs, with several key milestones expected over the next 12 to 18 months. One among them is REC-1245, an RBM39 degrader currently in Phase 1 for solid tumors and lymphomas. Recursion stated that its AI platform helped it spot RBM39 as an interesting cancer target, which wouldn’t have been possible using traditional drug discovery methods. Recursion then used its platform to design a drug candidate and moved it into human testing about 200 compounds over 18 months. According to management, this is relatively faster than traditional drug discovery. Early trial results have shown positive findings with manageable side effects.

Similarly, REC-4539 is another cancer drug candidate. It targets LSD1, which is already a known cancer target, especially in small-cell lung cancer and AML. However, in this case since the target was already identified, Recursion used AI to design a better version of an LSD1 drug. This program is still very early, and real safety and efficacy data won’t be available until the second half of 2027.

Financial Discipline Is Giving the Story More Credibility

Although the company has no approved products yet, it is maintaining financial discipline by focusing on cost control. In the first quarter, it reduced cash operating expenses by 30% year-over-year (YOY). Recursion ended the quarter with $665 million in cash equivalents, a balance management says should fund operations into early 2028 without the need for additional financing.

Additionally, Recursion expects to spend less than $390 million in cash operating expense for the full year. Furthermore, partnerships with Sanofi -Aventis S.A. ADR (SNY) and Roche Holding (RHHBY) are helping as well. It has delivered ten milestones across its partnerships and has generated more than $500 million in inflows from the partner portfolio.

The Key Takeaway

Recursion is still an unprofitable development-stage business and is not a low-risk stock. However, unlike many companies selling an AI vision, Recursion now has a growing list of proof that AI is turning into a drug-development advantage. If it keeps converting platform claims into clinical and financial proof, the company could eventually have successful products on the market. But that could take a while. Hence, this risky penny biotech stock is suitable for investors with a high risk appetite and a long-term investment horizon.

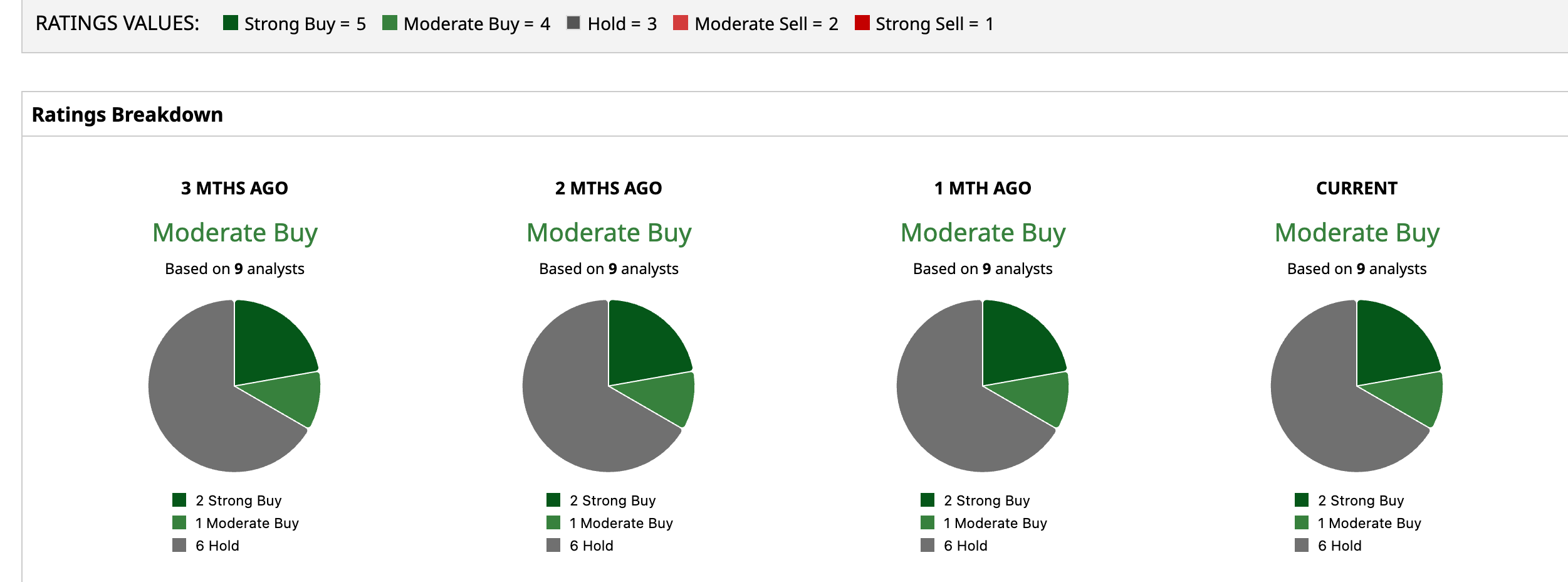

Overall, on Wall Street, analysts rate it an overall "Moderate Buy." Of the nine analysts covering the stock, two rate it a "Strong Buy," one says it is a "Moderate Buy," and six rate it a "Hold." Its average target price of $6.64 indicates 111.47% upside potential. Furthermore, its high target price of $10 implies a potential 218.47% gain over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)