/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

Amazon's (AMZN) stock has struggled to keep pace with the broader market in 2026. While the S&P 500 ($SPX) has advanced more than 7% year-to-date (YTD), Amazon shares have remained largely flat, reflecting growing investor concerns about the company’s aggressive spending plans despite its strong long-term growth narrative.

Amazon’s management has outlined plans to spend roughly $200 billion through 2026, with the majority of this investment directed toward expanding Amazon Web Services (AWS) and building the infrastructure required to support artificial intelligence (AI) workloads. Although the strategy reflects Amazon’s ambition to strengthen its leadership in cloud computing and AI, investors are questioning whether these massive expenditures will generate returns quickly enough to justify the near-term financial burden.

Notably, in the first quarter alone, Amazon reported capital expenditures of $43.2 billion, driven primarily by investments in AWS and generative AI capabilities. Management has also indicated that spending is likely to remain elevated over the coming quarters, suggesting that pressure on margins and free cash flow could persist in the near term.

From Amazon’s perspective, the investment will help the company to capture a larger share of the rapidly growing AI market, strengthen AWS’s competitive advantages, accelerate revenue growth, and generate substantial free cash flow over the long term. However, the market appears less convinced.

With Amazon navigating a $200 billion spending cycle, should you consider investing in AMZN stock? Let's take a closer look at Amazon's growth prospects, valuation, and Wall Street's outlook.

Is AMZN Stock a Buy Now?

Amazon is a compelling investment, supported by multiple high-growth businesses. The company’s strongest catalyst remains AWS, which delivered revenue of $37.6 billion in the latest quarter, marking 28% year-over-year (YoY) growth and an acceleration from the previous quarter. This performance reflects rising demand for both traditional cloud infrastructure and AI workloads.

Notably, within AWS, AI-related revenue is already expanding at a triple-digit pace, highlighting the rapid adoption of Amazon’s AI ecosystem.

The long-term visibility of AWS growth is impressive. The cloud division ended the quarter with a contracted backlog of $364 billion. This number does not include Amazon’s recently announced multibillion-dollar agreement with Anthropic. At the same time, the company is investing heavily in new data centers and plans to double its power capacity by 2027, positioning AWS to capture rising demand for cloud and AI services.

Another emerging growth engine is Amazon’s custom AI chip business. Revenue from its AI silicon division surged nearly 40% sequentially and is now running at an annualized rate of more than $20 billion. Demand for Amazon’s Trainium chips has been exceptionally strong, with major customers such as OpenAI and Anthropic signing long-term commitments. Current-generation chips are largely sold out, while future platforms are attracting reservations well before their commercial launch, indicating sustained demand and growing competitiveness in the AI infrastructure market.

Beyond cloud computing and custom chips, Amazon’s advertising business continues to strengthen. Amazon’s advertising revenue climbed 22% YoY to $17.2 billion in the first quarter. As a high-margin segment, advertising is becoming an increasingly important contributor to profitability. Amazon is also expanding beyond traditional sponsored listings by integrating AI-powered targeting, streaming partnerships, and advanced commerce data, creating new monetization opportunities.

Overall, AWS, AI infrastructure, custom chips, and digital advertising provide Amazon with multiple growth drivers. With demand trends accelerating across these businesses, the company appears well-positioned to deliver sustained revenue and earnings growth over the long term, making the stock an attractive investment.

Amazon’s Valuation Appears Reasonable

Amazon’s recent pullback from its highs has made the stock’s valuation attractive for long-term investors. At current levels, AMZN stock trades at a forward price-to-earnings (P/E) ratio of 31.7, a multiple that appears reasonable relative to its earnings growth outlook. Analysts project AMZN’s earnings per share (EPS) growth of roughly 30% in 2027.

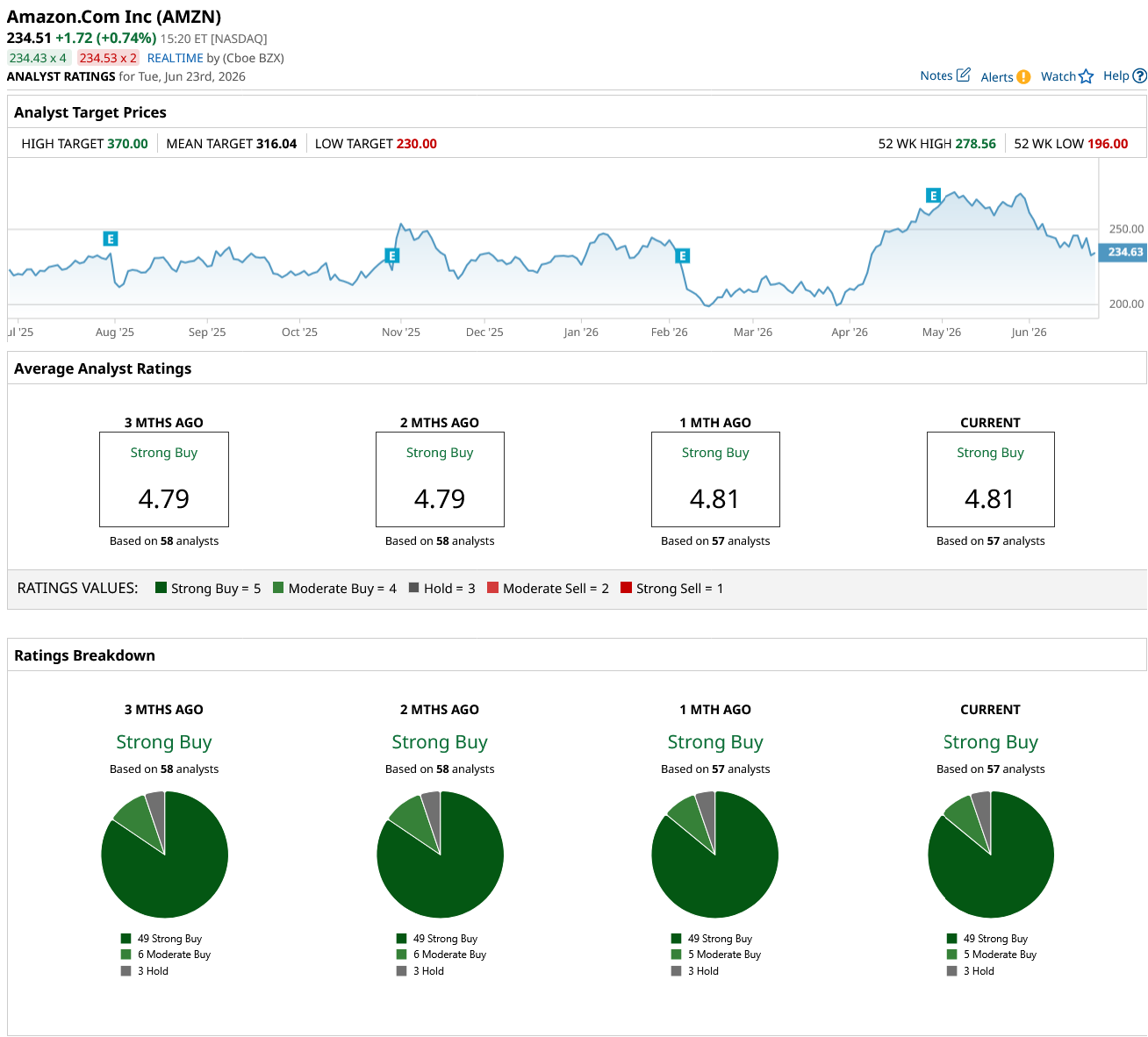

Analysts maintain a bullish stance on Amazon and assign a “Strong Buy” consensus rating on the stock.

The Bottom Line

Despite investor concerns about its massive $200 billion investment cycle, Amazon remains well-positioned to capitalize on long-term growth opportunities in cloud computing, AI, and digital advertising. While elevated capital expenditures may weigh on margins and free cash flow in the near term, the company’s strong AWS momentum, expanding AI ecosystem, and high-margin advertising business provide compelling growth catalysts.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)