/A%20close-up%20of%20the%20Adyen%20sign%20on%20an%20office%20building%20by%20StockMarketVisuals%20via%20Adobe%20Stock.jpeg)

Adyen N.V. (ADYEY) gave investors a fresh reason to pay attention after it unveiled Adyen Agentic, a suite of modular APIs built to help merchants sell through conversational AI platforms without rebuilding their commerce systems. Shares jumped 4.11% on Monday after the news and the move made sense because the release pushes Adyen deeper into the next phase of digital commerce, not just plain old payments.

That matters because Adyen is not trying to be just a payment processor. It wants to sit closer to the whole transaction, from discovery to checkout to money movement, and that is exactly where the company is spending time and money in 2026.

For long-term investors, that makes the stock interesting. For bargain hunters, it still looks expensive enough to make them squint.

A Chart That Still Needs Work

The stock’s bigger picture is messier than the headline pop suggests. Adyen is still down 37.32% year-to-date (YTD).

That weakness gives the new AI story more punch, because investors clearly want a reason to believe the business can reaccelerate. The problem is that Adyen already had a good business before the AI launch. The real question is whether this turns into a durable growth driver or just another nice product release in a stock that still has work to do on the chart.

Valuation is where the story gets tricky. Adyen trades at 26.17 times trailing earnings and 21.84 times forward earnings, which is below the software-infrastructure industry’s weighted average price-to-earnings of 32.93, but the stock still sells for 11.66 times revenue. That is not screaming cheap. It is a premium valuation for a premium operator, and that usually leaves less room for disappointment.

So the bull case is not about finding a bargain. It is about paying up for a company that keeps building a bigger platform. If Adyen can keep layering new products on top of its payments stack, the multiple may be easier to justify. If growth slips, the stock could stay stuck in the penalty box.

The Latest Quarter Still Looked Solid

Adyen’s latest quarterly update, for the first quarter of 2026, showed net revenue of $719.94 million, up 16% year-over-year (YOY), or 20% on a constant-currency basis. Processed volume climbed 21% to about $443.01 billion, while digital revenue reached about $405.43 million, unified commerce came in at about $227.53 million and platforms revenue rose to about $86.98 million. CFO Ethan Tandowsky said the quarter reflected “continued broad-based performance” across the customer base.

Adyen’s update did not use adjusted EPS the way some U.S. companies do. Instead, the company kept the focus on revenue and EBITDA. Its full-year 2025 report showed free cash flow conversion of 87% and capex at 5% of net revenue, while stock-analysis data puts cash at about $14.73 billion and debt at about $343.42 million. On a trailing basis, it reported about $1.23 billion in net income and EPS of 33.61.

What Adyen Is Doing Elsewhere In 2026

The AI launch is only one piece of the story. In 2026, Adyen also launched Personalize for real-time checkout optimization, rolled out Intelligent Money Movement, agreed to buy Talon.

One for about $868.98 million, teamed up with SAP on native payment infrastructure, and later struck a deal to acquire Orb for about $387.63 million. It also joined the x402 Foundation and the Agentic AI Foundation, which tells you management wants to shape the standards around this new commerce wave, not just follow it.

What Wall Street Thinks of Adyen Stock

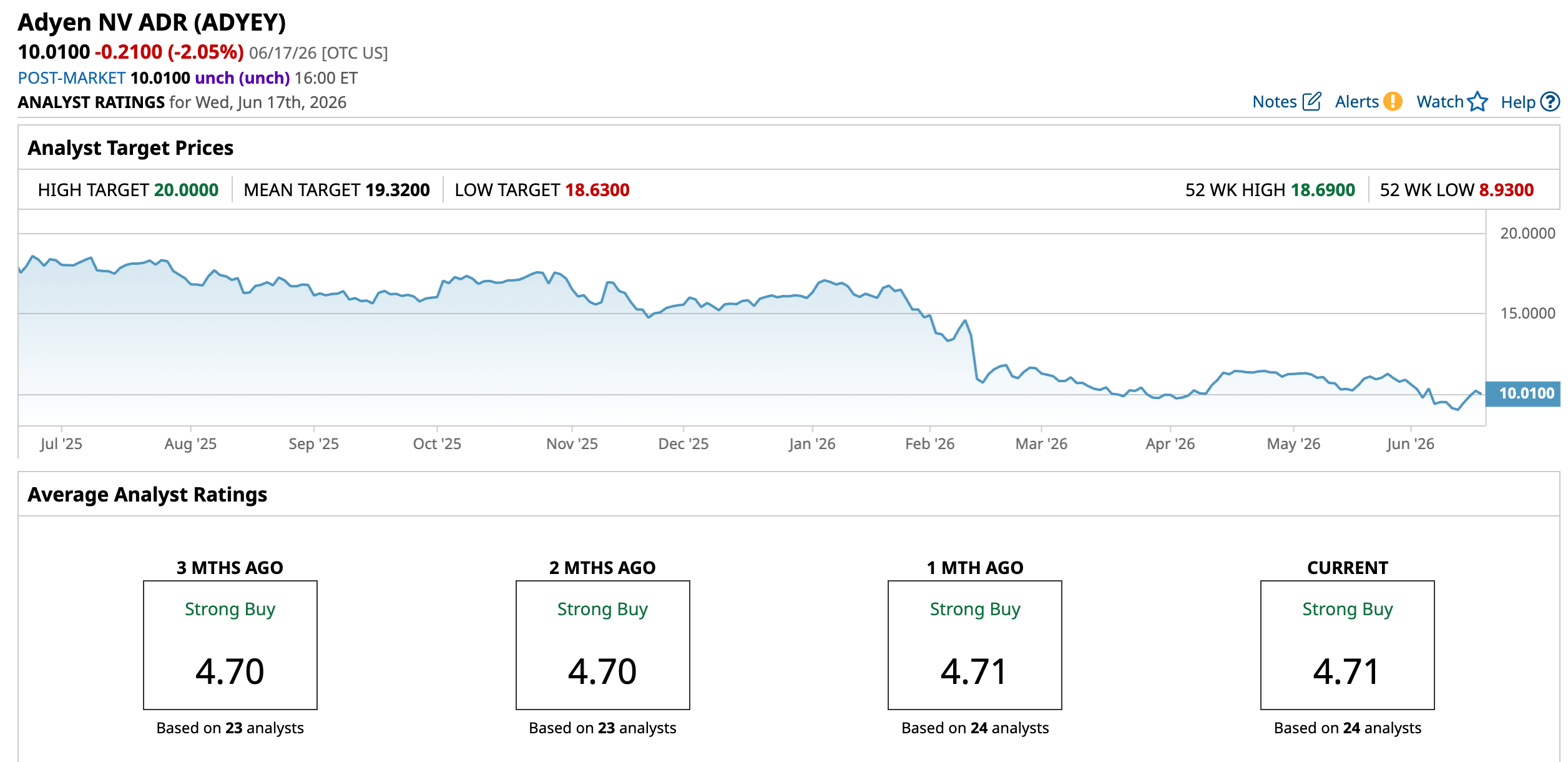

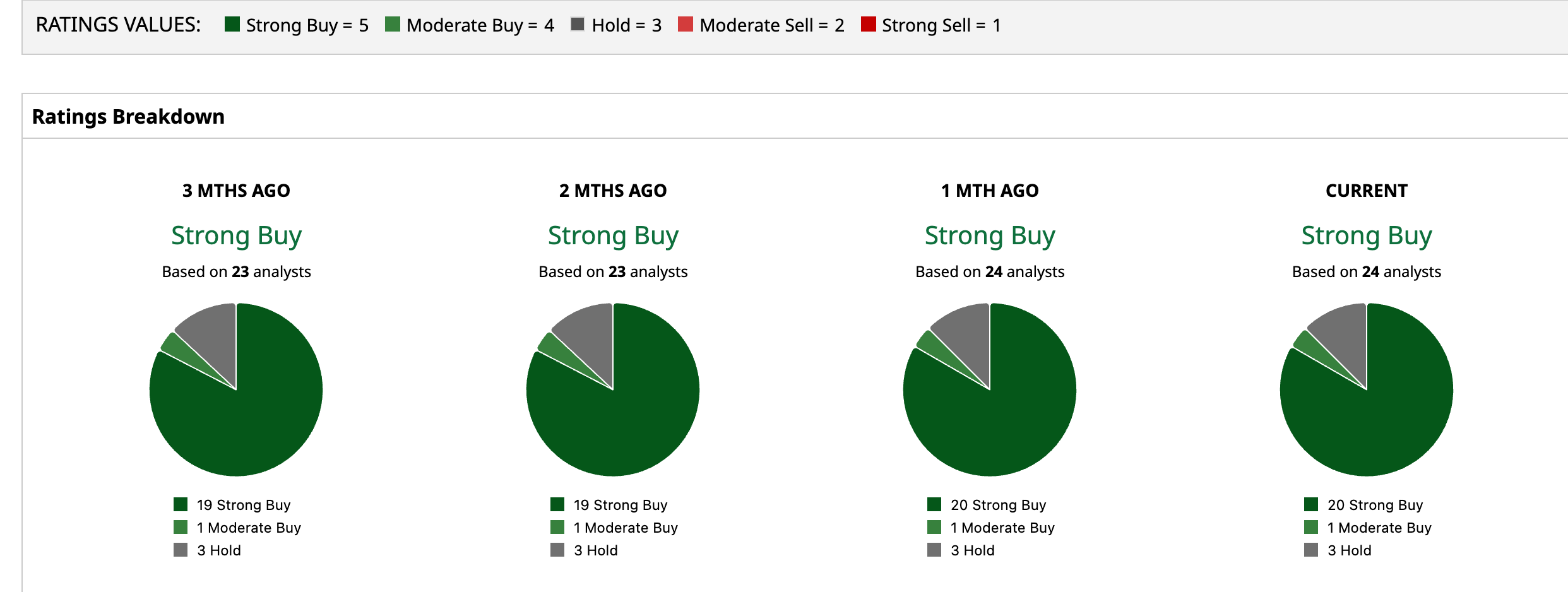

Wall Street is still leaning bullish towards ADYE Stock. Morgan Stanley said Adyen looked like a “highly attractive entry point” and argued AI-disruption worries were not very relevant to the company’s business model.

Similarly, Goldman Sachs raised its target to €2,200 and kept a “Conviction Buy” rating, while TD Cowen and Jefferies stayed constructive with targets of €1,175 and €1,166. BNP Paribas Exane is more cautious, with a “Hold” and an €890 target.

Overall, the consensus remains “Strong Buy,” with an average target of $19.32 implying 93% upside from the latest close.

Adyen looks like a “Buy” for investors who can handle a premium valuation and want exposure to a best-in-class payments platform pushing into agentic AI. It is not cheap, but the business keeps giving bulls reasons to stay interested.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)