Chesterfield, Missouri-based Bunge Global SA (BG) operates as an agribusiness and food company that produces and supplies plant-based oils, fats, and protein. Valued at $23.7 billion by market cap, the company’s products are used in a wide range of applications, such as animal feed, cooking oils and flours, as well as bakery and confectionery, dairy fat alternatives, plant-based meat, and infant nutrition.

Shares of this global agribusiness and food company have outperformed the broader market considerably over the past year. BG has gained 75.6% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 11.8%. In 2026, BG stock is up 37.6%, surpassing the SPX’s marginal fall on a YTD basis.

Zooming in further, BG has also outpaced the VanEck Agribusiness ETF (MOO). The exchange-traded fund has gained about 26.8% over the past year. Moreover, BG’s returns on a YTD basis outshines the ETF’s 17.2% gains over the same time frame.

Bunge Global's performance was driven by the successful integration of Viterra, expanding origination and processing capabilities, especially in softseed and soybeans. Early synergy realization and higher processing volumes in South America offset margin pressures in North America.

On Feb. 4, BG shares closed up marginally after reporting its Q4 results. Its adjusted EPS of $1.99 surpassed Wall Street expectations of $1.82. The company’s revenue was $23.8 billion in the period. BG expects full-year adjusted EPS in the range of $7.50 to $8.

For fiscal 2026, ending in December, analysts expect BG’s EPS to grow 7% to $8.10 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

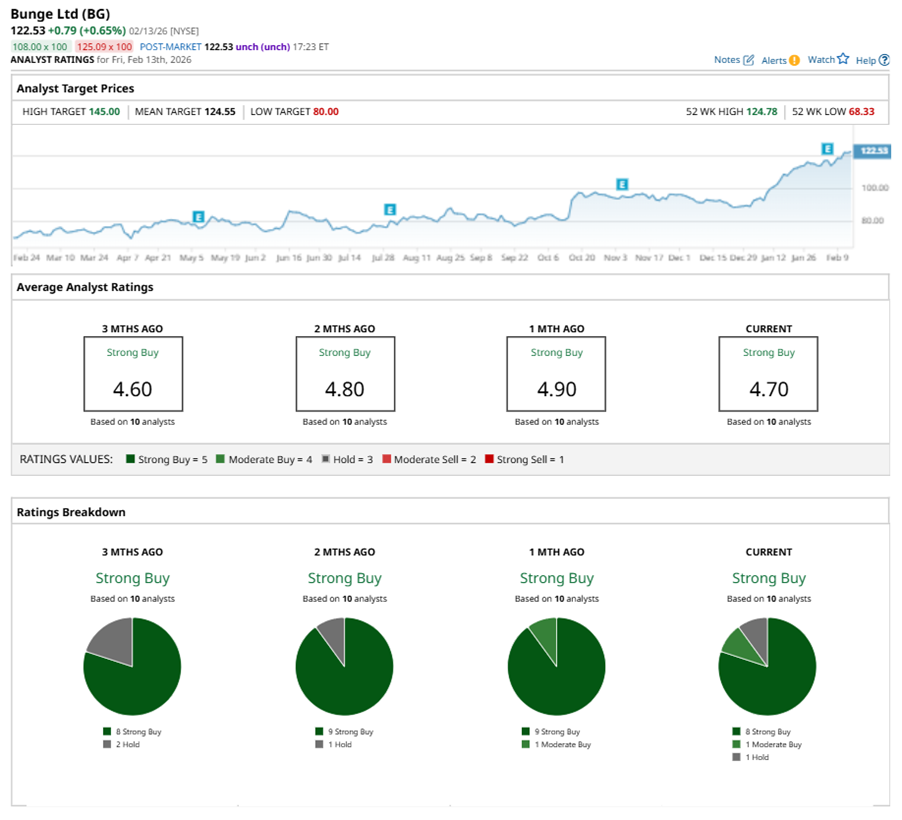

Among the 10 analysts covering BG stock, the consensus is a “Strong Buy.” That’s based on eight “Strong Buy” ratings, one “Moderate Buy,” and one “Hold.”

This configuration is slightly less bullish than a month ago, with nine analysts suggesting a “Strong Buy.”

On Feb. 5, Morgan Stanley (MS) analyst Steven Haynes maintained a “Buy” rating on BG and set a price target of $130, implying a potential upside of 6.1% from current levels.

The mean price target of $124.55 represents a 1.6% premium to BG’s current price levels. The Street-high price target of $145 suggests an upside potential of 18.3%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)