/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)

Shares of satellite communications company AST SpaceMobile (ASTS) ended sharply higher in yesterday's trading session following the successful orbital launch of its three satellites—Bluebird 8, 9, and 10. Further, Bluebirds 11, 12, and 13 are also set for launch soon, with Bluebird 37 in production too.

The timing could not have been better, as the excitement around space companies is at its highest among the investing public, thanks to the SpaceX IPO last week. In fact, SpaceX's Falcon 9 carried the satellites for deployment in low-earth orbit, continuing a long-standing relationship between the two companies.

About AST SpaceMobile

Founded in 2017, AST SpaceMobile is a satellite communications company whose goal is to build the first space-based cellular broadband network that connects directly to ordinary smartphones, eliminating the need for specialized satellite phones or external terminals. The company reports relationships with nearly 60 mobile network operators covering more than 3 billion subscribers globally.

Valued at a market cap of $31.9 billion, ASTS stock is up 10% on a year-to-date (YTD) basis. Although the stock is down about 7% in morning trading today.

Thus, with more satellites deployed, can ASTS finally break free? Let's find out.

No Space for Profits Yet

AST is seeking to revolutionize the telecom sector. However, that comes at a price, and the company is paying it in the form of widening losses. Out of the past eight quarters, AST's losses have increased on a year-over-year (YoY) basis on five occasions.

Q1 2026 was no different as losses came in more than three times higher than the prior year at $0.66 per share. Moreover, it came in higher than the consensus estimate of a loss of $0.26 per share.

However, in a positive development, revenues jumped to $14.7 million in the quarter from a mere $718,000 in the previous year, although this was lower than Street expectations by more than $20 million. Still, the company said that it remained on track to achieve its revenue guidance of $150 to $200 million for 2026 on the back of its existing backlog.

Net cash used in operating activities continues to rise as the company's investments in engineering and R&D are taking a toll on cash generation. The same came in at $48.1 million, up from $28.5 million in the year-ago period. Overall, AST SpaceMobile closed the quarter with a cash balance of $3 billion, much higher than its short-term debt levels of $37.1 million, reflecting less liquidity pressure.

Considering all this, its current valuations are just not sustainable, especially when it is not churning out any profits, not even at the operating level. Its forward EV/Sales and P/S are at 147.79 and 144.59 compared to the sector medians of 1.83 and 1.20, respectively.

Case for Making (And Not Making) an Investment in ASTS

To achieve what ASTS is set out to achieve, its primary tool is the BlueBird satellites, the largest commercial satellites in orbit. Notably, ASTS holds regulatory approval to deploy up to 243 satellites and is seeking to raise that limit further to 543. The company aims to place approximately 45 BlueBird satellites into orbit by the end of 2026. In addition, it has expanded its manufacturing footprint to more than 500,000 square feet and is targeting a steady production rate of six fully assembled satellites per month.

Encouragingly, the company maintains strong control over most of its supply chain through in-house manufacturing capabilities. This includes full ownership of the key processes and specialized composite materials essential for building its satellites. The firm also oversees its own chip design operations. These manufacturing strengths could prove far more challenging for competitors to replicate.

Against competitors, BlueBird is strongest on direct-to-smartphone capability and antenna scale, while rivals usually win on maturity, scale, or cost efficiency. Starlink is the biggest pressure point because it already has a much larger constellation and broader launch cadence, but AST’s value proposition is different since its satellites are designed for normal smartphones used by the common public rather than requiring dedicated terminals. Viasat and Iridium compete in satellite communications, too, yet they do not match AST’s direct-to-handset broadband thesis in the same way.

However, BlueBird is expensive and technically complex because of its massive phased arrays and proprietary chip, but that same design gives it stronger coverage per satellite and higher data throughput than older satellite architectures. So BlueBird is not the cheapest option in space connectivity, but it is one of the most ambitious in terms of user simplicity, spectrum efficiency, and the ability to make satellite access feel native to a normal phone.

In terms of revenue opportunity, defense is expected to become a major revenue contributor for the company going forward. ASTS has recently initiated testing for non-commercial initiatives with the Space Development Agency, focused on advancing radiolocation technologies. In a recent update, management indicated that it is actively pursuing ten distinct use cases for the United States government, spanning both communications and non-communications applications. The company suggested that roughly half of its anticipated 2027 revenue could already stem from government sources. With the overall opportunity for 2027 estimated at $1 billion, this points to potential revenue of approximately $500 million from the U.S. government alone next year.

That said, the unsuccessful delivery of the seventh satellite into its intended orbit by Blue Origin triggered notable concern among shareholders. This development has raised questions about the company's capacity to deploy the required number of satellites on schedule to meet its aggressive timeline targets.

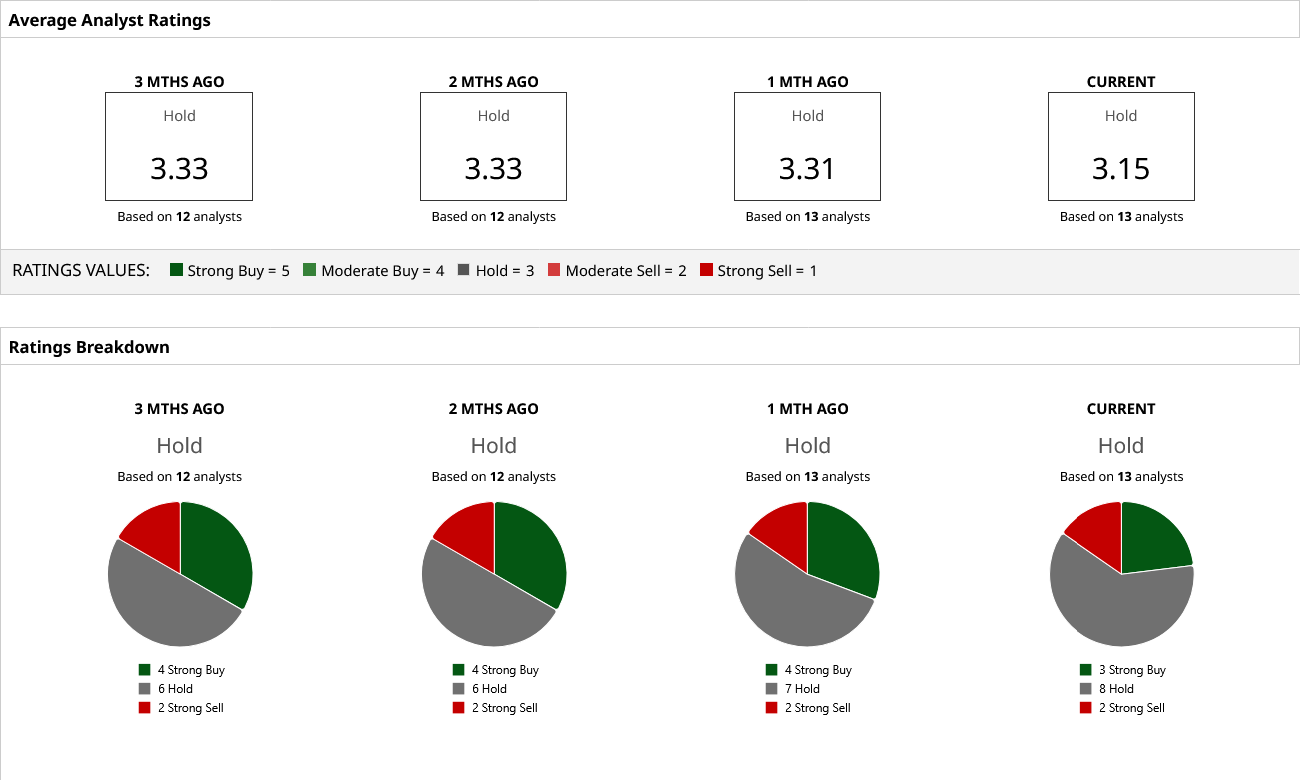

Analyst Opinion on ASTS Stock

Taking all of this into account, analysts have deemed ASTS stock to be a “Hold” with a mean target price of $84.82, which it has just dipped below recently. The high target price of $115 indicates an upside potential of about 44% from current levels. Out of 13 analysts covering the stock, three have a “Strong Buy” rating, eight have a “Hold” rating, and two have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)