Intel (INTC) stock continues to soar higher, reflecting improving fundamentals of the foundry business and solid artificial intelligence (AI)-driven demand. Its shares have climbed roughly 191% over the past three months and 510% over the past year, as the market remains optimistic about the company's turnaround strategy and its growing role in the AI boom.

The latest catalyst came after President Donald Trump stated on Truth Social that Apple (AAPL) had agreed to work with Intel to design and manufacture chips in the U.S. While investors await additional details, the announcement sent Intel shares sharply higher in early morning trading and strengthened optimism about the trajectory of the company's foundry business.

Notably, an Apple-Intel partnership would represent a major milestone for Intel Foundry and signal increasing confidence in the company's manufacturing capabilities. Intel has spent the past several years investing heavily to transform itself into a leading contract chip manufacturer capable of serving both internal and external customers.

Intel's Foundry Business Is Gaining Momentum

Intel's foundry strategy is becoming increasingly important as demand for advanced semiconductor manufacturing accelerates and supply remains constrained. The rapid buildout of AI infrastructure across the technology industry has created a massive opportunity for companies capable of producing cutting-edge chips at scale.

Intel’s recent partnerships have further strengthened investor confidence. Intel has highlighted collaborations involving major technology companies, including Nvidia (NVDA) and Elon Musk's Terafab initiative. These relationships show Intel's efforts to position itself at the center of the next generation of AI and data-center infrastructure.

The financial results also suggest that progress is being made. Intel Foundry generated $5.4 billion in revenue during the first quarter, representing a 20% sequential increase driven by higher Extreme Ultraviolet (EUV) wafer production. External foundry revenue reached $174 million during the quarter.

While the segment remains unprofitable, losses moderated compared with previous periods, and management expects operating performance to improve further in the coming quarters.

Why INTC Stock Could Reach $150

Intel's comeback story is gaining momentum. After spending years losing ground to competitors, Intel is beginning to show signs that its ambitious turnaround strategy may be working. Intel is pursuing a two-pronged strategy, including expansion in AI and the development of a global contract manufacturing business that could reshape its long-term growth profile.

A key pillar of the bullish case for Intel is its foundry expansion. Intel has been investing heavily in manufacturing capacity and in attracting external customers. If successful, this business could diversify Intel’s revenue beyond its own chip products and create a long-term growth engine similar to the model used by leading semiconductor foundries.

AI is emerging as another important catalyst. AI-related businesses now account for nearly 60% of Intel’s total revenue, highlighting the company’s growing exposure to one of the fastest-growing areas of technology.

In the first quarter, revenue from AI-focused operations increased 40% year-over-year (YoY). Much of that growth came from Intel’s Data Center and AI (DCAI) division, which generated $5.1 billion in revenue, up 22% YoY. Rising demand from enterprises investing in AI-capable computing infrastructure helped drive these results.

As the AI market evolves beyond model training toward inference workloads and autonomous AI agents, demand for server CPUs is expected to remain robust, supporting continued growth. Intel also reported strong demand for custom AI chips, with revenue from application-specific integrated circuits nearly doubling YoY.

Importantly, the AI opportunity is evolving. While much of the recent excitement has focused on training large language models (LLMs), the inference workloads are expected to become an even larger market over time. As AI agents and enterprise AI deployments expand, demand for server processors could remain strong for years.

Intel is also seeing increasing demand for custom AI chips. Revenue from its application-specific integrated circuits (ASICs) business nearly doubled from the previous year, reflecting growing customer demand for specialized AI solutions.

Execution Improving but Risks Remain

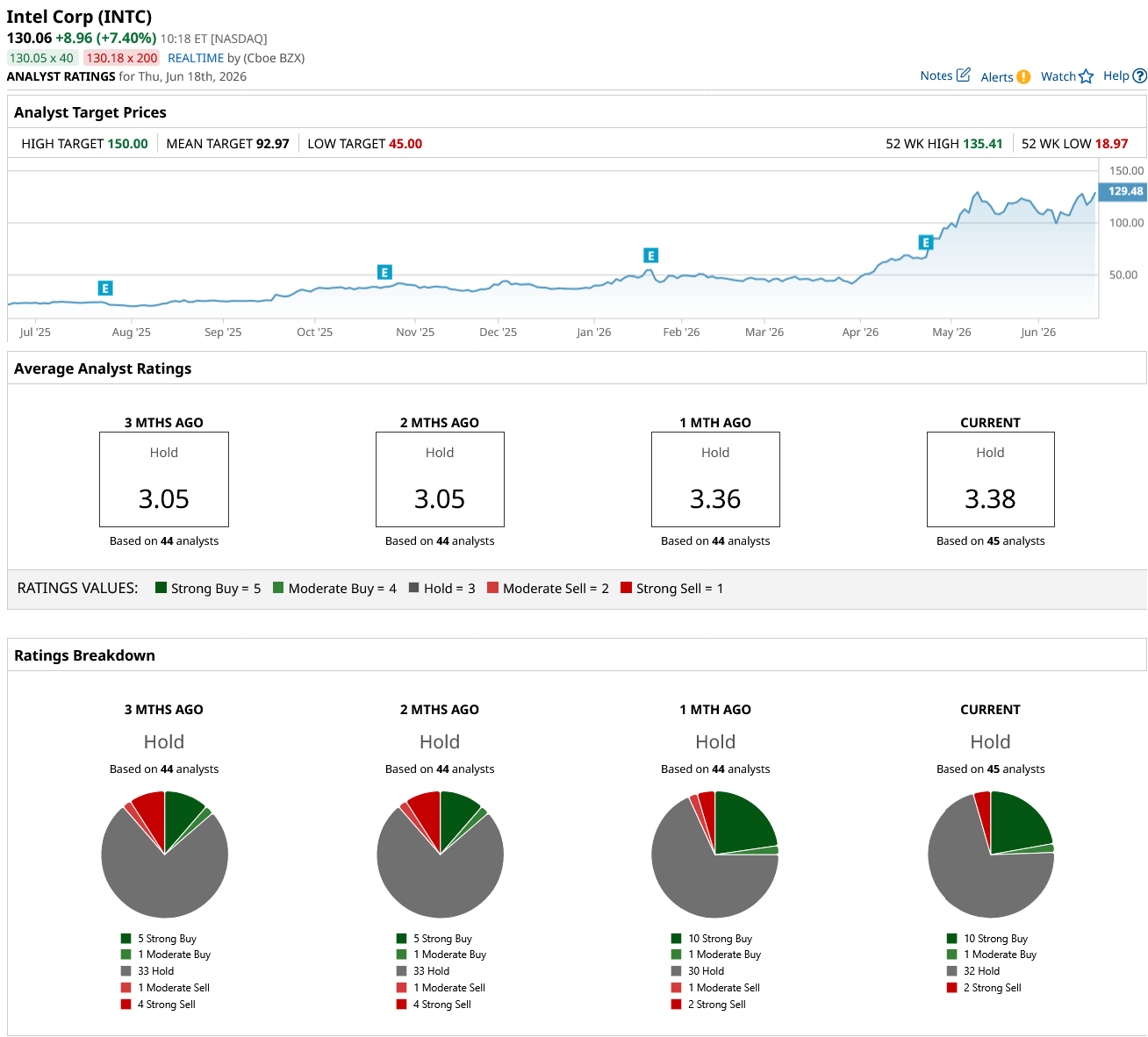

Overall, Intel’s improving execution, expanding foundry ambitions, and growing presence in AI provide a credible path for future growth. At least one analyst expects these catalysts to drive Intel’s stock price to $150 (the Street’s highest price target), representing about 15% upside from its recent price, as of this writing, of about $130.

However, risks remain. Intel shares have already risen significantly, meaning much of the optimism may already be reflected in the valuation. To justify additional upside, the company must continue executing well, win more foundry customers, and prove its AI initiatives can deliver sustainable growth. For now, most analysts maintain a “Hold” rating on the stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)