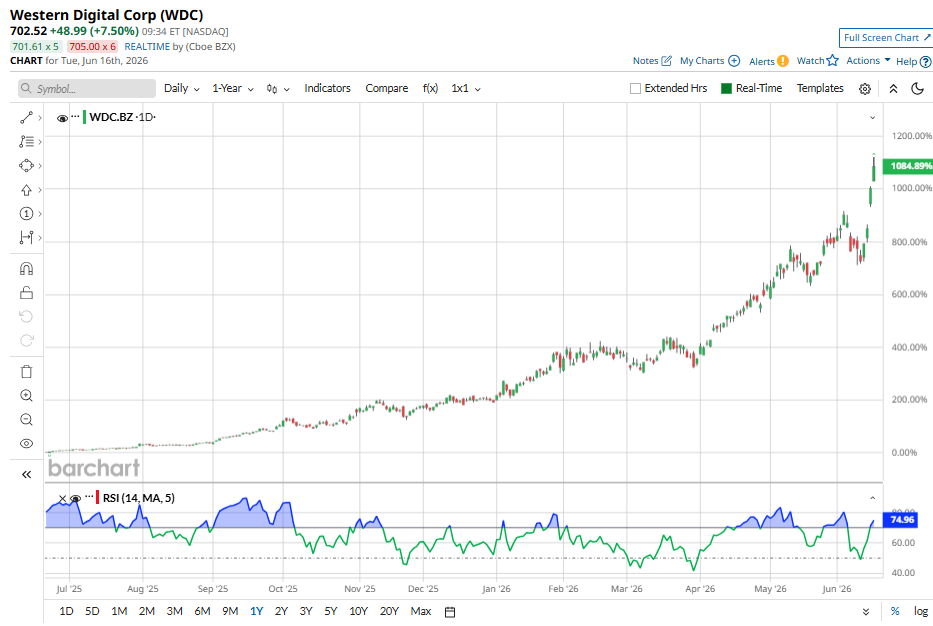

Western Digital (WDC) stock has delivered eye-popping returns for investors. Shares of the data storage company have surged more than 1,115% over the past year, thanks to booming artificial intelligence (AI) demand for high-performance storage and a favorable pricing environment.

The latest boost came after Morgan Stanley raised its price target on WDC stock to $650 from $488, citing robust demand for hard disk drives (HDDs) and continued pricing strength across the storage market. But after such an extraordinary rally, the key question is whether Western Digital stock still has room to run.

One factor supporting ongoing optimism is the accelerating buildout of AI infrastructure. As enterprises increasingly deploy AI-driven applications and leading cloud providers continue to invest in large-scale data centers, data creation and storage demand are rising at record levels. This environment positions Western Digital's high-capacity nearline HDDs to capitalize on the growing need for efficient, large-scale storage.

The rise of agentic AI could serve as another growth catalyst by driving additional demand for data storage. This emerging technology is expected to generate and process even larger amounts of information, extending the growth runway for storage providers such as Western Digital.

The company is also benefiting from tight supply conditions, which have supported pricing and allowed manufacturers to generate stronger margins. This trend will sustain in the coming quarters, indicating that Western Digital could continue to deliver strong earnings growth, which will support its ongoing share price rally.

Western Digital's Profit Could Continue to Soar Higher

Western Digital has witnessed strong earnings growth in recent quarters, and its profit could continue to surge, driven by sustainable demand and higher pricing.

In the company's fiscal third quarter, adjusted EPS jumped 97% year-over-year (YOY) to $2.72. As for fiscal Q4, Western Digital projects revenue of approximately $3.65 billion, representing about 40% YOY growth. Gross margin is also expected to reach 51% to 52%, a substantial improvement from 41.3% in the same period last year.

Profit growth could once again remain solid. Management expects quarterly earnings of approximately $3.25 per share in Q4, above the current analyst consensus estimate of $3.22. Moreover, this projection reflects a sharp increase from earnings of $1.66 per share in the prior-year quarter.

Wall Street also sees significant upside in Western Digital’s earnings in fiscal 2026 and beyond. Consensus estimates call for EPS of $9.60 in fiscal 2026, representing nearly 112% growth. From there, analysts forecast earnings to climb another 83% in fiscal 2027 to $17.61 per share. Given the strong demand and pricing conditions, those projections could prove conservative.

Supporting Western Digital's growth is its expanding portfolio of higher-capacity storage products. The company continues to ramp advanced ePMR technology while preparing for broader deployment of heat-assisted magnetic recording (HAMR) drives and driving UltraSMR adoption. These products are expected to further boost its margins and drive earnings.

Overall, durable demand, higher pricing, long-term agreements, and debt reduction position Western Digital to deliver solid earnings.

The Valuation Suggests Further Upside

Even though WDC stock has surged significantly in recent months, its valuation remains reasonable and suggests further upside ahead. Western Digital stock currently trades at 68 times forward earnings. That may seem high, but its solid earnings growth trajectory indicates that a premium valuation is warranted.

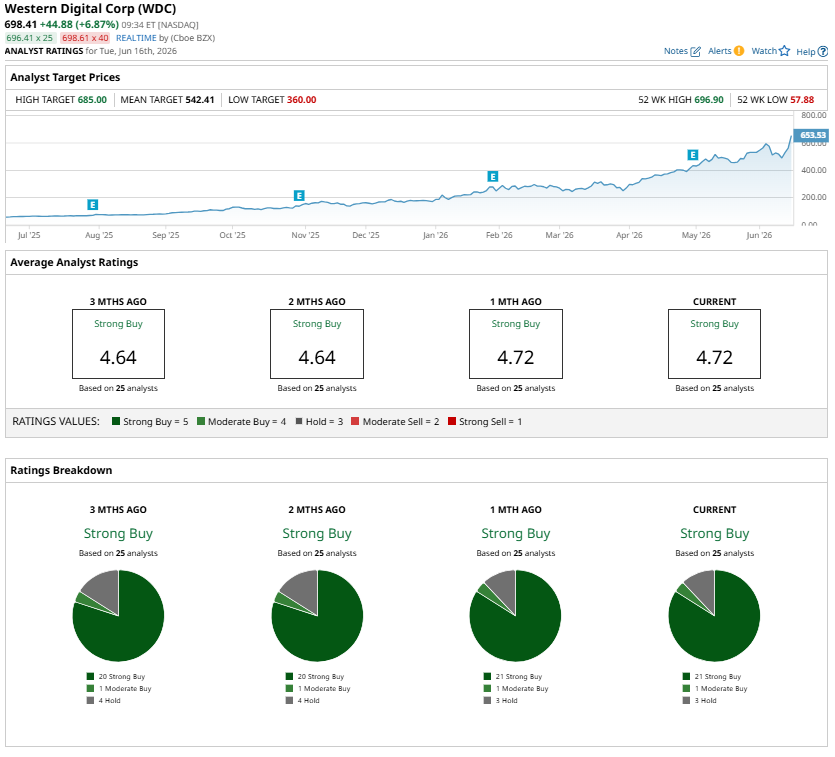

Wall Street’s sentiment toward WDC stock remains bullish, with 25 analysts assigning a “Strong Buy” consensus rating. Although the stock has already surpassed the highest price target of $685, analysts are expected to raise their forecasts further as the company continues to deliver strong financial results and earnings momentum.

Overall, Western Digital’s strong earnings momentum and reasonable valuation indicate that the rally in shares will likely sustain.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)