/Best%20Buy%20Co_%20Inc_%20store%20by-%20Michael%20Vi%20via%20iStock.jpg)

Best Buy Co., Inc. (BBY) has long been one of the biggest names in consumer electronics retail. Headquartered in Richfield, Minnesota, the company sells everything from laptops and smartphones to home appliances and smart-home gadgets through its nationwide store network and growing online platform. Its well-known Geek Squad service business adds another layer to the customer experience, helping shoppers with installation, repairs, and technical support. Today, Best Buy carries a market capitalization of about $15.9 billion.

That valuation firmly places Best Buy in the “large-cap” category, a label typically reserved for companies worth $10 billion or more. Its scale reflects decades of brand-building, strong customer loyalty, and a broad product lineup that keeps consumers coming back for their technology needs. Those advantages have helped Best Buy maintain a meaningful position in a highly competitive retail landscape.

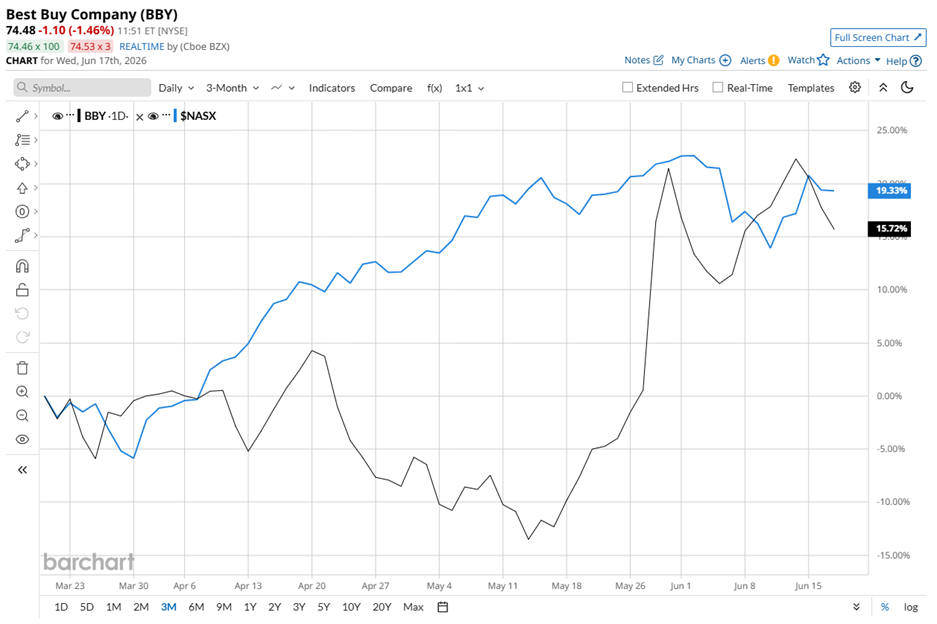

BBY stock is currently down 12.4% below its 52-week high of $84.99 reached in October 2025. However, the stock has found its footing in recent months, rallying 18.9% over the past three months and outperforming the Nasdaq Composite’s ($NASX) 17.1% surge during the same period.

While Best Buy has lagged the broader market, the stock has still managed to post respectable gains. Shares are up 11.2% on a year-to-date basis and 7.3% over the past 52 weeks. By comparison, the Nasdaq Composite has delivered stronger returns, gaining 13.3% this year and 34.9% over the past year.

Even so, BBY has shown signs of resilience, with the stock currently trading above both its 50-day and 200-day moving averages – a technical signal that suggests momentum remains tilted in the bulls’ favor.

Best Buy’s gains in 2026 may not have matched the broader market, but the stock has still given investors plenty of reasons to stay interested. The turning point came when the electronics retailer delivered a stronger-than-expected fiscal Q1 report, easing concerns that consumer spending was slowing too sharply. Revenue reached $8.94 billion, while earnings of $1.28 per share topped Wall Street estimates. BBY stock gained nearly 16% after the report.

More importantly, comparable sales rose 2%, beating guidance and marking a notable shift after nearly two years of declining store sales. That result suggested shoppers were finally returning for more than just necessities.

The company is also benefiting from a fresh technology upgrade cycle. Demand for AI-powered laptops, next-generation PCs, gaming hardware, and new devices like the Nintendo Switch 2 has helped drive store traffic and online sales. As consumers look to upgrade their tech setups, Best Buy is increasingly becoming a key stop in that trend.

Adding in renewed confidence from Wall Street, investors are starting to view Best Buy as a retailer that may be turning the corner after a challenging stretch.

Even against its closest peers, Best Buy has managed to hold the upper hand. Rival GameStop Corp. (GME) has struggled to keep pace, with its shares rising 8% year to date and falling 5.8% over the past 52 weeks.

Wall Street analysts are playing it safe and are cautious on BBY’s growth prospects. The stock has a consensus “Hold” rating from the 24 analysts covering it. That’s a downgrade from the “Moderate Buy” rating three months back. The mean price target of $79.37 suggests a potential upside of 6.5% from current price levels.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)