Bolingbrook, Illinois-based Ulta Beauty, Inc. (ULTA) is a specialty beauty retailer with a market cap of $19.9 billion. It offers branded and private label beauty products, including cosmetics, fragrance, haircare, skincare, bath and body products, professional hair products, and salon styling tools.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and ULTA fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the specialty retail industry. The company’s defining specialty is its unique "All Things Beauty, All in One Place" retail model, which disrupts traditional beauty shopping by combining high-end luxury prestige brands and affordable mass-market cosmetics under a single roof.

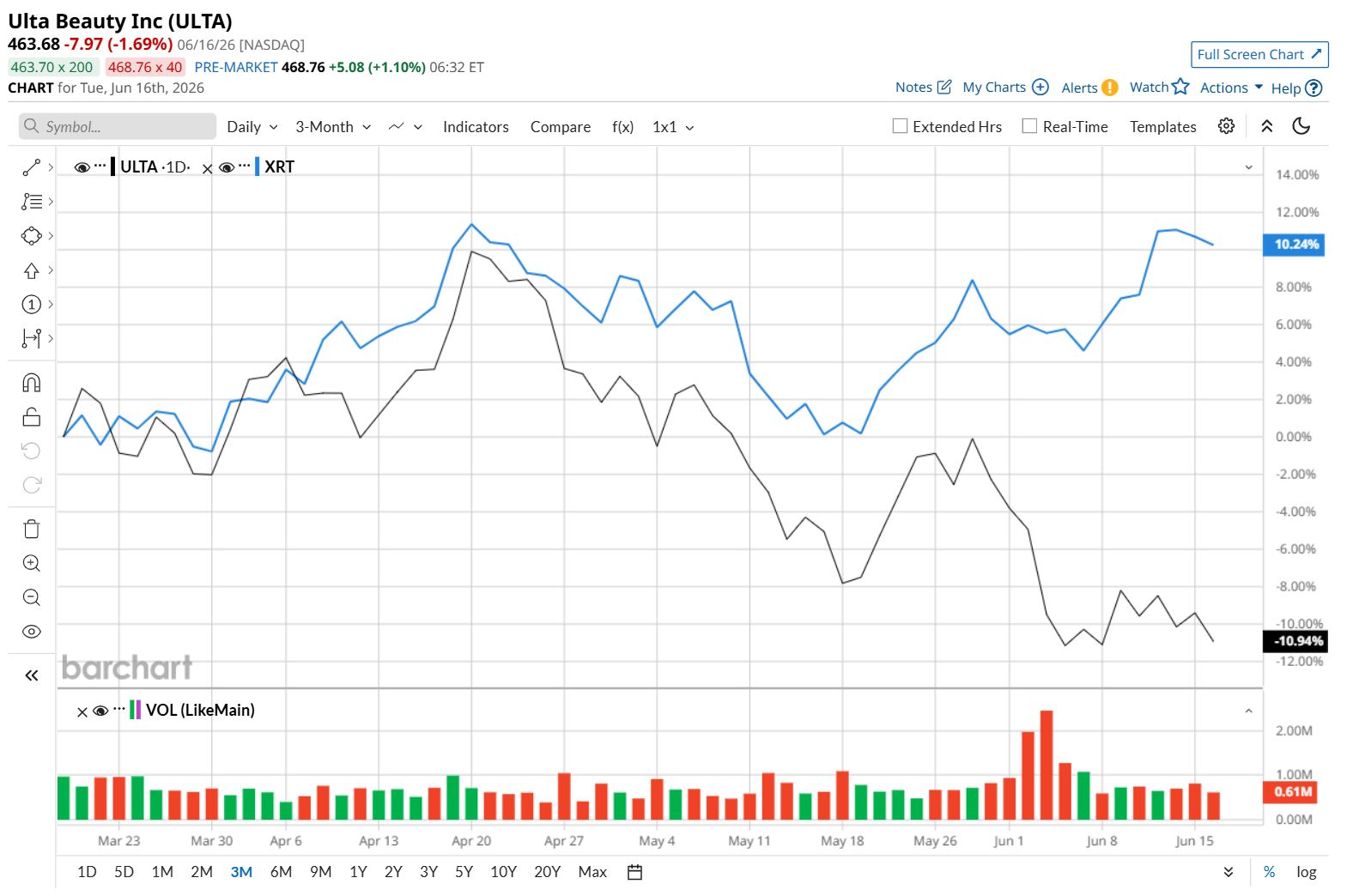

Despite its notable strength, the company had dipped 35.1% from its 52-week high of $714.97, reached on Feb. 18. Shares of ULTA have declined 10.3% over the past three months, considerably underperforming the State Street SPDR S&P Retail ETF’s (XRT) 8.6% uptick during the same time frame.

In the longer term, ULTA has fallen 1.8% over the past 52 weeks, notably trailing XRT's 13% return over the same time period. Moreover, on a YTD basis, shares of ULTA are down 23.4%, compared to XRT’s 2.1% rise.

To confirm its bearish trend, ULTA has been trading below its 200-day moving average since mid-March, with slight fluctuations, and has remained below its 50-day moving average since early March.

On Jun. 2, Ulta Beauty reported better-than-expected first-quarter results, but its shares fell 4.8% in the subsequent trading session. Revenue rose 11.1% year over year to $3.2 billion, exceeding analysts’ expectations by 1.6%, while EPS came in at $7.74, well above the consensus estimate of $6.90. The company credited its strong performance to healthy sales growth across both physical stores and e-commerce channels, with fragrance and prestige beauty products delivering particularly robust results.

Despite the solid quarter, investors appeared cautious as management struck a measured tone in its outlook. While Ulta remains focused on growing its U.S. business through enhancements to its product assortment and continued investments in stores and digital capabilities, the company highlighted intensifying competition and ongoing macroeconomic uncertainty as challenges that could weigh on future performance.

ULTA has notably outperformed its rival, Bath & Body Works, Inc. (BBWI), which declined 18.4% over the past 52 weeks. However, it has lagged BBWI’s 4.9% YTD rise.

Despite ULTA’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 25 analysts covering it, and the mean price target of $631.50 suggests a 36.2% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)