On Monday, June 15, Honeywell International (HON) received final board approval for its aerospace spin-off, locking in Monday, June 29, as the official separation date as the industrial giant sheds its skin and steps forward as a focused automation company. The stock wasted no time reacting, jumping roughly 3.2% in intra-day trading after the announcement, riding a broader market rally sparked by a U.S.-Iran peace deal.

The board formally greenlit the distribution of Honeywell Aerospace (HONA) shares to existing shareholders, setting the wheels in motion for a restructuring first unveiled earlier this year, and once the dust settles, the remaining entity takes the name Honeywell Technologies and keeps the HON ticker.

Shareholders of record as of June 15 will walk away with one HONA share for every two HON shares they hold, with the full distribution landing on June 29, pending standard closing conditions.

This ranks among the biggest industrial breakups in recent memory, carving out a standalone aerospace business covering commercial aviation, defense, and space, while Honeywell Technologies plants its flag in automation, industrial software, and related technologies.

CEO Vimal Kapur called the approval another milestone in the company's ongoing portfolio transformation, which has spanned several acquisitions and divestitures over recent years.

Honeywell also confirmed that a one-for-two reverse stock split of Honeywell Technologies common stock takes effect immediately after the spin-off closes, paired with a proportional cut in authorized share count, and the whole thing hinges entirely on the separation completing successfully.

About Honeywell Stock

Headquartered in Charlotte, North Carolina, Honeywell develops aircraft components, process technologies, control systems, sensing solutions, and specialized materials. Its products often operate behind the scenes, though they play a critical role in keeping industries moving efficiently.

With a market cap of nearly $144.1 billion, Honeywell serves customers looking to improve safety, reliability, operational performance, and energy efficiency. That wide reach has helped the company maintain its place among the industrial sector's heavyweights.

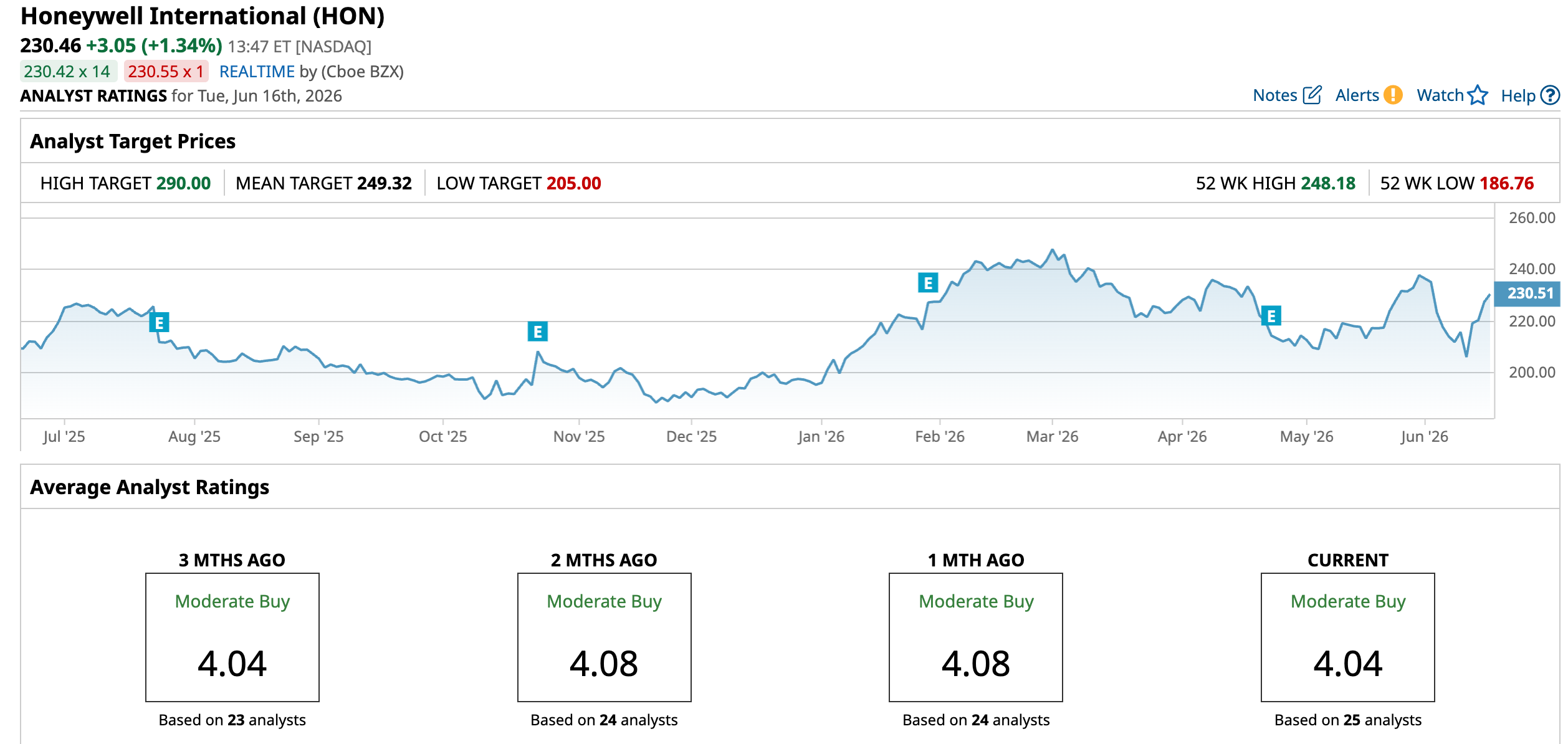

The stock has rewarded investors with a 9.1% gain over the past 52 weeks. Momentum has picked up considerably in 2026 as shares advanced 18.24% year-to-date (YTD) while adding another 8.18% during the past month alone.

Investors do pay a premium for that consistency. HON stock is currently trading at 20.91 times forward adjusted earnings and 3.66 times sales. Both figures sit above the broader industry average, signaling a premium.

Income-focused investors have also had reason to smile. Honeywell has raised its dividend for six consecutive years. The company pays an annual dividend of $4.76 per share, translating into a yield of 2.09%. Its latest quarterly dividend of $1.19 per share was paid on June 5 to shareholders of record as of May 15.

A Closer Look at Honeywell’s Q1 Earnings

Honeywell kicked off FY2026 with a mixed but largely encouraging first quarter report on April 23. Revenue increased 2.4% year-over-year (YOY) to $9.1 billion, falling short of Wall Street's $9.3 billion estimate. Earnings, however, told a brighter story. Adjusted EPS climbed 10.9% YOY to $2.45, ahead of analysts' expectations of $2.32.

Demand remained healthy across key businesses. Organic orders increased 7%, driven by strength in Building and Industrial Automation. That momentum helped lift backlog 2% sequentially to $38.3 billion, giving management plenty to work with heading into the rest of the year.

Operating income decreased 14.4% YOY to $1.5 billion, while net income amounted to $821 million, down 43.3% from the prior year’s period. Adjusted free cash flow also dipped 70.7% YOY to $56 million. Moreover, Honeywell finished the quarter with a formidable cash position, holding $12 billion in cash and cash equivalents as of March 31.

Management continues to tread carefully amid ongoing geopolitical tensions, particularly in the Middle East, while maintaining investments across Aerospace supply chains. Even so, the company expects business activity to gather pace during the second half of the year.

A strong backlog coupled with fresh contract wins in LNG and process automation has given Honeywell confidence that demand remains firmly intact. That confidence showed up in the company's guidance.

Following its solid first quarter performance, Honeywell left its full year outlook unchanged despite lingering uncertainty in the Middle East. The company still expects sales between $38.8 billion and $39.8 billion, alongside organic sales growth of 3% to 6%. Segment margin is projected to range from 22.7% to 23.1%, representing expansion of 20 to 60 basis points.

Honeywell also continues to forecast adjusted EPS of $10.35 to $10.65, reflecting growth of 6% to 9%. Operating cash flow is expected to land between $4.7 billion and $5 billion, while free cash flow should reach $5.3 billion to $5.6 billion, representing full year growth of 4% to 10%.

Wall Street expects a softer second quarter, with analysts forecasting Q2 FY2026 EPS of $2.42, down 12% from a year earlier. The longer-term picture remains considerably brighter. Analysts project full year FY2026 EPS of $10.54, which would mark a 7.8% increase from the prior year. Estimates for FY2027 call for another 8% climb to $11.38.

What Do Analysts Expect for Honeywell Stock?

Analysts remain largely constructive on Honeywell's prospects. Evercore ISI analyst Alexander Virgo maintains a “Buy” rating and attached a $265 price target to the stock. RBC Capital analyst Deane Dray took an even more optimistic stance by raising his price target to $275 from $268 while keeping an “Outperform” rating in place.

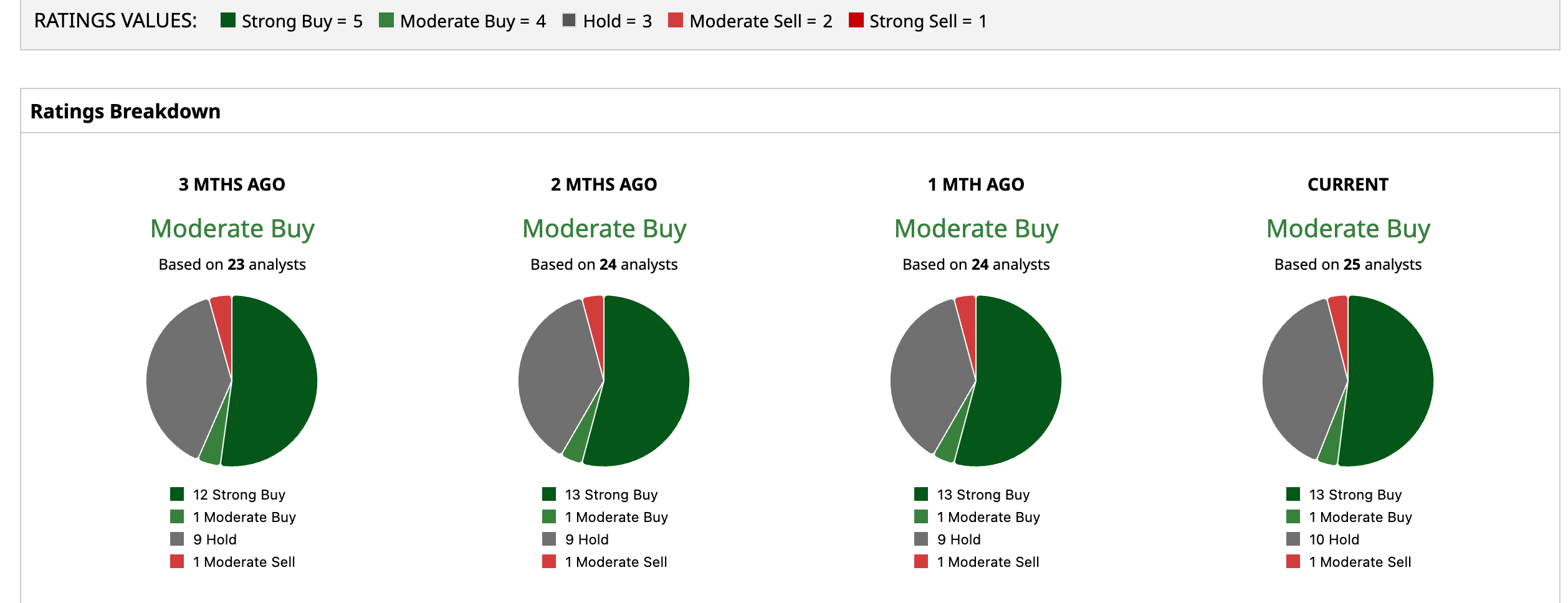

The broader Wall Street view leans positive as well. Honeywell is carrying an overall “Moderate Buy” rating. Among 25 analysts covering the stock, 13 recommend “Strong Buy,” one recommends “Moderate Buy,” 10 suggest “Hold,” and one recommends “Strong Sell.”

To that end, the stock’s average price target of $249.32 represents potential upside of 8.2%. Meanwhile, the Street-High target of $290 suggests a gain of 25.8% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)