/Amazon_com%20Inc_%20%20logo%20on%20building%20by-%20HJBC%20via%20iStock.jpg)

The race in AI is no longer just about building better models. It is now about owning the chips that power them.

Amazon.com (AMZN), Microsoft Corporation (MSFT), Alphabet (GOOG) (GOOGL), and Meta Platforms (META) are expected to spend as much as $725 billion combined in 2026, mostly on AI data centers, custom chips, and networking hardware. That spending push has made chips a key battleground. Intel Corporation (INTC) just showed how serious this is by unveiling its Crescent Island AI data center GPU at Computex 2026, going after Nvidia Corporation (NVDA) and Advanced Micro Devices (AMD) as companies race to lock in chip supply.

Amazon.com is building a strong position here. CEO Andy Jassy said its custom chip business, which includes Graviton CPUs, Trainium AI chips, and Nitro networking chips, already brings in over $20 billion a year and is growing at triple-digit rates. He also said it could reach $50 billion if Amazon sold the chips directly. Demand is clearly rising. Meta has agreed to use Graviton chips for AI workloads, and two large Amazon Web Service customers even tried to secure all of Amazon’s CPU supply for 2026, which the company turned down to keep access open.

Now, the Graviton5 CPU has moved from preview to general availability, marking a major step in Amazon.com’s push to control more of the cloud stack.

So does this finally push Amazon.com stock to be valued as the AI infrastructure player it is becoming?

Financial Momentum Remains Intact

Amazon.com runs a wide business that includes online retail, AWS cloud services, digital ads, and a growing logistics network, giving it several ways to drive revenue and profits.

The stock has been fairly steady, up 12.8% over the past year and 4.19% so far this year.

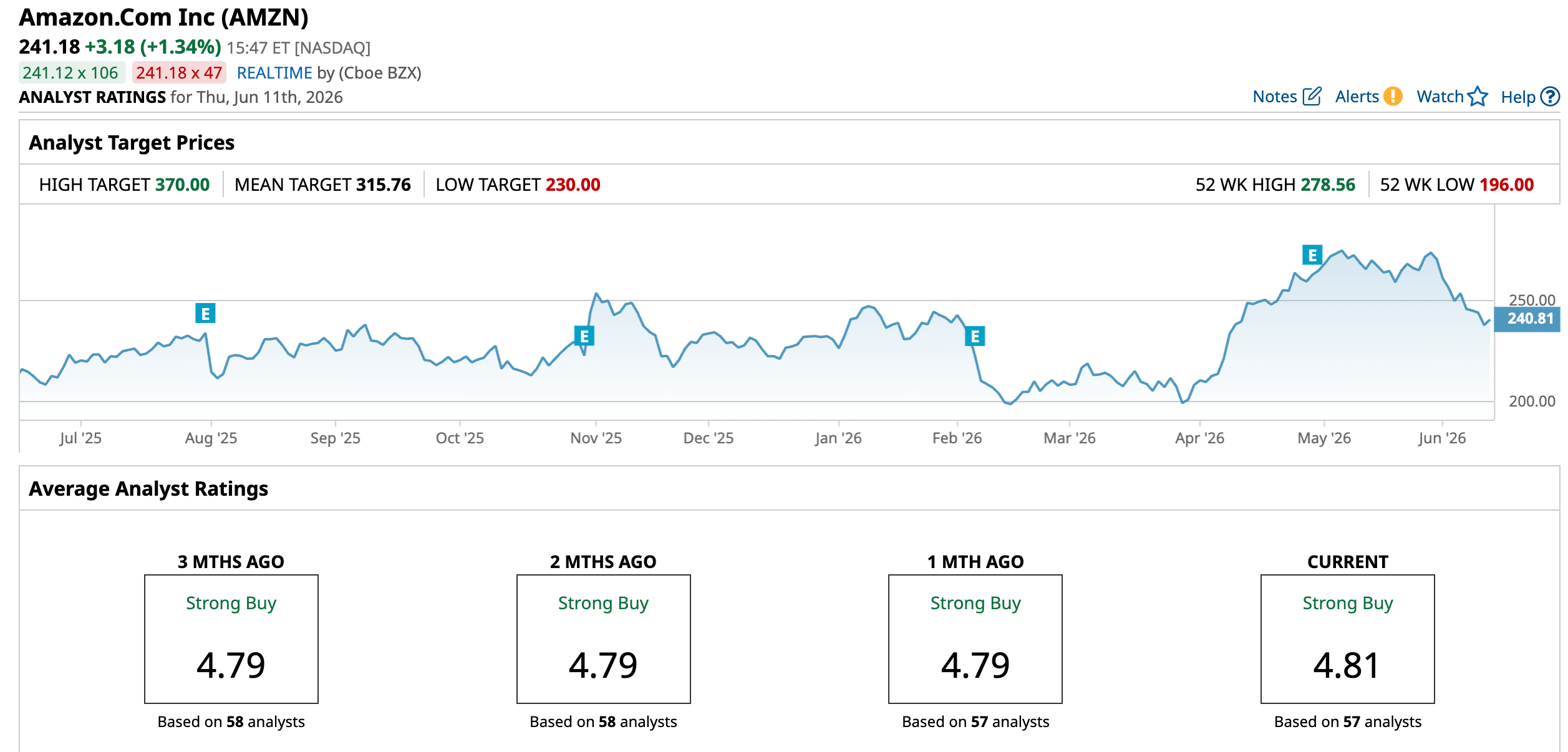

It still trades at a premium, with a forward price-to-earnings ratio of 31.65 times compared to the sector average of 15.50 times, showing investors are willing to pay more for its growth.

In Q1 2026, net sales rose 17% to $181.5 billion, or 15% excluding a $2.9 billion FX boost. Growth came from all parts of the business, with North America up 12% to $104.1 billion, international sales up 19% to $39.8 billion, and AWS leading with a 28% jump to $37.6 billion. Operating income increased to $23.9 billion from $18.4 billion, with AWS contributing $14.2 billion.

Net income reached $30.3 billion, or $2.78 per share, helped by a $16.8 billion gain from its Anthropic investment. Operating cash flow rose 30% to $148.5 billion over the past year, but free cash flow dropped to $1.2 billion as Amazon.com spent heavily, with $59.3 billion going into infrastructure, mainly for AI. For Q2, the company expects revenue between $194 billion and $199 billion and operating income up to $24 billion.

Silicon Strategy Drives Competitive Advantage

Amazon.com is opening up its logistics network to more businesses through Amazon Supply Chain Services (ASCS). This includes freight, warehousing, fulfillment, and delivery services that it originally built for its own operations and third-party sellers. Those systems have already been used by hundreds of thousands of sellers to move and store hundreds of millions of packages. Now, Amazon.com is offering them more broadly, putting it in direct competition as a third-party logistics provider across sectors like healthcare, manufacturing, automotive, and retail.

Also, it is expanding its less-than-truckload (LTL) service across the U.S., giving businesses a cheaper way to ship goods without paying for a full truck. What used to be limited to Amazon-bound shipments can now go to warehouses, distribution centers, and retail locations. Since 2019, the network has handled millions of pallets and supported tens of thousands of sellers, with demand continuing to grow.

At the same time, Amazon.com is working on cutting operating costs. A new multi-year deal with Transaera follows a six-month test of its cooling systems at an Amazon facility, where it showed strong energy savings in hot and humid conditions. With results confirmed by third-party analysis, Amazon.com is now expanding the rollout, with Transaera setting aside part of its U.S. production to support deployment.

Street Sees Continued Growth Ahead

Amazon.com is set to report earnings on July 30, 2026, and expectations are still moving higher. For the June quarter, earnings are estimated at $1.82 per share, up 8.33% from $1.68 last year. The September quarter is expected at $1.99, a smaller 2.05% increase from $1.95. For the full year, analysts see $7.71 in 2026 compared to $7.17 last year, a 7.53% gain.

In late April, UBS and BMO Capital both lifted their price targets ahead of earnings, pointing to stronger AWS demand and rising use of Amazon.com’s in-house chips. UBS raised its target to $304 from $301 and said AWS growth in 2027 and 2028 could come in higher than expected as Graviton adoption increases.

BMO went further, raising its target to $315 from $310, keeping an “Outperform” rating and calling Amazon.com a “Top Pick,” with checks showing AWS growth had already picked up again in early 2026.

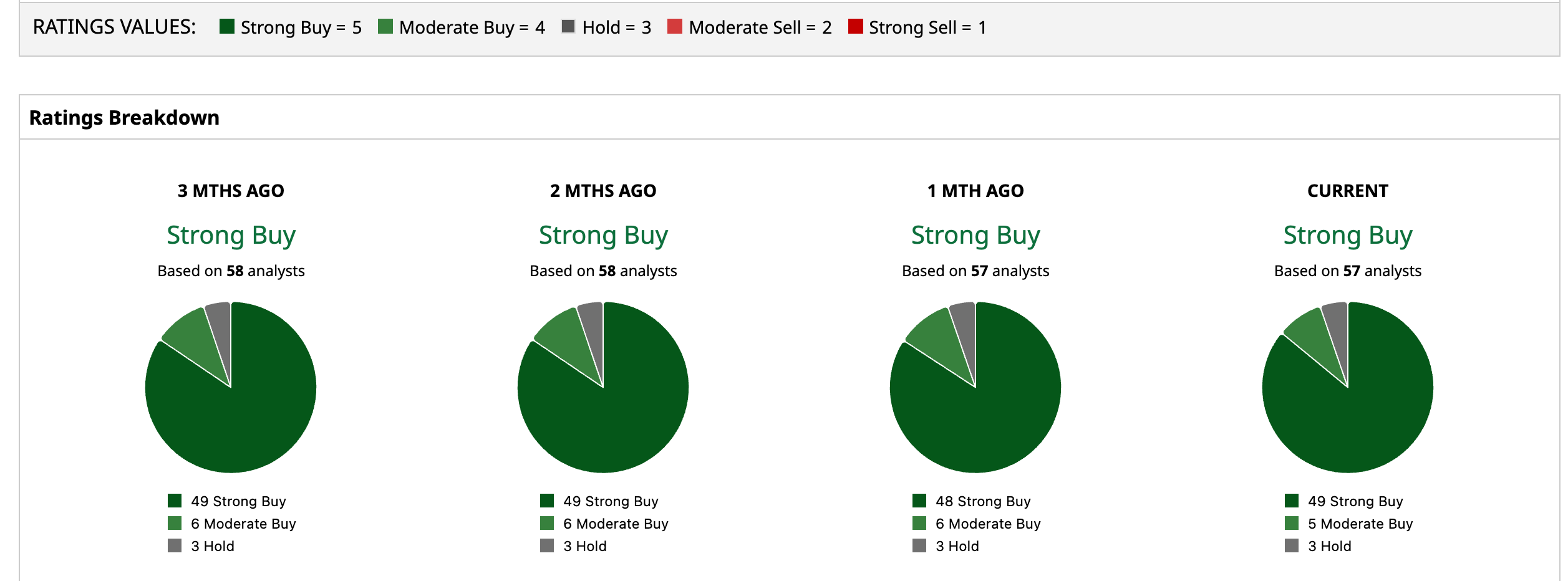

Overall, sentiment is very strong. Of 57 analysts, 49 rate the stock a "Strong Buy," with an average target of $315.76. From the current price levels, that suggests 30.9% upside.

Conclusion

Amazon’s push to make Graviton5 broadly available reinforces a shift that investors are starting to take more seriously. This is no longer just a cloud story but a full-stack infrastructure play where owning the silicon directly feeds margins, performance, and long-term AWS growth. With strong earnings momentum, rising analyst conviction, and clear demand for its in-house chips, the pieces are aligning. From here, the path of least resistance for AMZN stock appears tilted to the upside, especially if Graviton adoption accelerates and AWS growth continues to surprise ahead of expectations.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)