Dual Edge Research publishes two powerful newsletters that work great individually — and even better together. The Bull Strangle Newsletter focuses on stocks and options, combining stock ownership with premium-selling strategies to generate consistent income and market-beating returns. The Smart Spreads Newsletter specializes in seasonal commodity futures spreads, offering a diversified approach with low correlation to equities. Together, they deliver a complete investment perspective — one focused on income, the other on diversification — all under one simple subscription.

Introduction

Most traders instinctively focus on direction. They want to know whether a market is likely to move higher or lower. While direction certainly matters in outright futures trading, spread traders often face a different reality. In many cases, the structure of the forward curve has a greater influence on spread performance than the market's outright price direction. Understanding carry can help explain why some spreads seem to have a natural tendency to move in a trader's favor while others require much more precise timing. In many markets, carry is one of the most powerful structural forces affecting spread behavior.

What Is Carry?

Carry refers to the pricing relationship between nearby and deferred futures contracts. It reflects the market's valuation of time and is heavily influenced by factors such as storage, financing, and insurance costs, as well as immediate supply-and-demand conditions.

Carry is visible through the shape of the forward curve. In positive carry markets, deferred contracts trade at higher prices than nearby contracts. In negative carry markets, nearby contracts trade at higher prices than deferred contracts. These pricing relationships create natural pressures that influence how spreads evolve.

The Natural Pull of Positive Carry

Consider a grain market exhibiting positive carry. A deferred contract may trade at a premium to a nearby contract because grain stored for future delivery incurs storage, financing, and insurance costs.

As expiration approaches, both contracts converge in time. The economic value of carrying grain into the future gradually declines. As a result, some of the premium embedded in the deferred contract tends to erode. This process often creates a natural tendency toward spread compression.

For spread traders, that tendency can become a powerful tailwind. A trader positioned in the direction of carry is not relying solely on seasonal patterns or price forecasts. The structure of the market itself may be assisting.

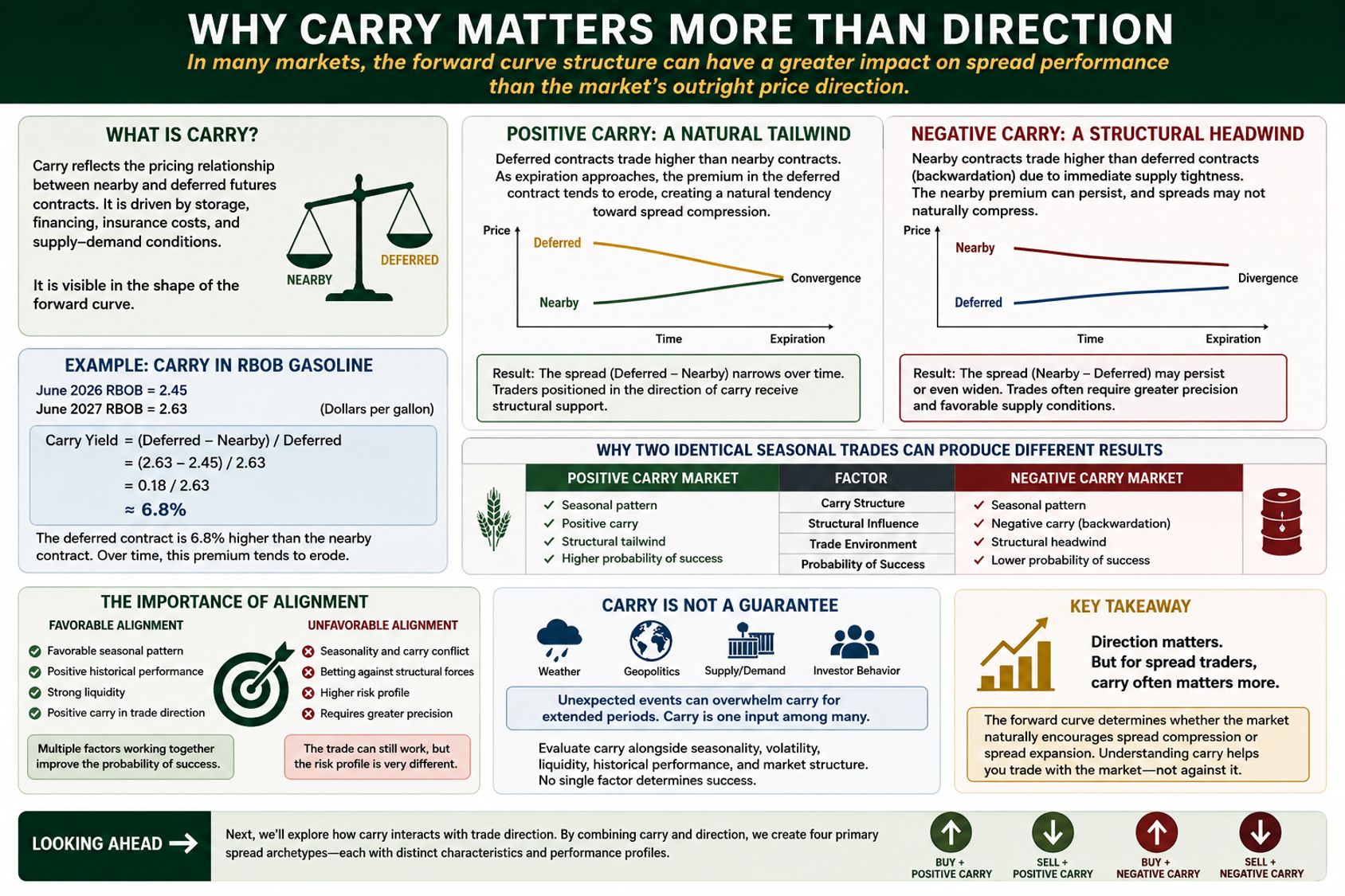

Example — Carry in RBOB Gasoline

Consider RBOB Gasoline. Assume the following prices:

- June 2026 RBOB = 2.45

- June 2027 RBOB = 2.63

(Prices quoted in dollars per gallon.)

To calculate carry yield:

![]()

The deferred contract is 6.8% higher than the nearby contract. The curve prices in storage and financing costs for the deferred month. Over time, as the deferred contract approaches delivery, that premium tends to erode. The price difference between the two contracts narrows. Again, this is a tendency—not a guarantee.

The Challenge of Negative Carry

Negative carry markets operate differently. In markets experiencing immediate supply tightness, nearby contracts may trade at a premium to deferred contracts. This structure is commonly referred to as backwardation. Energy markets frequently display this behavior during periods of strong demand or constrained supply. In these situations, buyers are willing to pay more for immediate delivery than for delivery months later. Unlike positive carry markets, backwardation markets often do not benefit from a natural tendency toward compression. The nearby premium can persist as long as supply tightness remains in place. As a result, spreads in negative carry markets frequently require greater precision. A favorable seasonal pattern may still exist, but the trader is no longer receiving the same structural assistance from the forward curve.

Why Two Identical Seasonal Trades Can Produce Different Results

Many traders assume that a strong seasonal pattern should behave similarly across markets. In reality, the forward curve can dramatically alter a trade's probability of success. Imagine two seasonal trades with nearly identical historical patterns. The first occurs in a grain market exhibiting strong positive carry. The second occurs in an energy market exhibiting strong negative carry. Although both trades may show similar historical tendencies, the underlying forces are very different. The grain spread may benefit from seasonal factors and carry working in the same direction. The energy spread may require supply conditions to remain favorable throughout the holding period. One trade enjoys a structural tailwind. The other faces a structural headwind.

The Importance of Alignment

The most attractive spread opportunities often occur when multiple factors align. A trader may identify:

- A favorable seasonal pattern

- Positive historical performance

- Strong liquidity

- Positive carry supporting the trade direction

When these factors point in the same direction, the probability of success often improves. Conversely, traders should exercise caution when seasonality and carry conflict. A seasonal pattern may still work, but the trader is effectively betting against one of the market's structural forces. This does not mean the trade should be avoided. It simply means the risk profile may be very different.

Carry Is Not a Guarantee

While carry can provide a meaningful edge, it should never be viewed as a guarantee. Markets frequently experience unexpected changes in supply, demand, weather, geopolitics, and investor behavior. These forces can overwhelm the influence of carry for extended periods. Carry should be viewed as one input among many. Successful spread traders evaluate carry alongside seasonality, volatility, liquidity, historical performance, and market structure. No single factor determines success.

Bringing It All Together

Many traders focus almost exclusively on direction. Spread traders should focus on structure. The forward curve determines whether a market naturally encourages spread compression or spread expansion. That structural influence can significantly affect trade performance.

Understanding carry helps traders identify when the market is working with them and when it may be working against them. Direction will always matter. But for spread traders, carry often matters more.

Looking Ahead

Understanding carry is only part of the equation. The next step is understanding how carry interacts with trade direction. A positive carry market can produce very different outcomes depending on whether a trader is buying or selling the spread. In our next article, we'll examine the four primary spread archetypes created by combining carry and direction, and why these combinations often lead to dramatically different performance profiles.

Want to build a more complete trading toolkit?

The Bull Strangle Newsletter focuses on stocks and options, combining stock ownership with disciplined option-selling techniques designed to generate consistent income while managing risk.

The Smart Spreads Newsletter focuses on seasonal commodity spreads, a historically proven approach that seeks opportunities across agricultural, energy, metal, and financial futures markets.

Each strategy is designed to stand on its own, but together they provide a diversified approach that can perform across a wide range of market environments. For traders looking to deepen their education, The Bull Strangle Strategy and Trading Commodity Spreads, both available on Amazon.

Visit BullStrangle.com to subscribe for just $1 for the first month.

For a video overview of the Bull Strangle Newsletter

For a video overview of the Smart Spreads Newsletter

Darren Carlat

Dual Edge Research

(214) 636-3133

DualEdgeResearch@gamil.com

Disclaimer

This information is for informational purposes only and should not be considered as investment advice. Past performance is not indicative of future results, and all investments carry inherent risk. Consult with a financial advisor before making any investment decisions.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)