The space sector was on a strong run through most of May 2026. Redwire (RDW) surged 181% year-to-date (YTD), Momentus (MNTS) jumped 109% in a single session, and Rocket Lab (RKLB) gained 71.95% since January. The rally was driven by excitement around SpaceX’s planned Nasdaq listing, which could value the company at up to $1.75 trillion. Money flowed into almost anything tied to space, and the idea was simple. When SpaceX goes public, the rest of the sector benefits.

Then things turned. A Blue Origin rocket explosion shook confidence, and investors who were sitting on big gains started taking profits. That quickly pushed many space stocks lower.

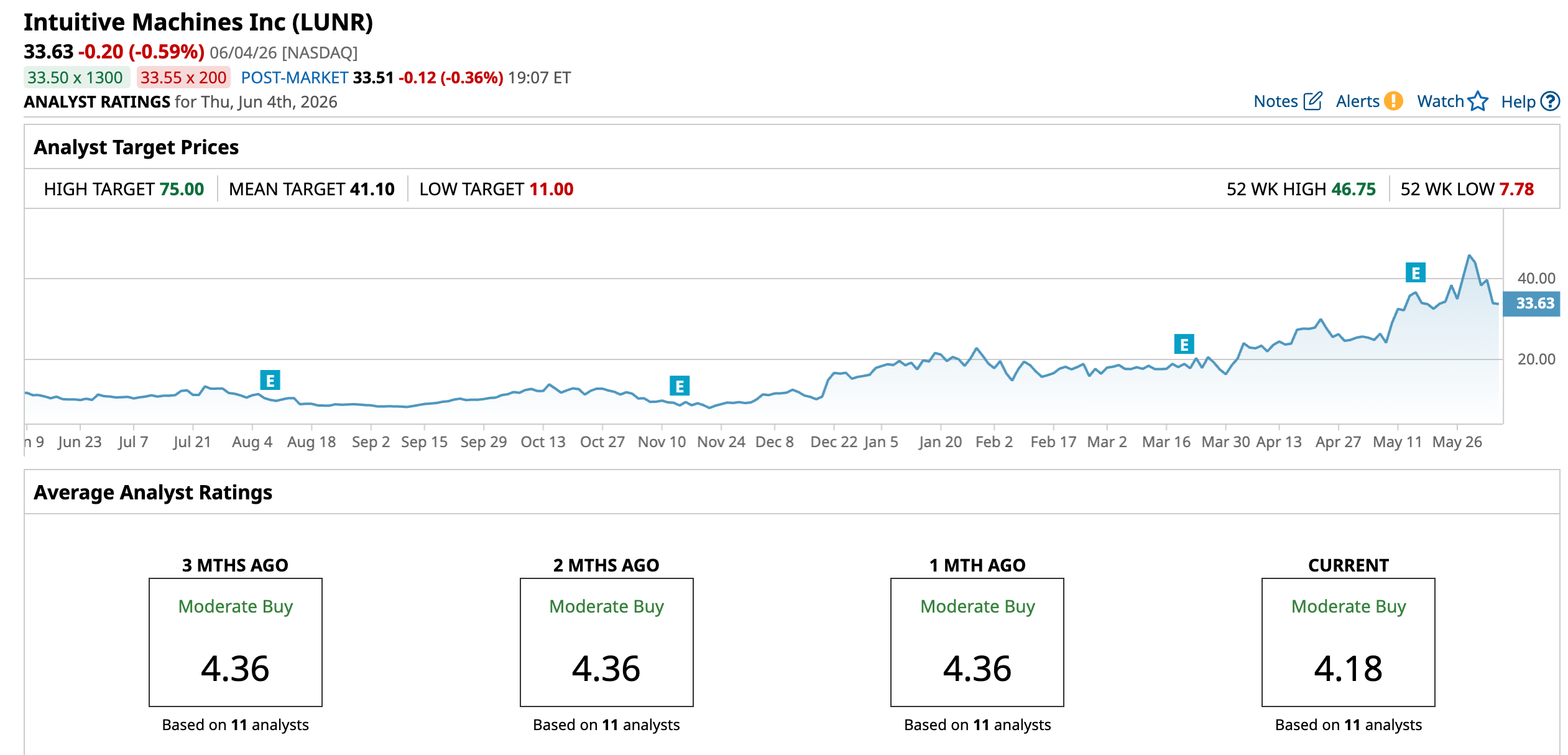

Intuitive Machines (LUNR) is right in the middle of that pullback. The stock hit $46.75 on May 28, its 52-week high, and is now down 28.06% from that level. After running more than 204% over the past year, some selling was expected. But the drop got worse after a setback. NASA passed on Intuitive Machines for its Lunar Terrain Vehicle contracts, awarding them to Astrolab and Lunar Outpost instead, a deal Cantor Fitzgerald estimated at up to $4.6 billion.

Now the setup is clear. The stock is down nearly 30% from its peak, and the sector has quickly shifted from chasing gains to locking them in. Is this a good entry point, or is the hype fading just as the SpaceX IPO approaches?

Breaking Down LUNR’s Numbers

Intuitive Machines builds and runs space systems, mainly focused on the Moon, data services, and now more end-to-end mission work as it expands its capabilities.

Even after the drop, the stock is still up about 204.07% over the past year and roughly 107.2% YTD .

The business itself is growing fast. In Q1 2026, Intuitive Machines reported record revenue of $186.7 million, nearly 3x higher than last year, helped by the Lanteris acquisition and steady work across CLPS, OMES, and NSNS programs. That number does not even include about $13 million from Lanteris due to timing, which points to even stronger momentum. Also, the company posted $2.7 million in positive adjusted EBITDA, showing early signs of profitability.

At the same time, future revenue is becoming more visible. Backlog jumped to a record $1.1 billion, up $842 million from the end of 2025, driven by new contracts and acquisitions. Management is guiding for $900 million to $1 billion in revenue for full-year 2026, with expectations of staying EBITDA positive.

The Real Drivers Behind Future Growth

The company is now the prime contractor for operations of NASA’s Lunar Reconnaissance Orbiter Camera under a $15.5 million, three-year cost-plus-fixed-fee contract, and for ShadowCam under a separate $4.5 million, three-year contract.

Those awards put Intuitive Machines in charge of imaging operations, data storage, analysis, mission support, lunar surface mapping, and advanced imaging of permanently shadowed lunar regions. Just as importantly, the company plans to use the publicly available LROC data archive to support its lunar data relay satellite constellation and build out orbital and surface navigation services.

That strategy extends back to Earth through its planned acquisition of Goonhilly Earth Station and COMSAT. The deal would add major deep-space communications assets in the U.K. and U.S., expanding Intuitive Machines’ space-to-ground network with communications, data transport, and positioning, navigation, and timing capabilities for lunar and cislunar operations. And, it broadens the customer base across civil, commercial, government, defense, and security markets.

The same vertical integration logic is behind the completed $800 million Lanteris Space Systems acquisition. With $450 million in cash and $350 million in stock, Intuitive Machines added a proven spacecraft manufacturer with capabilities across LEO, MEO, and GEO satellites serving missile warning, tracking, ISR, Earth observation, and space domain awareness. That gives the company more control over how it builds, connects, and operates mission solutions across the value chain.

Analysts Weigh In on Sector Outlook

The next earnings release is set for August 6, 2026. For the June 2026 quarter, analysts expect a loss of $0.05, a clear improvement from -$0.11 a year ago, reflecting 54.55% year-over-year (YOY) growth. The September quarter is projected at -$0.06, unchanged from the prior year. For the full year 2026, estimates stand at -$0.35 versus -$0.40 previously, implying 12.50% growth.

Roth Capital reiterated its “Buy” rating on May 28, and raised its price target to $75 from $50, implying more than 90% upside from where it was at the upgrade. On the other end, the most recent note of caution came earlier in the year, when Stifel on January 9, 2026, lifted its target modestly to $20 from $18 but effectively downgraded its relative stance.

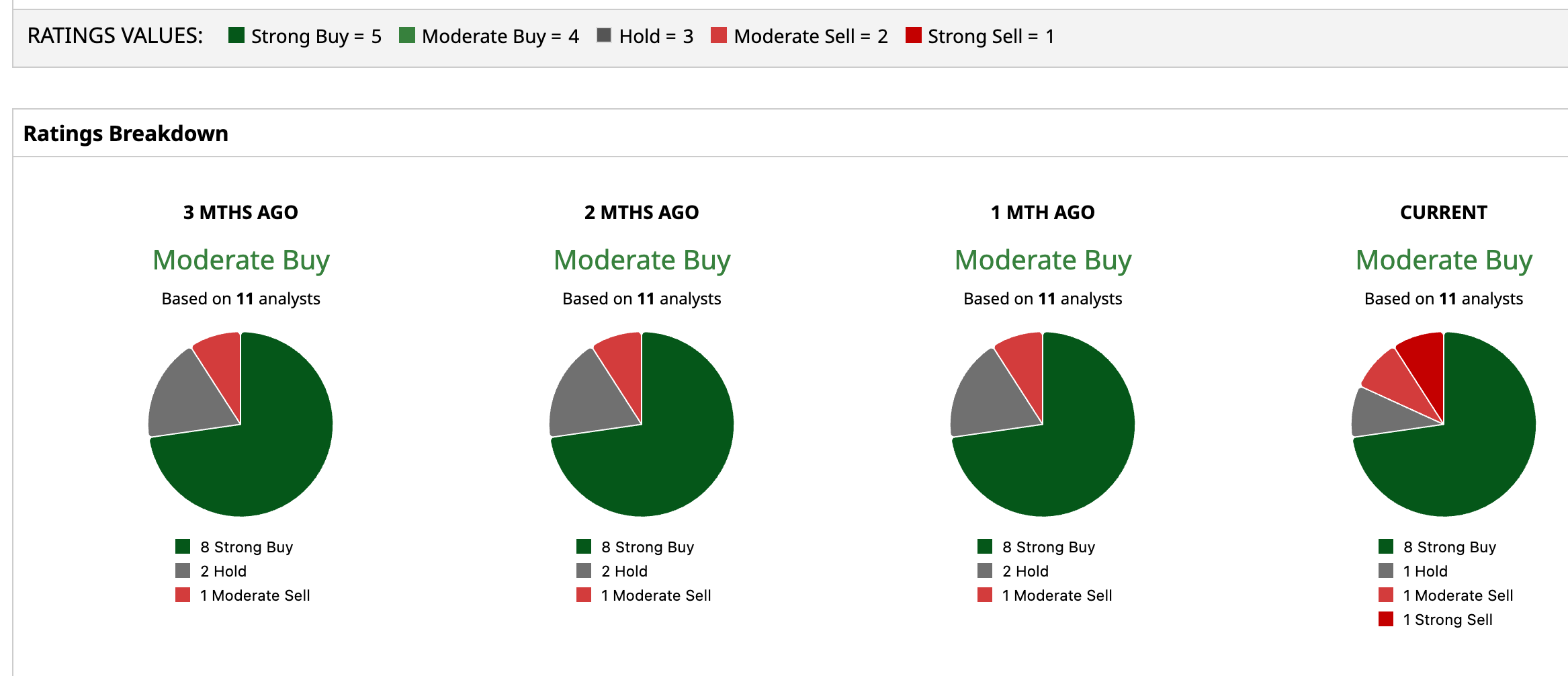

Taken together, 11 analysts covering the stock rate it a consensus “Moderate Buy,” with an average price target of $41.10, implying a potential upside of 22.2% from here.

Conclusion

The pullback in Intuitive Machines looks less like a breakdown and more like a reset after an overheated run, especially with the broader space sector cooling ahead of the SpaceX IPO. The fundamentals are still moving in the right direction with strong revenue growth, expanding backlog, and a clear path toward profitability, even as near-term sentiment gets shaky. Even so, volatility is likely to persist as capital rotates and expectations recalibrate. The most probable path here is volatile upside rather than a straight rebound, with shares gradually trending higher if execution holds and sector momentum stabilizes.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)