/Technology%20byAles%20Nesetril%20via%20Unsplash.jpg)

For years, the PC industry has been searching for its next big growth catalyst. Now, artificial intelligence is emerging as a strong contender, reshaping computer design and expanding their capabilities. Sensing that opportunity, Nvidia Corporation (NVDA) is betting that the next wave of AI adoption won’t be confined to massive data centers but will increasingly happen on the personal computers people use every day.

At Taiwan’s Computex conference, Nvidia CEO Jensen Huang unveiled the company’s new N1X processor and RTX Spark superchip, technologies designed to bring advanced AI capabilities directly to Windows PCs. It aims to power a new generation of AI-focused devices capable of handling demanding workloads without relying entirely on the cloud.

That shift could create opportunities well beyond Nvidia itself. As AI moves onto personal devices, demand may rise for everything from memory and storage to networking and PC hardware.

HP Inc. (HPQ), along with some others in the same industry appears determined to capitalize on that trend. The PC and printing giant recently unveiled a broad lineup of AI-powered PCs and developer workstations built around Nvidia RTX Spark technology. Designed for creators, developers, gamers, and enterprise customers, the new products reflect a growing belief that AI will become a standard feature of everyday computing.

If Nvidia succeeds in bringing AI to the edge, HP could find itself in a particularly favorable position as businesses and consumers upgrade to the next generation of AI-ready PCs. For investors, that raises an important question: Could HP become one of the biggest beneficiaries of the AI PC wave as demand shifts from traditional computers to devices built for a more AI-driven future?

About HP Stock

Founded on a legacy of innovation, HP Inc. is a leading technology company that helps people and businesses work, create, and connect through its portfolio of PCs, printers, 3D printing solutions, and workplace technologies. Headquartered in Palo Alto, California, the company serves consumers, small businesses, large enterprises, and public sector organizations across more than 180 countries.

Through its Personal Systems, Printing, and Corporate Investments segments, HP delivers a mix of hardware, software, services, and subscription offerings. With a market capitalization of approximately $23.8 billion, HP is increasingly focused on AI-enabled products and hybrid work solutions designed to enhance productivity and support the evolving needs of modern workplaces.

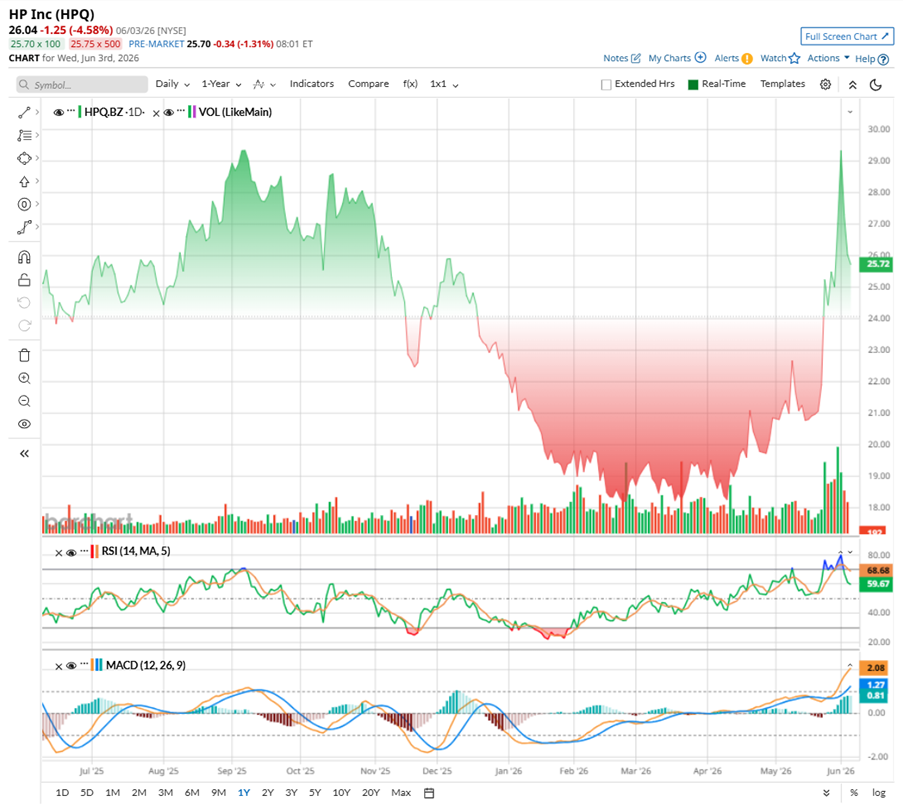

HP’s stock has quietly turned into one of the stronger comeback stories in tech this year. After spending much of late 2025 and early 2026 under pressure, shares of the PC-making giant have staged an impressive rebound, fueled by improving fundamentals and growing enthusiasm around AI-powered devices.

The rally recently pushed HPQ to a 52-week high of $29.65 on June 2. While the stock has pulled back 11.3% from that peak, the broader trend remains positive. HP’s shares are still up 4.45% over the past year, and the gains have accelerated in recent months. The stock has climbed 18.04% year-to-date (YTD), surged 37.12% over the last three months, and jumped 26.44% in the past month alone. Even over the last five trading sessions, HPQ rose 5.16%.

Much of the recent momentum came after HP delivered stronger-than-expected fiscal second-quarter results and offered an upbeat outlook, helped by rising demand for its AI-enabled PCs. Investors received another reason to cheer when the company unveiled a new lineup of Nvidia RTX Spark-powered laptops, notebooks, and desktop systems aimed at AI developers, creators, and gamers. The launch reinforced the idea that HP is positioning itself to benefit from the growing AI hardware wave rather than simply watching it from the sidelines.

Technically, the stock appears to be taking a breather after its sharp run higher. The 14-day RSI has cooled to 61.99 after recently reaching overbought levels, suggesting some of the near-term excitement has eased. At the same time, the MACD oscillator remains steady, with the MACD line holding above the signal line and a positive histogram. That typically points to bullish momentum still being in place, even if the stock pauses or consolidates after its recent surge.

When investors look at HPQ these days, the stock still looks relatively inexpensive. It trades at just 9.16 times forward adjusted earnings and about 0.4 times forward sales, both below many of its technology peers and even below its own historical valuation levels. The market is not placing a premium price tag on the company despite its steady business and cash generation.

Then there’s the dividend story, which has become one of HP’s biggest attractions. The company has paid quarterly dividends for 36 consecutive years and has increased that payout for 15 straight years. That’s the kind of consistency income-focused investors tend to appreciate.

HP is scheduled to pay a quarterly dividend of $0.30 per share on July 1, translating to an annual payout of $1.20 per share and a forward yield of roughly 4.6%. That’s well above the State Street SPDR S&P 500 ETF Trust’s (SPY) 0.98% yield and also State Street Technology Select Sector SPDR ETF’s (XLK) yield of 0.39%. With a payout ratio of just 35%, HP also appears to have enough room to keep rewarding shareholders in the years ahead.

A Snapshot of HPQ’s Impressive Q2 Report

HP’s latest quarter, released on May 27, showed that the company is still finding ways to grow, even as parts of the PC and printing markets remain challenging. In fiscal Q2 2026, HP delivered stronger-than-expected results, with revenue climbing 9% year-over-year (YOY) to $14.4 billion, which marks HP’s eighth consecutive quarter of top-line growth. Meanwhile, non-GAAP EPS jumped 21.1% annually to $0.86.

The biggest driver was HP’s Personal Systems segment, which includes its PCs and related products. Revenue from the business rose 13% YOY to $10.2 billion, accounting for more than two-thirds of total sales. The growth was driven by increasing demand for its AI-powered personal computers. Interestingly, PS segment growth came despite a decline in unit shipments. Total PC units fell 7%, with both consumer and commercial shipments moving lower. Still, stronger pricing and product mix helped push consumer PS revenue up 10% and commercial PS revenue up 14%.

Meanwhile, HP’s Printing business remained steady. Revenue held flat at $4.2 billion as weakness in consumer printing was offset by stable commercial demand and a modest increase in supplies revenue. Total hardware unit continued to face pressure, with total units down 7%.

HP also continued to generate solid cash flow. The company ended the quarter with $3.7 billion in cash, cash equivalents and restricted cash and generated $926 million in operating cash flow, along with $780 million in free cash flow. It also returned $374 million to shareholders through dividends and share repurchases.

Beyond the quarterly numbers, HP is betting that AI will play a bigger role in how people work every day. On the earnings call, interim CEO Bruce Broussard said companies are increasingly looking to run AI tasks closer to users and devices rather than relying entirely on the cloud, helping reduce costs while improving speed, privacy, and security.

To capitalize on that shift, HP recently unveiled a new lineup of AI-powered PCs, workstations, and AI-focused systems. And, the company is building a broader software ecosystem, with partners creating tools that can handle everything from audio transcription to content production directly on devices.

HP is bringing the same AI push to its printing business. New LaserJet printers feature AI-driven workflows, stronger security protections, and faster document processing. The company also introduced a compact industrial 3D printer and expanded HP IQ, a platform designed to connect and coordinate experiences across HP’s growing product portfolio.

Looking ahead, management expects fiscal 2026 non-GAAP earnings between $2.90 and $3.10 per share, while forecasting Q3 EPS in the range of $0.61 to $0.71, signaling confidence in the company’s ability to navigate a mixed demand environment.

Nevertheless, analysts believe the road ahead could be a bit bumpier. Wall Street expects HP’s earnings growth to cool, with Q3 EPS projected to decline 12% YOY to $0.66. For fiscal 2026, EPS is projected to dip about 4.5% YOY to $2.98, and then fall by another 1.7% annually to $2.93 in fiscal 2027.

What Do Analysts Expect for HPQ Stock?

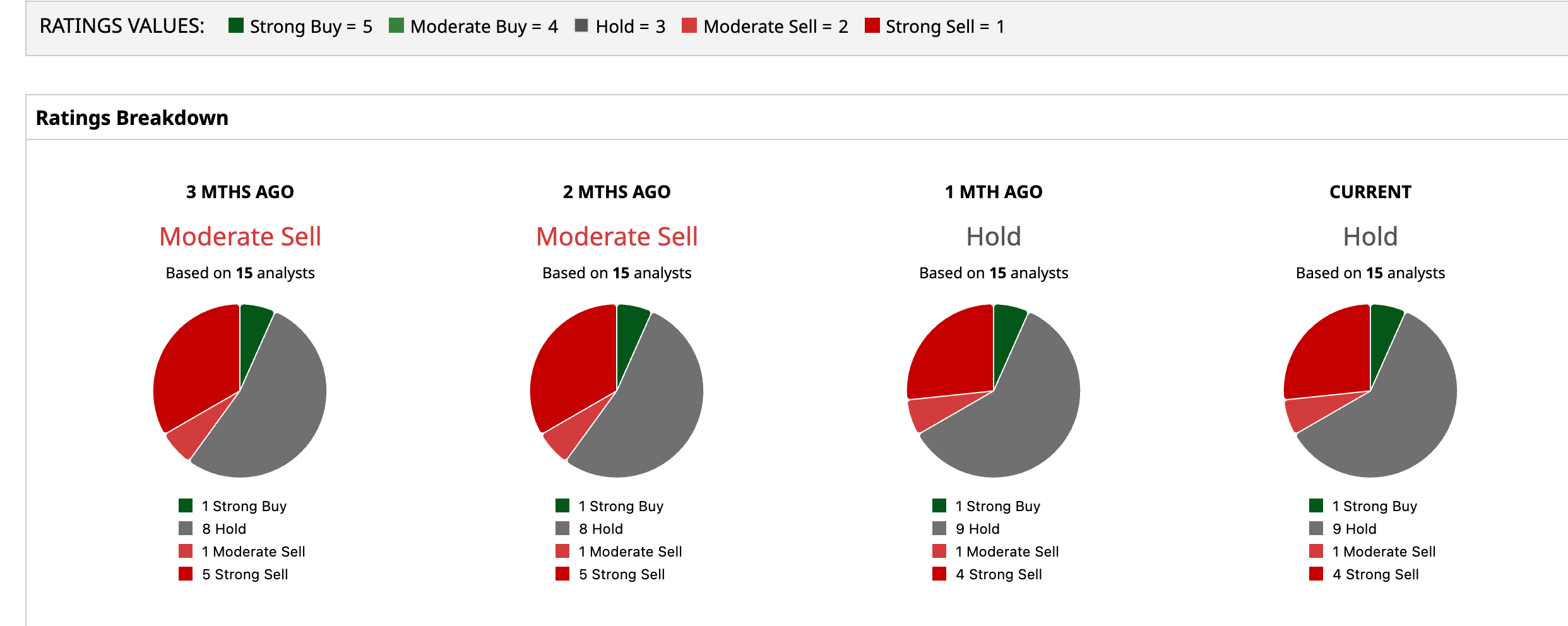

Analysts monitoring HPQ appear cautious. The stock carries a consensus rating of “Hold” overall, and that’s an upgrade from the “Moderate Sell” rating two months back. Out of 15 analysts, one is upbeat, giving a “Strong Buy,” nine are playing it safe with a “Hold” rating, one has a “Moderate Sell” rating, and the remaining four are outright skeptical, recommending a “Strong Sell.”

The stock currently trades above the average price target of $23.84, but the Street-high target of $34 suggests HPQ stock could rise as much as 29.28%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/The%20logo%20for%20ASML%20on%20a%20corporate%20office%20by%20Skorzewiak%20via%20Shutterstock.jpg)