Jim Cramer is bullish on the newly public FedEx Freight Holding Company (FDXF) because he believes the business was undervalued and underappreciated while buried inside parent FedEx. As FedEx Freight officially began trading independently on June 1 under the ticker FDXF, Cramer said the company “could be a true winner” after suffering from “not-so-benign neglect” inside the larger organization.

The bullish sentiment stems from the idea that FedEx Freight operates in the highly profitable less-than-truckload (LTL) trucking market, where competitors such as Old Dominion Freight Line (ODFL) command far richer valuation multiples than FedEx historically received. Analysts and investors believe the spinoff allows the freight business to finally be valued on its own merits instead of being bundled into FedEx’s broader express and parcel operations.

Another reason Cramer and Wall Street are paying attention is the unusually strong market debut. FedEx Freight immediately joined the S&P 500 Index ($SPX) and the Dow Jones Transportation Average ($DOWT) after the separation, which forces many index funds and institutional investors to buy shares.

Nevertheless, short-term volatility, separation costs, and execution risk remain as the business transitions into a standalone company.

About FedEx Freight Stock

FedEx Freight officially began trading as an independent company on June 1 after being spun off from FedEx Corporation (FDX), with shares now listed on the New York Stock Exchange under the ticker symbol FDXF while simultaneously joining the S&P 500 Index. The company is North America’s largest less-than-truckload carrier, serving industrial, manufacturing, retail, and healthcare customers through a broad transportation network focused on speed, reliability, and premium freight services. Its market cap currently stands at $28 billion.

Leading the newly independent company is longtime FedEx executive John A. Smith, who officially became CEO upon completion of the spinoff after previously serving as chief operating officer for FedEx’s U.S. and Canada operations. Meanwhile, R. Brad Martin, vice chairman of the FedEx board, has taken over as chairman of FedEx Freight’s board.

Under the terms of the separation, FedEx shareholders received one share of FedEx Freight common stock for every two shares of FedEx owned as of the May 15, 2026, record date. FedEx distributed roughly 80.1% of the new company to shareholders while retaining a 19.9% stake that it plans to monetize over time.

The market debut generated substantial investor attention as Wall Street increasingly views standalone LTL trucking companies as deserving higher valuation multiples than diversified transportation conglomerates. However, the first trading session was volatile. FedEx Freight shares surged as high as $166.90 on June 1, before reversing sharply and ultimately closing at $150.01. The stock surged by 2.55% on June 2.

In addition, FedEx Freight enters the public markets with ambitious medium-term financial targets. Management expects fiscal 2026 revenue of $8.7 billion and adjusted operating income of $1.1 billion while targeting annual revenue growth of 4% to 6% and core profit growth of 10% to 12% over the medium term. The company is also aiming for operating margins near 12%, supported by improving freight pricing conditions, automation investments, and network optimization initiatives.

Also, industry conditions may provide a favorable backdrop for the newly independent trucking giant. Freight markets have recently begun tightening as weaker carriers exit the industry and capacity becomes more constrained, trends that could support stronger pricing and profitability across the LTL sector.

What Do Analysts Expect for FedEx Freight Stock?

Analysts across Wall Street are largely viewing FedEx Freight’s launch as one of the transportation industry’s most significant spinoffs in years, as the separation from FedEx allows the business to be evaluated more like a dedicated less-than-truckload carrier rather than part of a diversified logistics giant.

Ahead of the spinoff, JPMorgan (JPM) highlighted that FedEx Freight may initially trade at a modest discount to established LTL rivals because of near-term transition uncertainty, but could see its valuation improve as the company delivers on technology investments and commercial growth strategies.

Meanwhile, BMO Capital Markets emphasized that strong execution and the ability to preserve premium service standards will be essential for FedEx Freight to command valuation multiples in line with top players in the sector.

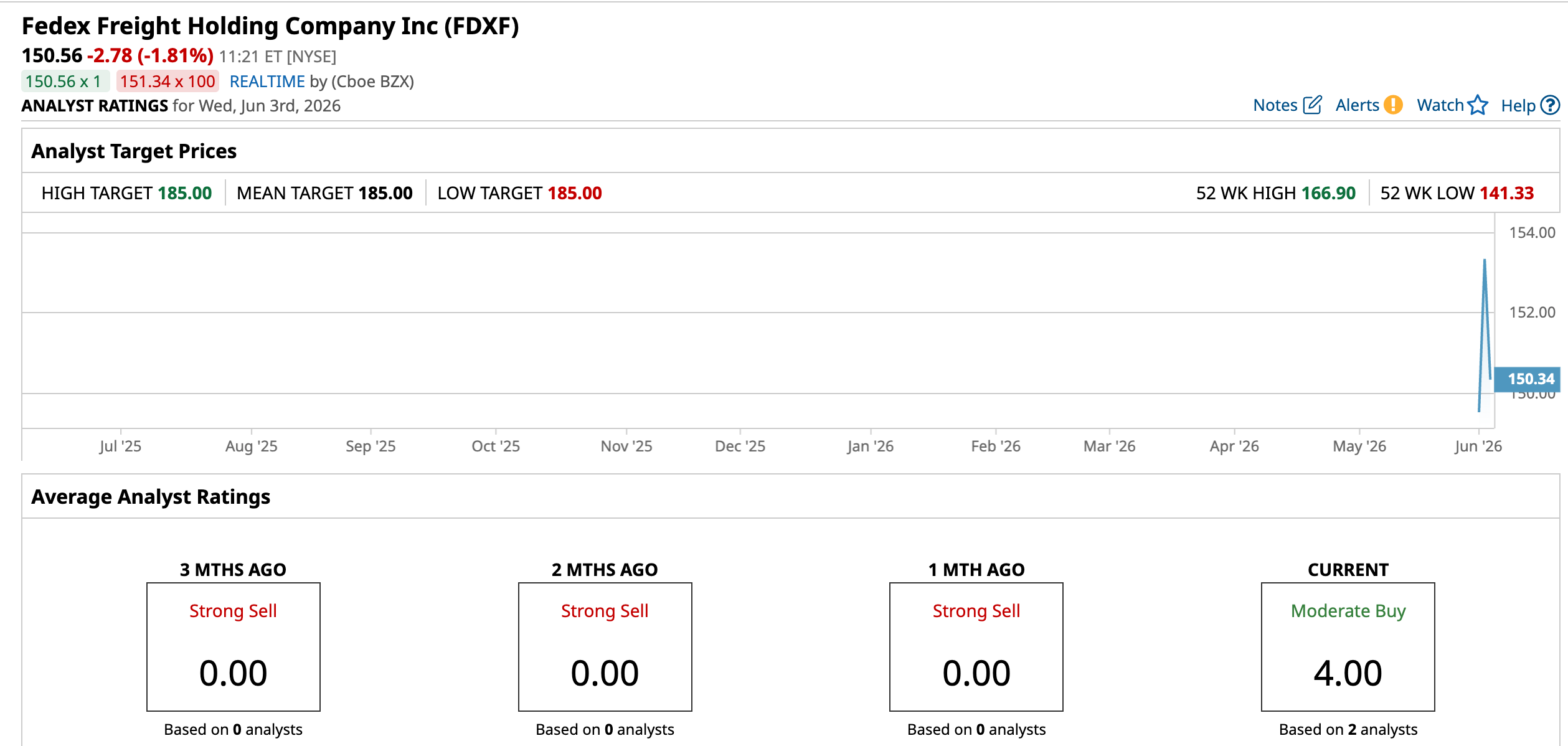

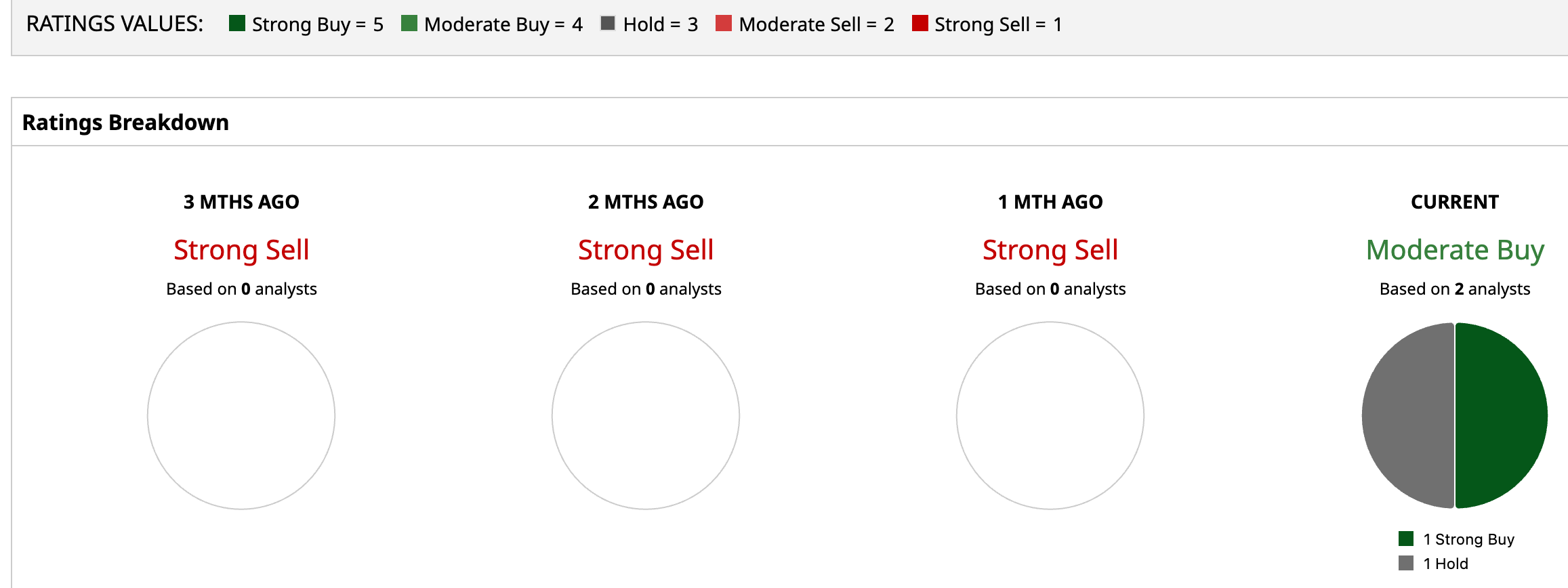

Additionally, Truist Securities initiated coverage on FedEx Freight Holding Company with a “Hold” rating and a $155 price target, saying it wants clearer evidence that the newly independent trucking company can improve profitability and move closer to historical peak margin levels before turning more bullish.

On the other hand, BofA Securities initiated coverage on FedEx Freight Holding Company with a “Buy” rating and a $185 price target, highlighting the company’s dominant position as the largest less-than-truckload carrier. Overall, FDXF has a consensus “Moderate Buy” rating as of now, with both the average and Street-high price targets pointing to a potential 22.88% upside from here.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Amazon_com%20Inc_%20%20package%20by%20-%20AdrianHancu%20via%20iStock.jpg)

/Salesforce%20Inc%20HQ%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)