/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

Sandisk Corporation (SNDK) completed its separation from Western Digital in February 2025 and began trading on the Nasdaq under the ticker "SNDK" as an independent, pure-play flash memory and enterprise SSD company. The spinoff freed SanDisk to operate without the hard-disk drag of its former parent, positioning it exclusively in the high-growth NAND flash and accelerated-computing storage market, just as global AI infrastructure demand ignited a once-in-a-generation memory supercycle. Revenue remains heavily weighted toward its enterprise storage, accounting for over 55% of total quarterly sales.

Sandisk has reinvented itself from a legacy consumer brand into a mission-critical AI infrastructure play, supplying the high-speed, high-density flash storage that modern large language models and agentic AI systems cannot function without.

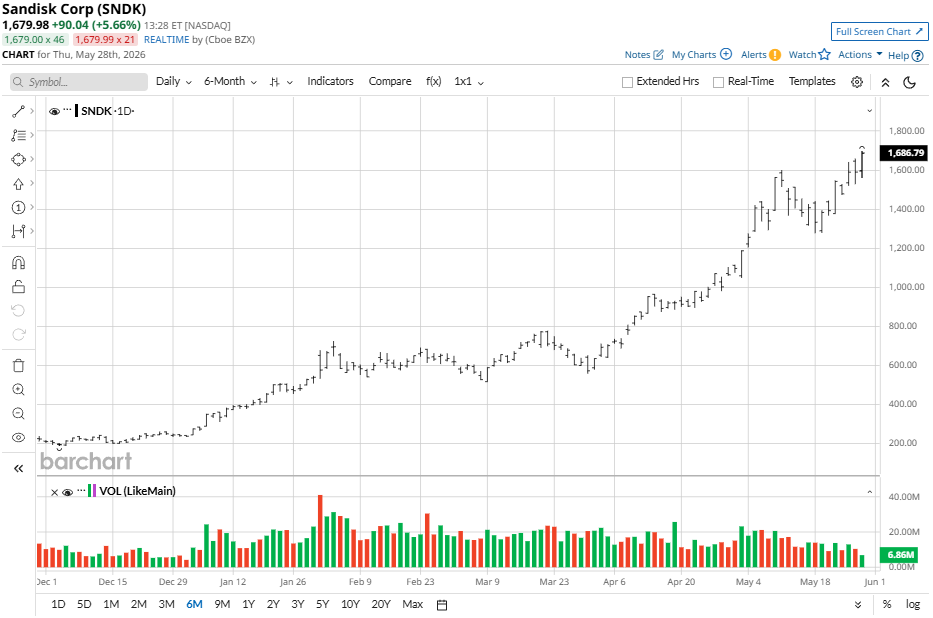

Sandisk Stock Rallies

Since its spinoff, SNDK has delivered total returns reaching nearly 4,500% over the past 12 months, making it one of the most extraordinary post-spinoff performances in semiconductor history, far outpacing every other stock in the S&P 500. The stock surged over 550% in 2025 alone, fueled by booming AI-related NAND demand, a tightening supply environment, and rapid margin improvement.

Against the S&P 500 Information Technology Index ($SRIT), SNDK has significantly outperformed the Philadelphia Semiconductor Index over the past 12 months, driven by its specialized exposure to AI-optimized enterprise storage, cementing its status as the defining momentum trade of the AI storage cycle.

Sandisk Results

Sandisk reported fiscal Q3 2026 revenue of $5.95 billion, up a staggering 251% year-over-year and 97% sequentially, surpassing the company's own guidance range and decisively beating Wall Street estimates. Non-GAAP diluted EPS came in at $23.41, representing a massive beat against analyst expectations of approximately $14, with a positive EPS surprise of nearly 60%. Datacenter revenue surged 233% sequentially, driven by strong adoption among AI infrastructure builders, semi-custom customers, and technology companies deploying AI at scale.

GAAP gross margin expanded to 78.4% in Q3 2026, up 27.5 percentage points sequentially, while operating income surged 286% quarter over quarter to $4.11 billion, reflecting the extraordinary pricing power unlocked by the global NAND supply shortage. The company secured five multi-year AI-focused supply agreements worth approximately $42 billion in total commitments, and authorized a $6 billion share repurchase program, underscoring management's confidence in the durability of its earnings power. Sandisk also ended the quarter completely debt-free.

For Q4 FY2026, management guided revenue in the range of $7.75 billion to $8.25 billion, with non-GAAP EPS expected between $30 and $33, guidance that, once again, surpassed Wall Street consensus. CEO David Goeckeler characterized the quarter as a fundamental inflection point, stating: "We are advancing to a new business model built on multi-year customer engagements backed by firm financial commitments. Together, this transformation is driving structurally higher and more durable earnings power," positioning Sandisk as not merely a cyclical memory name, but a structurally transformed AI infrastructure powerhouse.

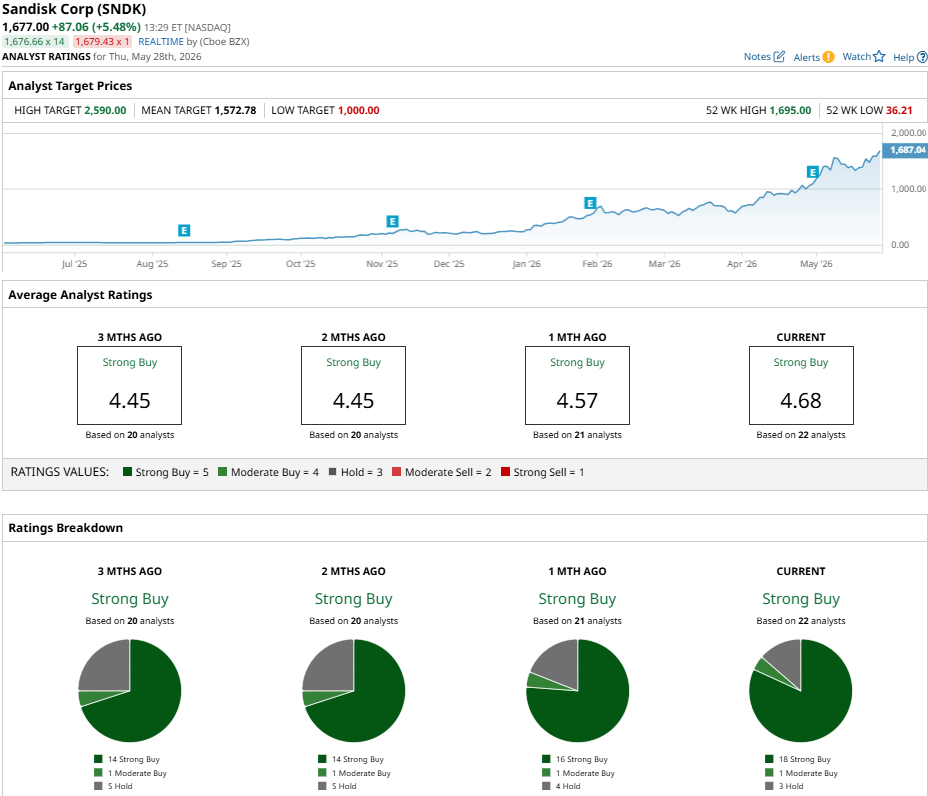

Sandisk Upgraded by Analyst

Barclays analyst Tom O'Malley upgraded Sandisk to “Overweight” with a bullish $2,300 price target, signaling a potential 34% upside from here, calling memory and storage the most attractive segments after AI accelerators. O'Malley highlighted Sandisk as the most structurally innovative player in the space, crediting its New Business Model (NBM) contracts. Some extend as far out as 2031 to fundamentally transform the company's earnings visibility.

The three NBM agreements signed in Q3 FY2026 alone carry a minimum revenue commitment of approximately $42 billion, with financial guarantees exceeding $11 billion, including $400 million already recognized as prepayments. O'Malley argued these contracts eliminate the traditional cyclicality risk of memory stocks by providing Sandisk with guaranteed revenue and customers with assured supply, a structural shift that Barclays believes sets the stage for another significant leg higher in SNDK shares.

Should You Buy SNDK?

With Barclays setting a Street-high price target of $2,300 and citing structurally transformative NBM contracts as a multi-year earnings catalyst, the bull case for Sandisk is hard to ignore. However, the broader Wall Street consensus reflects a stock that has largely priced in near-term upside. SNDK carries a "Strong Buy" rating across 22 analyst ratings, comprising 18 "Strong Buy," one "Moderate Buy," and three "Hold," with a mean price target of $1,714, close to current levels.

For long-term investors, SNDK remains a high-conviction AI storage play, though disciplined entry points matter given the stock's extraordinary run.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)